I recently opened an IBKR account and started investing in ETFs. I’m still very new to this, so I have a few beginner questions.

I began by buying shares of the iShares Core MSCI World (EUR), which focuses on developed markets. I can purchase this ETF in both EUR and CHF, and the fund itself primarily holds assets in USD. My first question: if I buy 10 shares in EUR and another 10 shares in CHF, then later sell all 20 shares, can I choose in which currency I will receive back the money? Will this involve extra costs?

Second question (investment advice): at the moment, my portfolio only covers developed markets. Which complementary ETF would you recommend to diversify further? I’m investing for the long term, with monthly contributions.

Final question: are there ETFs that are generally more convenient to buy in CHF—for example, to reduce currency exposure or hedging costs?

You can’t choose the currency when you sell (at least I’m not aware of a broker that allows that). However, if it’s the exact same fund and share class (same ISIN), you can instruct a broker to e.g. change the EUR position of that ISIN into a CHF position without any trading. Swissquote charges a flat fee of CHF 50 for that (per position). If the position is large enough and you would otherwise pay high currency exchange fees, this could make sense. However, if you only have a few EUR shares and your broker offers reasonable exchange fees, just convert the cash after selling the funds.

An ETF tracking the MSCI EM index would be the obvious choice. And maybe a small allocation to an SPI ETF if you want a home bias, but this is completely optional. Check justETF for a good overview of ETFs. There are various other ETFs (maybe different asset classes such as real estate, gold/commodities, bonds) you could add but I can’t say what makes sense in your individual case.

I’m not sure what exactly you’re asking. Trading currency on its own is irrelevant (except for currency exchange costs). I would advise against hedged ETFs with the exception of bond ETFs (if you want international bond exposure). Currency exposure and ETF may be useful to you.

What speaks against just buying an ftse all world/ msci ACWI etf, that tracks the whole world including emerging markets?

Gets rid of the need to rebalance, as well as psychological benefits such as not questioning the choice if one region outperforms etc. One-and-done solutions, if they exist for your needs, should be the prefered option in my opinion

SPDR’s ACWI fund SPYY (large and bigger mid-caps), is available in CHF at a low TER of 0.12%. Or SPYI that also includes smaller mid-caps and small caps (with sampling though, so not full replication currently, may be in the future when the fund gets bigger) for 0.17% TER.

For FTSE all world (large and mid cap companies) exists Invesco’s FWRA for 0.15% and Vanguard’s VWRA for 0.19%.

Should all be available to buy in CHF at many brokers. Also more convenient to have them accumulating, to not get USD dividends distributed.

Yes, I was curious about what happens when you buy the same ETF (same ISIN) in two different currencies. From your explanation, I understand that the gains and losses are tracked separately for each currency. This also means that I could choose to sell, for example, 5 shares purchased in EUR and 7 shares purchased in CHF, and receive the money in their respective currencies. Is that correct?

Yes, I was probably not clear, or maybe I just don’t know enough. I will make an example. I own several shares of IWDA, which I bought using EUR. Is there any downside to buying the same ETF using CHF? Should I target a different ETF which is more advantageous?

The MSCI World (developing market) consists of 70% US.

The MSCI EM consists of 25% China, 19% Taiwan, 15% India.

The FTSE all World consists of 59% US, 5% Japan and 3% China.

When I look at this number, the combination MSCI World and MSCI EM looks more diversified than the FTSE all World. What is your view on this?

MSCI World + MSCI EM is the exact same (in the right relative size, which would be about 89% world +11% EM) as just having MSCI ACWI (all countrie’s world index).

FTSE all world is very similar to MSCI ACWI, the difference aren’t meaningful for this dicussion.

The equivalent to MSCI world in FTSE indices would be FTSE developed markets, there US also has 70% weight.

Adding 11% MSCI EM to 89% MSCI World, gives you about the same weighst as here

It’s a matter of how much EM you would add to change those weights. But that would be discretionary from your side and if you would want more China for example, you’d overweight it compared to market cap of the world.

