I just ran the numbers (% gain, including dividend):

18

50.5

35.8

6.2

3.9

3.8

3.2

-1.5

-6.1

-2.4

-6.5

Overall % gain:

8.9

So I’d say there’s no real losers (just yet anyways).

I just ran the numbers (% gain, including dividend):

18

50.5

35.8

6.2

3.9

3.8

3.2

-1.5

-6.1

-2.4

-6.5

Overall % gain:

8.9

So I’d say there’s no real losers (just yet anyways).

VT is +34% (ex dividend) since June, so I’d say you have some significant losers there.

I meant losers in the sense of huge loses against what I invested in specific shares. But yes, of course you are right if comparing to VT.

New to the forum, please allow me to understand some basic dynamics for my own benefit.

Having an account with Swissquote & Degiro is there a sensible way in deciding which one to pick if investing in ETFs that are available on both platforms. The simple answer would be to fill in the order form for 5k CHF and compare fees but what I do not quite grasp is that VT is denominated in USD while on Degiro there is the EUR version of the fund. As both should be identical what is the downside in holding it in either USD or EUR? As I would like to put some money in ARK funds which seem to be available at Swissquote only, but read a lot about low-fees at DEGIRO I could use a little help here.

Secondly, is there a point in breaking down VT in all world ex-USA & SP500, I would miss out on everything US based that is not listed on the SP500 right?

Much appreciated

Hello,

I will only answer to some of your questions as my knowledge is limited

First of all, on Degiro, you can’t purchase US domiciled ETF such as VT (Vanguard Total World Stock) or ARK ETF. This broker let you only invest in IE (Ireland) domiciled ETF such as VWRL (Vanguard FTSE All-World). Furthermore, VWRL can be purchased on different stock exchange (London Stock Exchange, SIX Swiss Exchange, NYSE Euronext, Deutsche Börse and Borsa Italiana S.p.A.). On Degiro you can purchased VWRL for free if you select the one which is listed on the NYSE Euronext (Amsterdam).

Second of all, on Swissquote you can purchased VT (US ETF) or VWRL (IE ETF) as you wish, but if you purchase VWRL on the SIX Swiss Exchange it will cost you less as it is one of the “ETF Leader” selected by Swissquote with a special price of 9 CHF whatever the amount of your purchase.

Hope this explanation help you a bit.

If anyone is looking for daily updated country weights: SPGM: SPDR® Portfolio MSCI Global Stock Market ETF

Made some rebalancing.

VIAC (24k)

30% World ex CH

30% SPI Extra

20% EM

17% SMI

ValuePension (22.5k)

80% World ex CH

19% EM

IBKR (33k)

100% USA

78.5k invested right now (-1k for cash at Viac/VP), so in total:

55k USA (63.6%)

11.3k CH (14.4%)

9.1k EM (11.0%)

9.1k Developed (11.0%)

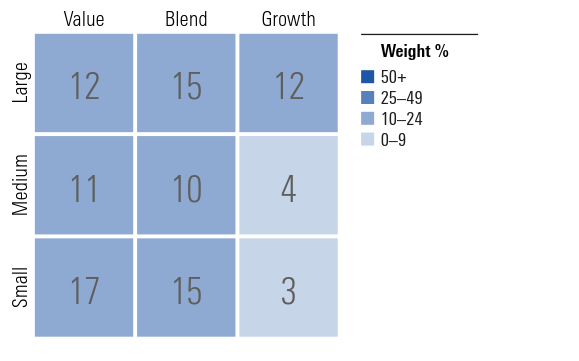

So I updated my portfolio to use Avantis ETFs with a small cap value tilt.

