So the thing to be aware of (from a Swiss resident perspective) to to check whether the US domiciled ETF that one has selected appears on the list of the funds on the ICTax website.

If it doesn’t appear, then the best course of action would be (I presume) to send an email to ICTax authorities and request them to add the fund. This would avoid arbitrary taxation of any gains in the future.

On the topic of accumulating funds, I have a question which will sound trivial to many of you but I could not find an answer online: what do you actually see in your portfolio the day the dividends are paid? Is there automatically an increase in capital (ie. shares)?

Edit: What if the dividend is less than a full share?

No, that’s important for accumulating funds. Distributing funds as I already said are easy. You declare exactly the amount of dividends you received, it’s an undisputable number. For accumulating funds the line between capital gains and income is blurred, taxes are correspondingly more difficult and burden of proof what part is taxable income and what is not is on you. If the fund is in ICTAX, the authorities already did the math and you can piggyback on it

NAV value changes on the basis of which the fund’s shares are traded on the market.

Then it goes into the cash pile, there’s always of a bit of cash kept for expenses and future distributions. Some funds also invest the cash for distribution in the market during the short time before paying out, others don’t. Whatever a particular fund is doing will contribute to its tracking error vs benchmark, they don’t guarantee you it will be exactly zero.

Thanks, that would make sense. I saw that the dividends of the US-based ETFs are higher, but I thought it was solely due to the absence of the US withholding tax. I will investigate that further. It’s just hard to find a website with return chart for both EU & US ETFs.

But what about VT vs VWRD? There are a few thousands of shares missing in VWRD and is still gives the same price?

Dropping some low weighted stocks probably ain’t going to move the needle much. In fact this is exactly what some ETFs do, this is called “optimized sampling” in industry jargon

All the data you need - price & dividend is readily available e.g. on Yahoo. It seems like they’ve closed their API recently, but you can still download csv’s manually in UI. For example here’s dividend history for VWRL, note “Download Data” button. And then with just a few lines of code or an excel spreadsheet you can slap together whatever chart you want on your own

VWRD is missing small caps, which take up about 10% of VT. And small caps slightly outperform VT. In the end, we should see a small, but visible, difference.

Optimized sampling is not how Vanguards ETFs are done, or? I thought they use physical replication.

