Since there are many expats here, I wonder if someone could explain how difficult/easy is to invest in housing on another country. It could be the near France/Germany, where we can buy a condo and give it to an agency or manage ourselves, or far away in Thailand.

Rinch already commented on his experiences in France and GB here. So that is a good starting point!

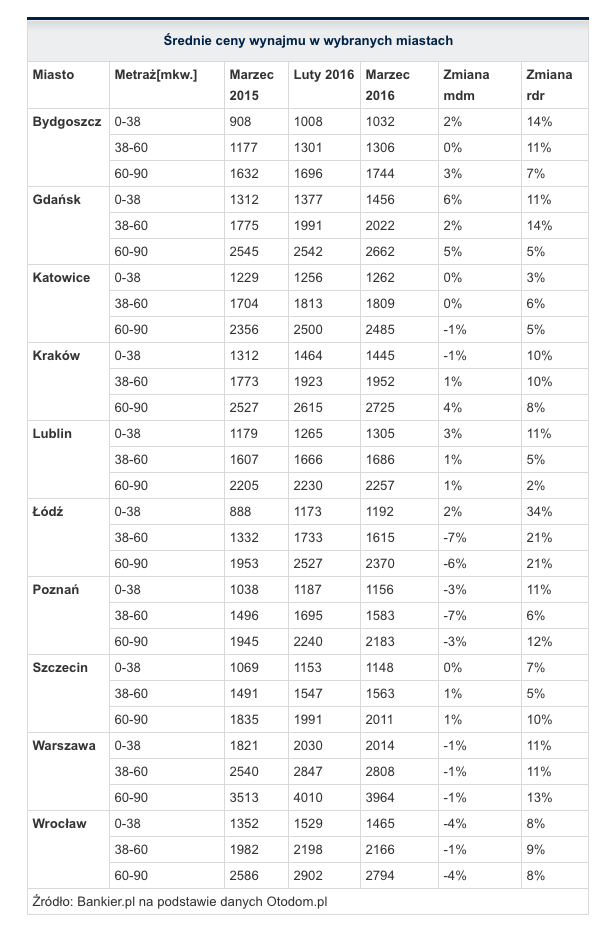

I also had some friends saying that the Renting market in Poland looked very interesting (regarding brut margin), especially in Krakow… if any Pole of the forum could confirm it, that would be nice as well

The rents are generally rising as Warsaw and other big cities are growing economically, but the prices of the apartments are going down for last 7 years. Here you have the apartment prices on first chart and land price on the second chart: https://www.pb.pl/ceny-mieszkan

I don’t know how interpret that, but in the early 2000’s we had a boom in the housing market, then it went down (maybe it was a small bubble?) and now it seems more or less stable. The land was growing all that time though.

Having bought two apartments in France and the UK, here is my take on it. The first thing is that with property it’s really difficult to build a really accurate financial model before you start. In the UK you need to get a certified gas safety engineer to inspect your property every year. Maybe you wouldn’t have realised that so didn’t account for it in the model. When a neighbour applied for planning permission to build a house next to my apartment in France our syndicate voted to hire a lawyer to oppose the decision. It’s also really hard to estimate how much you’ll spend on upkeep. How long before that old kitchen needs replacing?

Second is that transaction costs are huge. In France it cost me around 10% of purchase price for all the fees. It’s certainly a barrier to flipping property if you decide you want the money for something else after a few years. You’ve got to be in it for the long haul.

Third is that one of the reasons why property is attractive is leverage. Your deposit of 20% gets you 100% of the rental income. As you pay off the capital your return on equity will steadily get worse.

Tax is an absolutely huge one. In the UK the first 10,000 income is tax free, so if your income isn’t that big you might have nothing to pay at all. In France you’ll have property taxes plus, income taxes. For my airbnb place I’m under the Micro BIC system so 50% of my gross income is taxable at 20% (ouch). Watch out for rule changes too! In the last few years the UK changed the rules so that mortgage interest payments are no longer tax deductible. All the people who bought buy to let property with big mortgages may now have to pay a high tax bill even though the rent only just covers the interest wiping out most of the profits. What about capital gains? In France you will pay 19% capital gains tax, 15.5% “social charges” and an additional charge if the gain was large. All in all probably around 40% (double ouch).

I have never really considered using an agent to manage the property. They will probably take 10% of your rental if you rent on an annual basis and 30% for holiday rentals. This seemed a good way to wipe out the entire margin to me so I do it myself.

Overall, it can certainly work but you really need to do your research and make sure you account for everything.

