I’ve been doing some reading as I want to use extra liquidity saved to diversify, hedge (and bet) a bit. 100% stocks or mix of stocks + bonds is comparatively far easier to understand. I can’t claim to understand more than the very basics around Futures and trend following, and nothing about how they’re managed so I am hesitant. The results do look good on backtesting but I’m warry of biasing myself by cherry picking what supports my current thought process.

Buffett, when asked about MFs said, in typical Buffett succinctness, that an investor is taking on the manager risk. This could be countered by also admitting that a BRK investor is taking on the Buffett risk, right?!

They look great on backtest and are not a new untested FOTM thing

The theory of holding uncorrelated assets lowering risks and volatility and increasing gains holds

Cons

Trend following bases its risk premium on (bad) behavioral aspects and external interventions (ie is not as quantifiable and/or reliable as Factors)

They are tax-inefficient (not a problem for us here, according to forum wisdom), and very expensive in terms of TER.

Thoughts?

Edit: I remain amazed by how good of a communicator Buffett is, as someone who’s very much in communication (consulting) I really value his ability to accurately answer questions, giving just enough insight to make the other person think (in the shareholder meetings he’s answering for free, in a way), but in essence giving a complete answer more or less every time. That’s including the ahhh, ohhh, and occasional mumbling.

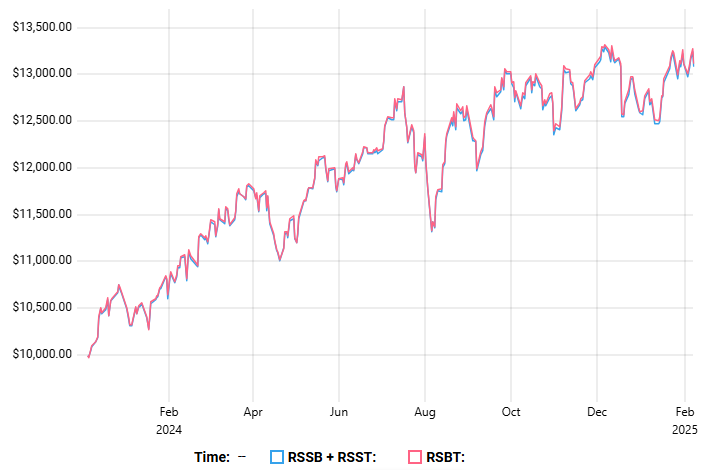

Excuse me, I do not understand if there is currency risk involved in RSBT?

I understand that for RSSB and RSST you buy stocks and with the rest of the currency you buy futures contracts for the VT, VOO or respectively the MF part. But as I understand for RSBT you hold approximately directly 50% of US Bonds ( iShares Core U.S. Aggregate Bond ETF (“AGG”)).

Isn’t then like 50% of the ETF not currency hedged for bonds, which one should never do?

Or is there no currency risk, because it can be seen as 100% MF and the 100% US bonds are just “accompanying” the investment?

The currency exposure is not really that important with such a fund.

Also the fund does trade currencies and if the USD is trending down, the fund will likely pick that up and compensate the currency losses.

Also basically all (non hedged) managed futures funds hold t-bills/USD cash as collateral. So will always have currency exposure. RSBT is not different from a currency exposure perspective here. These funds basicall all hold 100% USD.

But again they trade currency futures and are long/short on those depending on trend.

Some even trade CHF futures directly (kmlm for example)

-1x MF Collateral Replication (I think mostly short term treasuries or USD cash)

+1x Treasuries (1x USD, 1x US Treasury Term)

This is:

1x TF Strategy Replication

1x US Treasury Term (=> no USD exposure)

1x USD

I assume this will have some exposure to USD. But it is not fixed at long or short or how much. If your TF goes long S&P 500 futures, it will be short USD for the same amount.

I think there are two ways to think about this:

Plot the net exposure of the fund over time.

What kind of average trend following is replicated. Do those funds mostly look at the trend of single futures (many are pairs with USD), or do they also heavily look at trends across futures (and where do those trends occur)?