Morningstar style box (VIAC+Finpension is approximated with VT):

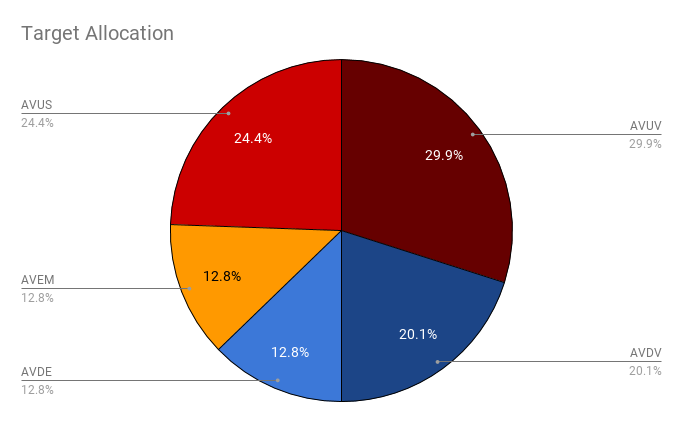

Taxable:

| Ticker | Name | Weight |

|---|---|---|

| AVUS | Avantis U.S. Equity ETF | 24.4% |

| AVUV | Avantis U.S. Small Cap Value ETF | 29.9% |

| AVDE | Avantis International Equity ETF | 12.8% |

| AVDV | Avantis International Small Cap Value ETF | 20.1% |

| AVEM | Avantis Emerging Markets Equity ETF | 12.8% |

Reference is MSCI region weights. Small cap value is 50% of the whole taxable portfolio. Cost is 0.26% per year.

VIAC+Finpension

| Region | Allocation | Fund | Allocation |

|---|---|---|---|

| Switzerland | 22.8% | CSIF SMI | 15.8% |

| CSIF SPI Extra | 5.9% | ||

| CSIF (CH) Equity Switzerland Small & Mid Cap ZB | 0.4% | ||

| CSIF (CH) Equity Switzerland Large Cap Blue ZB | 0.7% | ||

| World | 32.6% | CSIF (CH) III Equity World ex CH Blue - Pension Fund ZB | 28.7% |

| CSIF (CH) III Equity World ex CH Small Cap Blue - Pension Fund DB | 3.9% | ||

| North America | 22.4% | CSIF US - Pension Fund | 21.1% |

| CSIF Canada | 1.3% | ||

| Europe | 7.6% | CSIF Europe ex CH | 7.6% |

| Asia | 4.5% | CSIF Pacific ex Japan | 1.7% |

| CSIF Japan | 2.8% | ||

| Emerging Markets | 10.1% | CSIF (CH) Equity Emerging Markets Blue DB | 4.0% |

| CSIF Emerging Markets | 6.1% | ||

| Total | 100.0% |

Here is my global weighted average portfolio that I am starting with this year. Interested in your feedback

50% - SWDA - iShares Core MSCI World UCITS ETF

22% - EIMI - iShares Core MSCI EM IMI UCITS ETF

8% - WSML - iShares MSCI World Small Cap UCITS ETF

20% - AGGH - iShares Core Global Aggregate Bond UCITS ETF

Goal is to rebalance on bear trends, selling bonds and buying more stock.

Why eur hedged, and what’s your expected return? (Looking at same risk bonds in eur, I’m not sure it’s positive, besides the fx volatility for eurchf)

Just because all other ETFs I buy are bought in Euro, since the european exchanges have better volume in Euro. And such bonds, in case of bear markets, tend to have the least fluctuations, even to slight appreciate (although not guaranteed).

That’s not a very compelling argument…the currency you use to buy stock ETFs as explained multiple times is not very important.

If you live or plan to live in a EU country then it can make sense to hold EUR-hedged bonds. If you plan to stay in CH though the EUR-hedging would most likely add cost while also increasing volatility.

As I said, bonds will be used to balance the portfolio for above market average gains. The portfolio I made is focused only on accumulation. What would be a better bonds alternative if considering retirement in CH?

Cash might more stable with higher returns than equivalent bonds (at the moment, might change at some point). That works great for rebalancing.

Meaning all 20% allocated to bonds to be kept in cash. I thought of that, indeed. But not sure what is the best way.

You might want to consider US bonds instead such as USD treasury bonds if you don’t mind too much having USD ETFs. Yield is at least not negative for US bonds…

There’s higher risk though, and probably more correlation between corporate bonds and equity markets.

In general the theory is that the expected return after hedging should be the same as the equivalent return in bonds denominated in the hedged currency.