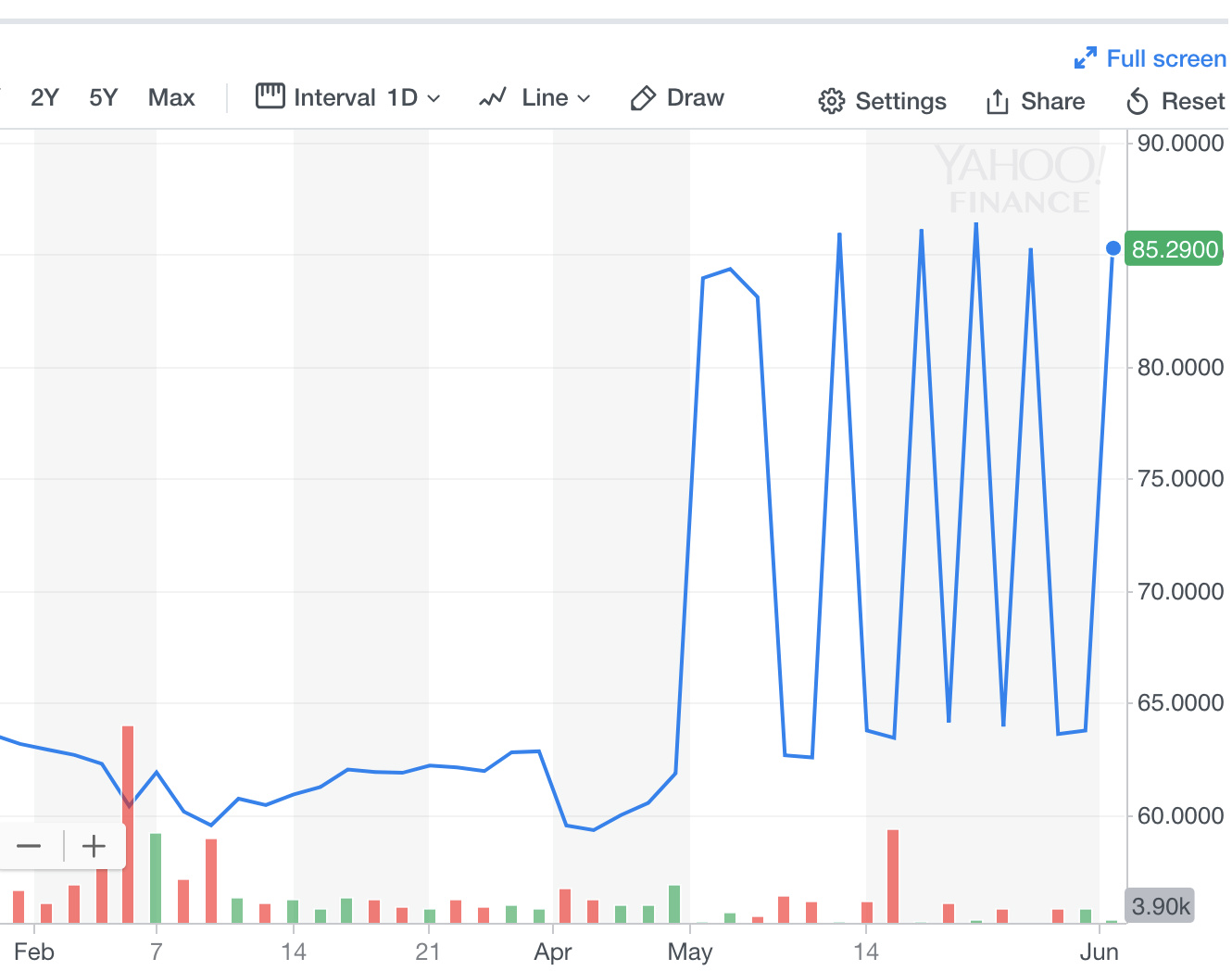

Yeah, Yahoo would be a nice option, but did you look at the chart? WTF is going on there? Yahoo and Google often suffer from this problem. Their data is unreliable.

Hmm looks like data error, just check a few other sources like vanguard’s own website

Well, I guess they didn’t this time. Anyway investigating this methodologically isn’t hard: get & clean the data, look at correlations between N day returns, throw in some simple linear regression or PCA at it, plot all things and you’ll see exactly what’s going on.

Thanks @hedgehog. However I am a bit confused since my understanding is that it contradicts your answer just above. I understood that NAV value will change, and therefore wouldn’t it be something like new share value = old share value + dividend, hence making the issue with not having full shares irrelevant?

Could you detail the cash pile story? Is it that the dividend is not paid to the investor? If there is quaterly payment of a dividend, you then need quite a lot of money to be able to purchase full shares.

After dividend is paid, cash increases, what’s so hard to understand about this and where’s the contradiction? Share’s value btw immediately drop on ex-dividend date as the dividend payment was priced into the share price by the market before ex-dividend. Between ex-dividend and dividend payment instead of cash you have accruals, but that’s a minor technical detail.

At the scale that ETF providers operate, the issue is a negligible rounding error

NAV = shares + cash

The fund will normally try to convert as much cash as possible into shares in order to track the benchmark, but there will be always some small amounts left - to pay for transactions and managers’ salaries for example, and also arising from normal day-to-day business operations: creating new or liquidating old ETF share blocks in response to market demand. Distributing ETFs also need to set aside cash to pay you your dividend

thanks this is great. i think i found another good answer on the link below:

I understand you are basically saying the same as:

"- Had I had the income version of the fund, the value of my holding would have fallen by around 4%, and I would now have 4% cash sitting in my income account

With the accumulation version, you don’t see any rise in your fund value from distribution yield, but you don’t lose the equivalent value either."

Assuming ETF doesn’t have to issue/destroy its shares (i.e. enough buyers/sellers meet on stock exchanges without ETF having to chime in), no changes in the index and that dividend payments are sufficient to cover fund’s expenses, a distributing fund will have exact same number of shares of each companies forever. Expenses will be substracted from dividends and the leftover cash will be distributed to you and you do whatever you want with it, you can buy more shares of the fund or you spend it elsewhere, choice is yours.

An accumulating fund on other hand will not pay this cash to you, but rather buy more of the same shit it’s invested in. So over time its ETF share will represent ownership of a larger and larger number of shares of underlying companies.

If you’d choose to reinvest dividends received from a distributing fund back into the same fund, performance should be same as from an equivalent accumulating fund (module maybe minor losses on trading fees and spreads when you buy on exchanges, maybe some taxation differences). If you’d choose instead to spend the distribution on other things, then of course the total return will not be the same. It’s common sense, money doesn’t appear out of nowhere, no?