Don’t underestimate how pathetically poor that country is, you might buy a condo in thailand but you might never be able to sell it again without a huge loss

In general i think one should do real estate in places where you can physically easily reach, should any problem happen and where you understand local market and rental laws well, it’s highly varying from country to country and very pro-tenant in some countries. Also take into account various taxes.

Over the past 10 years i have bought 3 condos/lofts in Toronto where property values have gone crazy (similar to Australia and UK). So crazy in fact that the rental income ‘return’ is not worth the equity sitting in them so i have decided to sell them all and invest the net profit in index funds. One just sold for more than double the purchase price which is nice but not normal since properties really are only supposed to go up with inflation, so you must ensure you really are geting a very nice net profit on the rental income. Canada has 25% cap gains tax + 5% real estate commissions on selling plus closing costs so i will definitely net out positive but if it weren’t for the unusually high capital gains i’d be way under water. i have read that you’re supposed to get 1% of the curreent value of the property in monthly rental income to be a good investment (and not expect capital gains in your model). While everybody on this board will (have) say this is totally unreasonable, i do think it is a good yardstick for comparing against an alternative like index fund investing. If you want to read the 1% article let me know.

How can you say this without specifying what is the interest rate and the inflation rate? In Switzerland the annual rent is about 3-4% of the property value, in Poland it’s 5-6%. I think it really depends on the location.

It is a basic rule of thumb to find out if a real estate renting investment is worth it. Using it, you understand quickly why people invest more in real estate in USA than in Switzerland for instance…

This was in interesting read, but I still believe the 1% rule is complete nonsense for european standards. For USA it’s maybe ok. First of all, she mentions something like replacing the garage door etc, so she’s talking about houses. I guess they have more overhead. In flats I cannot see how you could generate 50% overhead. Moreover, American houses are made of wood and siding, I guess are cheap to make and not very durable. Finally, in USA you have this real estate tax which can be about 2% of the property value annually.

I don’t get it why she insists on calculating the number of years the purchase pays itself off. She should be talking about something like ROIC, because that’s what you can compare to, say stocks or bonds. She could say: so you get 12% gross, but 6% is cost, so 6% net. And then she mixes mortgage in. Mortgage is leverage of your invested capital.

Well, but do they? Can you link an example? I think real estate development in Switzerland is pretty solid. Wherever I look there are some blocks of flats being built. Swiss real estate prices are high and the rents are low, but you can leverage them with a very cheap mortgage (1%), whereas in USA the mortgage cost is around 3-4% if I checked correctly.

Btw this page shows the huge disproportion of return over the World, but US cities have the highest rates. I’m not sure if the things I mentioned explain this anomaly in full, but I don’t believe that there is some kind of untapped market in the USA. Would be happy if someone offered a full explanation.

Hi, I would not look to buy in high taxed European countries, go somewhere more Emerging Market, somewhere where landlords are protected by a well designed and abided law and where you can see the environment changing. I have found Singapore and Taipei to be great places for such endeavours as they all have long term city planning which works and for an investor it’s something like real life SIM City which pays you rent and appreciates in value. Check out the Singapore URA plans for instance (https://www.ura.gov.sg/uol/master-plan.aspx?p1=view-master-plan). Another great long term plan can be seen in Shanghai (https://www.tripadvisor.ch/Attraction_Review-g308272-d554654-Reviews-Shanghai_Urban_Planning_Exhibition_Hall-Shanghai.html) where I feel the best time to go long has long past though. Other interesting places could be Bangkok, Jakarta or Manila (more uncertain though). For more established countries, try to look at Australia (e.g. Perth) or New Zealand (Auckland, Wellington, Christchurch, Queenstown - which can also have other upsides in case of global crisis, geopolitical negative events or pandemics spreading). Exploring these options could be combined with a nice vacation trip! There is definitively more dynamics with such investments than in our hemisphere.

Technically speaking, both of them are not EM, but developed markets. I think what you meant is that it is better to invest in RE in countries with strong private property protection (so that our investment won’t get confiscated by governments or other local mafiosos) and that have strong economic and population growth, so that there’re better long-term prospects for renting or sale with profit.

As you say, when looking into an investment we should look at the yield of this investment. let us not talk about mortgage, because you can involve leverage in any investment.

In the article she interprets the 1% rule a little bit differently, but the 1% rule says nothing else that “Look for rental investments with at least 12% gross rental yield” (1% per month => 12% per year). Which after taxes and overhead lead to 6% net I guess (But this is not compounded but linear yields).