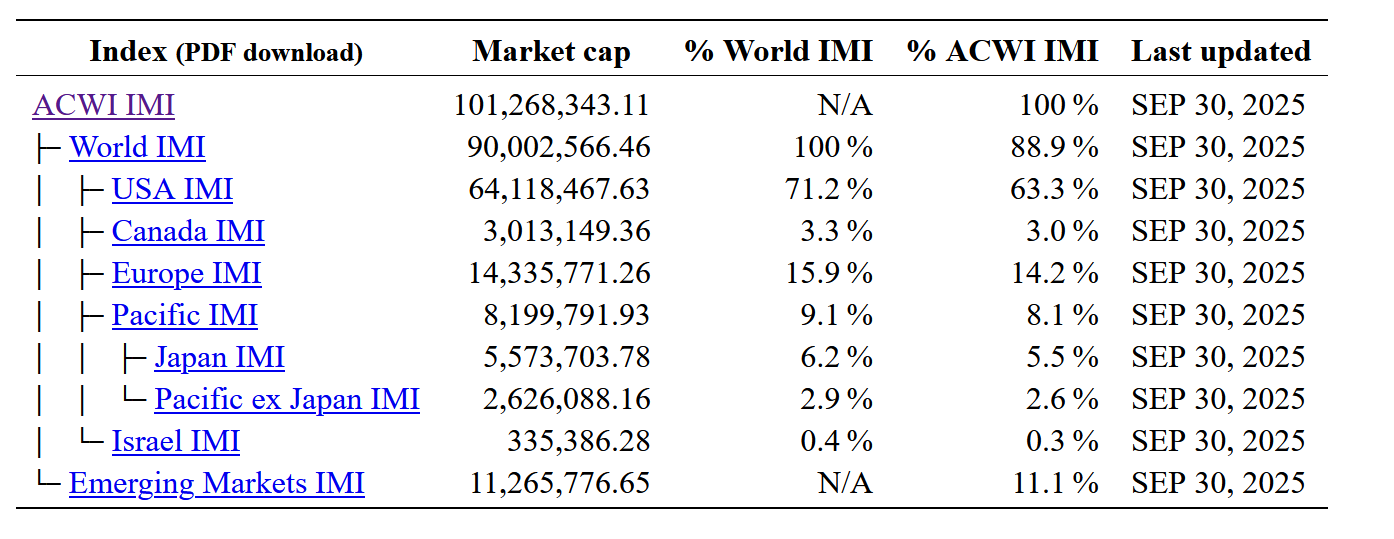

You can see the market caps of the various indices on this site: https://marketcaps.site/

IMI is the investible universe.

Yes, the EUR and the CHF listings of the same ISIN would show up as separate positions at your broker and when you sell, you pick one or the other (or both, but that would be two independent trades).

There are no substantial differences as you still invest in the same fund. Your broker portfolio overview would look slightly more complex and the broker might calculate profit/loss differently due to different trading currencies (but the actual profit/loss in CHF would be the same for both). The trading fees and spreads at SIX may be higher. On the other hand you save currency exchange fees. Overall, it mainly depends on your broker and the exchange, not the currency.

IWDA is not the cheapest MSCI World ETF with a TER of 0.20%. I myself would go for an ETF with a lower TER, either UBS Core MSCI World (0.06%, only the distributing variant is listed in CHF, though) or straight to a ACWI or All-World for a one-fund option that is still cheaper than 0.20% as @Tony1337 has already mentioned. Currency-wise, I don’t think you need to target anything else. You can add a bit of Swiss stocks if you like but global companies domiciled in Switzerland are still heavily exposed to other currencies, so don’t expect Swiss stocks to be immune to exchange rate fluctuations.

That’s strictly talking about stocks. 100% stocks may or may not be too risky for you. And for bonds and also real estate, you should definitely pay attention to the currency.

Yes, I understand now. Holding both the MSCI World and MSCI EM ETFs provides more flexibility in how to balance developed and emerging market exposure. This approach essentially replicates the MSCI ACWI while giving you the option to adjust the allocation DM vs EM later if your strategy changes.

Looking at fund sizes on JustETF, it seems that most investors prefer to invest in the MSCI World and MSCI EM separately rather than in a single MSCI ACWI or FTSE All-World ETF. I know this ultimately comes down to personal preference, but, out of curiosity, what is your perspective on this?

Yes, indeed, this is a good point. Essentially, it doesn’t matter whether you buy the MSCI World ETF in EUR or CHF. When you sell the shares, you’ll receive the money in the same currency you used for the purchase, which was my concern and is now clarified.

What would make you change strategy and why?

Seems to me just a recipe for psychological stress if you already plan now to potentially change strategy down the line and maybe at bad moments etc.

That it doesn’t matter if more people prefer to split their funds.

A lot of that is probabaly also institutional money.

I just don’t see any reason why one should put any relevancy on how others split their allocations, as long as the ACWI/FTSE fund you choose has enough aum.

Cheap all country world etfs are also a lot newer and therefore haven’t had the time to attract as much aum.

There is likely no right or wrong here, the funds I mentioned are all very similar. The most complete ucits offering is probably the SPDR MSCI ACWI IMI (SPYI), because it includes companies of all sizes. The others do not include small caps.

@Tony1337 I’ve looked into the topic a bit more over the past few days, and I now agree that VWCE/VWRL can be a better and simpler choice compared to manually splitting between emerging and developed markets.

I have one additional question regarding VWCE and VWRL. As far as I understand, the only difference is that VWCE is accumulating while VWRL distributes dividends. Since I’m relatively young (31) and investing with a long-term horizon (planning to reinvest the dividends anyway), I’m leaning toward VWCE. Is there anything else I should consider when comparing these two ETFs?

Another simple question: I’m currently trading mainly in EUR, since I’m temporarily investing only through my 3a pillar in CHF.

I recently bought some shares of VWCE, which is traded on XETRA in EUR. If I’d like to buy the same ETF using CHF, should I buy VWRA, which I believe is the same ETF but traded on EBS?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.