So expected yield of non-sovereign USD bond after hedging should be similar to expected yield of corporate CHF bonds of similar rating (which is barely above zero?). The main advantage of global bond hedged will be some extra diversification.

edit: and need to keep in mind what your goal is, usually that’s having a less correlated asset class, so if you’re increasing the yield but increase correlation with equity that might be detrimental to the overall portfolio.

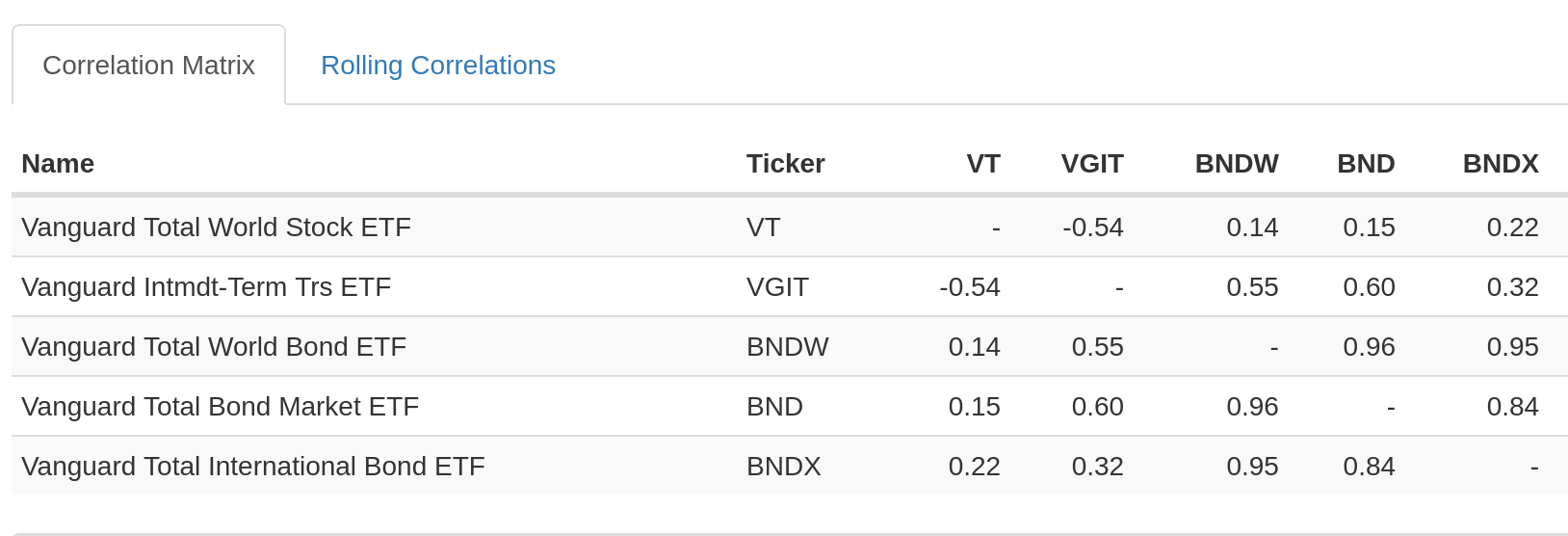

Agree regarding the higher risk… then regarding the correlation this is the reason why I would go for US treasury bonds (VGIT or VUTY.AS) which even has a negative correlation when compared to a world equity ETF like VT. See the correlation matrix below from portfoliovisualizer where I also added global bonds ETFs such as BND/BNDX/BDNW for comparison.

So maybe for less risk one should go for a global world bond ETF such as BNDW but then the correlation is higher with VT as the correlation VT<->VGIT.

But then US treasury bond have the same expected return as CH sovereign bonds after hedging (so pretty deeply negative). (and unhedged, it kinda defeats the purpose for people with no tie to the US due to the volatility, my understanding is that long term through interest rate parity even unhedged you’d expect same CHF return as the hedged one anyway, just with a lot more variance).

I don’t quite understand why a US treasury bond would have the same expected return as a CH government bond? For instance the 10 year treasury interest rate is at around 1.5% (Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis (DGS10) | FRED | St. Louis Fed) whereas in Switzerland it is more around 0% as far as I have heard (source missing). But I don’t have much clue about bonds, so I am asking here to understand better the differences…