I still think this is a very healthy way of proceeding : you want to buy at a price low enough, and with rents high enough to have a fair return on investment. And yes, we can find a lot of these opportunities in American cities (not all, as you relevantly pointed out). I know for sure that in France these kind of opportunities, although rare, are doable.

In Switzerland (or let’s say Zurich because it is the only part of Switzerland i know well) it is far out of reach. If I look at my appartment, I pay 1500 CHF rent per month and similar apartments sell for 800’000 CHF! That makes a meager 2.25% gross rental yield. Pfew.

I’ll give you that point : In Zurich there are a lot of buildings being built currently. But who get the profits? I don’t think it is the investor, with the ridicule rental yields. In my opinion people dreaming of having their property buy over-expensive houses or apartments, and the ones getting the real money are the promoters… and of course the banks with all the mortgages they are providing!

Don’t forget that Switzerland taxes more properties than the U.S

The apartment is included in the wealth tax and depending on the canton you also have a property tax.

The income from the apartment will be taxed as income. Capital gain will also be taxed in a lot of canton

But if this rule of thumb is only applicable to a couple of american cities, then it’s not a very good rule of thumb, is it? Even in a city like San Francisco, you will fail miserably to find real estate that meets the condition.

Counting 6% for overhead seems a lot. Does a 1m CHF apartment in Zurich generate 60k annual overhead?

Some years ago I bought a new flat in Warsaw for 70’000 CHF and put 20’000 CHF to furnish it. Over the last 10 years it did not rack up any considerable costs. It could rent for 450 CHF net / month (6%) and the utilities cost 150 CHF / month (2% on top). That’s 8% in total. To keep it in good condition would cost roughly 75 CHF / month (1%). So this gives a true return of 5% per year.

I think you can’t answer this question without considering mortgage. I imagine Gemeinschaften and rental developers are in permanent debt. Maybe they bring in 20% and the rest is paid by the bank. So you pay them 3% rent on a flat worth 1m, but they only invested 200k capital. On the remaining 800k they pay interest of maybe 1.25%. So in the end they collect rent as 15% of the invested capital and pay 5% in mortgage. I don’t know how it looks in reality, this was just a product of my imagination to demonstrate the effect of leverage.

US property tax is often close to 3%. The Swiss wealth tax is something like 0.1%?

Well, that means that San Francisco is a terrible city for rental investments. Of course you can still speculate and hope that real estate prices will go up there no matter what, but I would not be so willing to take that bet…

Depending where you live i guess you should pay as well income tax on the rent. if i am not mistaken, in Poland it would be 19%… That makes a 243 CHF per month net, so 3.2% net if you start from 8% gross. In the article and in your example, half of the yield have been eaten by overhead and taxes.

Yes but if you use leverage then you can not compare it anymore to other potentials investments. I could do the same with stocks, buying for 100 but putting only 20 on the table. If the stocks goes up 10% then my equity goes up 50%! But of course if the stock goes down 20% then i am wiped out.

And, although Real Estate cycles are slower, Real Estate prices DO go down from time to time… Remember the US in 2007 or Paris in the nineties (-40%)…

With current stratospheric prices in Switzerland and tiny interest rates, the guy going into real estate only for capital gains might be in for a painful surprise…

So for the moment i compare investments without using leverage to compare apples to apples

Yes, the worst wealth tax you could have with a 1M home would be a 0.67% in canton Neuchatel…Which, if we take again my example of 2.5% gross in Switzerland on rental income, gives a tax of 6700 CHF, compared to the 25’000 CHF of rent from a 1M CHF house…

Rental income in Poland is taxed with a fixed 8% rate to encourage people to actually pay this tax. I guess more than a half of people rents illegally.

OK, I agree. So I guess you could say, in countries with cheap mortgage, the real estate prices are inflated by people leveraging their purchase. Looking at it this way, all the tax incentives for purchasing a home are such bullshit and do more harm than good.

Another reason why Swiss real estate is overpriced could be that the supply is too low (and that’s why so much is being built). And the third reason could be all the rich people who treat Swiss real estate as a safe way to preserve wealth.

On a side note, did you know that Swiss banks can pawn in a house that they already use as a collateral to a special institution and get fresh money to offer to customers as loan? Seems like a really risky game to me.

With the bonds yielding negative, banks and insurances use RE as an alternative investment, thus inflating the market (here in TI they’re building like crazy and vacancy rates increase year after year → people who want to rent have more choice and prefer to move to newer apartments, prices being equal).

This is one of the reasons why I’m so hesitant taking the plunge (and won’t probably do, at the end…)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.