I can’t answer #2, but I can give a snapshot for #1. You can download the raw holdings on their website. As of today (2025-02-06) RSBT has:

Asset

Net Exposure

TF strategy

USD

175.03%

75.03%

AUD

-24.23%

-24.23%

CAD

-41.03%

-41.03%

EUR

-71.82%

-71.82%

GBP

-16.71%

-16.71%

JPY

-15.85%

-15.85%

US Stocks

22.51%

22.51%

Ex-US Stocks

53.87%

53.87%

Term

-64.23%

-164.23%

Energy

2.46%

2.46%

Metals

15.77%

15.77%

Let’s also have a look at DBMF:

Asset

Net Exposure

MF strategy

USD

213.55%

113.55%

EUR

-70.38%

-70.38%

JPY

-5.49%

-5.49%

US Stocks

22.76%

22.76%

Ex-US Stocks

11.50%

11.50%

Term

-97.86%

-97.86%

Energy

5.37%

5.37%

Metals

20.55%

20.55%

USD is quite high, but USD is also trending at the moment, so that’s something we want. But I can’t read if there is a USD bias from this snapshot.

I’m still unsure if MF funds consider their collateral part of their trend exposure. If they consider it part of their trend exposure, we would expect an average net exposure of about 0% to USD. The value USD is not trending as much as stocks. And about the same as other currencies.

I’m also unsure what the replicators regress against (regardless of what the regressed funds actually do). If they regress against 1x USD and 1x Strategy, adding a USD collateral to the strategy will yield the original fund exposure in any case. But separating this specially cut strategy and putting it on another collateral (e.g. RSST) will yield strange results.

I am just asking the following with regards to the currency exposure (neglecting rebalancing, TER and other side effects).

Will these two portfolios behave the same for a Swiss investor tracking in CHF or do they not because we have unhedged bonds? Due to the additional leverage involved I am not so sure.

First portfolio:

75% VT

25% RSSB

25% RSST (assuming RSST holds VT instead of a S&P500 ETF)

So for a rough equivalent you‘d need a 4th fund and reduce VT exposure and replace with VXUS. Else you are overweight on US stocks in the first portfolio.

That would translate to

100% VT

25% S&P 500

25% notional exposure to treasury futures (and these are more or less currency neutral, due to the nature how futures work)

25% managed futures overlay

On the second you‘d be 100% VT + 25% RSBT, which translates to:

So if you want to get rid of more currency exposure, but have it equivalent to the second:

~50% VT

25% RSSB

15% VXUS

25% RSST

Would cancel out most of the currency exposure from RSBT, but is more complicated.

Overall I wouldn‘t say it makes that much of a difference, but this would be more tax efficient (as RSST is more capital efficient) and have less currency exposure.

With the difference that RSST is rebalancing more or less daily, and that will keep you managed futures exposure always = RSST position, while with variant one it can float a bit more.

25% RSST (assuming RSST holds VT instead of a S&P500 ETF)

That is what I meant with it to neglect that RSST does not hold VT. But you are right, one definitely has to add something like VXUS to compensate for that.

Good point with the tax inefficiency of AGG, compared to the first portfolio. One should not neglect that. Yes, I can imagine the difference wil not be large, but I would have to backtest first to be sure.

The second portfolio has a missing 25% exposure to stocks (125% vs 100%). Fixing that, using S&P500 for the S in RSST, and adding an additional 1% interest on margin:

Assuming the overlay Ts have no currency exposure on average (lacking the regressed 100% USD collateral from the average fund), I calculate the following USD exposures

Have been snooping around the sex shop district of reddit investing (r/LETFs - the red light district would be r/wallstreerbets, r/options) and saw KMLM supposedly employs a 200 SMA strategy. Isn’t that way too long to do anything? I mean a year barely has 250 trading days?

I‘ll try to remember to find a podcast episode where the strategy was discussed in detail and the rationale for KMLMs longterm signal.

But in general, there are different approaches on how to do it. KMLM is specifically longterm trend only. The data also shows that longterm trends are really what gives the big returns.

There are other funds that incorporate shorter signals and most of the time a blend of signals.

What the advantage specifically is of longterm: keeps trading costs very low, as you do not switch from short to long and back frequently.

This also keeps preventing a lot of the whipsaws you can get (meaning a short term trend in one direction → dund goes there and then a short term reversal, where you are on the wrong side, this for example helped the fund not crash as much in the Yen Carry blowup and quick reversal)

Especially in crazy volatile back and force phases this can help prevent losses.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.