Sure, do it. It’s definitely not a bad choice if you don’t want to learn about investing in US ETFs.

Well I would say the criteria would be based on your domicile. If you are planning to be domiciled in Switzerland for years to come, then it’s fine to use the US ETFs. The Irish ETFs are meant for people domiciled in a country without a favourable deal with the US, or maybe for people who use a broker without cheap exchange of currency to USD.

Well, US funds are better than the Irish funds from a tax perspective (for Swiss residents). So VT is better than any combination of the Irish funds.

Also, the small caps don’t really make a big difference. The have a really small total market cap plus their return curve mimics the large and medium caps. Here’s a demonstration:

If you go for VWRL instead of VT, you will probably lose (per year) around 0.3% on tax, 0.2% on other hidden things, so maybe 0.5% in total.

What I mean is, if your money is stuck with a Swiss broker (CT, Swissquote, PF), you don’t necessarily have to close your account. You could buy VFEM (Emerging markets) or VEUR (Developed Europe) instead. If you own VUSA, then Vanguard has to pay 15% withholding tax to the USA for the dividend, which is 2% of the portfolio. This means that 0.3% of the portfolio is lost. If you, however, own VOO, you can get a refund from the Swiss tax office. If your portfolio is worth 100’000, that’s like 300 CHF extra money each year. sure, in the first year it takes a lot of time to understand it and learn it, but in the following year it should cost you maybe 10 minutes of your time.

And if you invest in VFEM or VEUR, there is no easy tax to reclaim, so theoretically no potential loss.

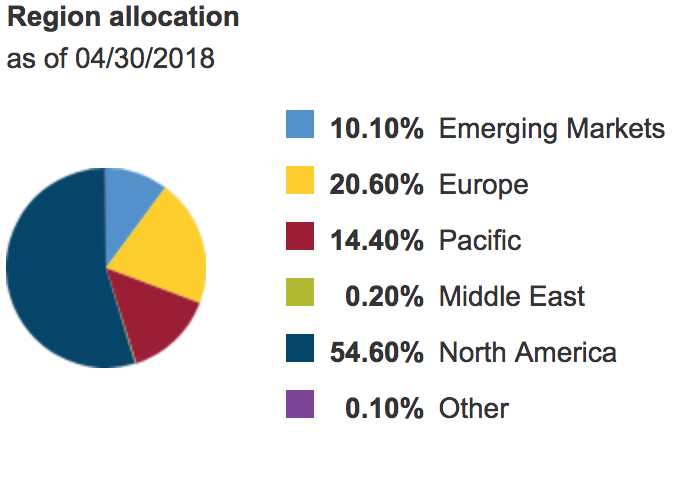

Yes, if you want to keep a fixed ratio of A and B (let’s say 50% / 50%), then if A is outperforming B, then you will need to sell some A and buy some B to bring it back to 50%. However, this does not apply to replicating VT, because there the ratio between US and exUS is NOT fixed! So once you replicate the fund, it should roughly keep the right proportions.