Mustachians, i would be very interested in having your views on the following questions. I am aware that some of the topics have been approached on different parts of the forum, therefore apologies if I am too redundant:

If you have 100 000 CHF at hand today for investing. How would you approach it? Would you invest it all at once as a lump sum or through progressive payments? I am aware that the lump sum approach is the most effective long term because of the compounding effect but I would like to know if you have different strategies and why. One of the reason to go for progressive payments could be to avoid the psychological distress of having bought everything at a peak even if this pays off long term

Do you think that today is a good time for investing a lump sum? Of course I am aware that none of you has a cristal ball to predict the future but still there has been a crazy growth in the markets during previous years and we can see some potential troubles coming in the Eurozone for the next 5 years (potential Italexit, Frexit, countries threatening to leave the EUR, etc etc). Is this something you would consider to have progressive payments and make sure you buy some shares at a lower price or you dont care about external factors?

I had a look and I guess it’s clear now. I took the NAV value directly from Vanguard’s website since the inception of VWRL (22 May 2012) until now and compared it with VT. I got exactly the same price return.

Then I had a look at the dividends and VT had around 0.23% higher dividend than VWRL. That’s the only difference. So I guess 0.14% comes from TER (0.25% - 0.11%) and the rest comes from the US withholding tax (15% * 50%?).

The last riddle was, why small caps make no difference. This should be interesting to @glina. A short reminder: FTSE Global All Cap (MCap $52 trillion) = FTSE All-World ($46 trillion) + FTSE Global Small Cap ($6 trillion).

Notice how the Global and the All-World practically overlap! And how Small Cap barely manages to outperform, then falls back in place. This is why VT and VWRL will have no relative price difference.

So where does the confusion come from? Well, @glina owns SPDR MSCI World Small Cap UCITS ETF. These are small caps only from developed markets. What is missing are emerging market small caps, which the FTSE Global Small Caps has.

To conclude, I think the whole exercise of owning small caps on top of VWRL is pointless. First of all, there is no matching ETF to fill the gap. Secondly, even if you found one, it does not outperform the VWRL. Just tell me, looking at the chart above, if you owned VT, would you still want to additionally own Small Caps?

What is better, get extra 0.23% and pay tax on it, or not get it at all?

Did you even look at the chart? Just compare the light blue (VWRL, Large+Mid) with the dark blue (Small Caps). Small Caps don’t seem to diverge from the Large+Mid, at least not in this 5-year period. I don’t have better data.

Thank you for the analysis. For the range you analyzed, this is indeed true. If you look at 3Y, the VWRL actually outperformed WOSC, but then at 1Y, the WOSC returned +100% over VWRL.

In any case, my basis was the long term performance (starting 2003) of underlying indexes. I can’t be sure about the future. Could be they will be 100% correlated from now on.

As of now, I only hold VWRL and AUUSI. My WOSC purchase is due in July to stick with my cost averaging regime. Until then I still have time to change my mind, but I don’t think I see an alternative.

Edit:

Another explanation to your riddle could be that EM Small Caps actually pulled the index lower. They performed poorly in last 1/3/5Y.

this is a nice discussion!

i’d like to only add the details that concernign small or value investing, literature says that the over-and under performance might take more than a decade to develop. bojak’s horizon up there is 5 years, which is not a suitable basis to do analysis on the small caps. but in case your investment horizon is that short, small caps might not be your first choice

I really like the approach of @glina and the mix of VWRL, WOSC (small caps) and Gold. Simple 3 ETFs approach.

Two questions (for everybody):

→ I am a bit worried about the low exposure to the CHF as I am planning to be here on the long term. If we look at the 3 ETFs portfolio on the blog, I like the fact of having some CHF exposures through the mid-cap CH (SMIM). It could be a nice way to replace the WOSC with a lower TER.

I am actually hesitating between

55% VWRL (all world)

10% WOSC (world small caps)

25% SMIM (Mid caps Swiss)

10% Gold

Or do you think that WOSC is an overkill and simply choose 65% VWRL / 25% SMIM / 10% Gold makes more sense?

→ In times of crisis, it is true that gold goes high but CHF too. AUUSI trades in USD. Therefore you may gain in Gold but lose from the currency side, hence suppressing the effect. I saw the ZKB Gold ETF trades in CHF but is much more expensive (0.3% management fee + 0.4% TER) and apparently lower return. Was it part of your decision making?

Edit: i have read @Bojack analysis and I should precise that my view is long term regarding small caps

Can you please show me a 20y chart where I can see that small caps outperform large & mid? I cannot find it. In USA there does not even seem to be a global small cap ETF, and in Europe there is only the Developed World one, and it’s a small one. Your strategy does not seem to be too popular.

I just had a look at the 5y and that’s enough for me. Small Caps return has a very high correlation with Large+Mid. I don’t see the point. Why the heck do you have to overcomplicate it?

If you want to squeeze a guaranteed 0.3% per year and have small caps included (not that it makes ANY difference), then just buy the US ETFs already…

The graphs also show the equivalent ACWI and ACWI Small caps so there’s enough data to make an educated guess how different combination would work out :-).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.