I have one topic that keeps my mind busy for quite some time. Bring my currency exposure and ETF investments in line. My main currency exposure at the moment is in CHF, due to salary and main expenses. I also have expenses in EUR, but no income in EUR. Then I invest in the US ETF, so another exposure in USD.

I read about the long term currency impact on ETFs and that it is not that significant for long term investments. But I am also thinking about my midterm plans and how to secure the right strategy for myself, especially in EUR.

So what I am considering at the moment is having some ETF in EUR, but here is again the currency risk aspect that bothers my mind. I selected IMEU that is traded in EUR and has a 50% EUR exposure. But then when I look at the performance of VWRL that is traded in EUR and has a 60% exposure in USD, it is just performing much better than IMEU. So what is better? To cover my EUR exposure via IMEU (or any other ETF with a large EUR exposure) or to cover it via VWRL (any other ETF with a large USD exposure). Kind of performance vs. currency fluctuation dilemma.

Maybe somebody has some the same thoughts or could help me to understand what is better? Maybe I am completely wrong and I need to look at this from a different perspective.

Forget about trading currency of equity ETF products.

When two ETFs are quoted and traded in different currencies but hold the same shares of the same underlying index/companies, what will be the difference in performance between the two? It will just correspond to the exchange rate between the two currencies.

Don’t think of it as covering “EUR exposure”.

Rather think of it as investing in European companies/stocks

Holding stocks of European companies doesn’t necessarily mean positive currency exposure to that European currency. Think of a global, Swiss-domiciled company such as Nestlé, for example. It makes most of its revenue outside of Switzerland - and probably outside of Europe, too. The more the Swiss Franc loses value against other currencies, the better your Nestlé stock performance in CHF would be.

So basically what you are saying here is that it does not matter if I go for a US ETF traded in USD and when needed I do a USDEUR spot trade? Because eventually underlying currency is USD, so an ETF in EUR will not help me much. But at the same time, an ETF focused on the European market and traded / exposed mostly to EUR will underperform vs. US ETF? Thank you

Absolutely. I agree with you on the international exposure of these large companies. But the FX aspect of ETF really interests me and I think I still don’t understand it completely

Thank you very much for your thoughts. I totally agree with you on fees and duration of the investment. Having a cash reserve for expenses is essential and I am counting that one in. This whole topic is in my head, because of the uncertainty I have. Like if I stay in Switzerland for my whole life or move to another country in the Eurozone. And i mean like in 10 years or maybe even 20 years. So I was trying to think strategically and cover this possibility with a smaller investment in EUR portfolio. Just to be more secure in case USDEUR exchange rate will be not that great and I will not want to touch my USD investments.

But more I think about this topic, more trading fees, higher TER, lost opportunity and Taxation of dividends disadvantages I see in my EUR portfolio idea.

That is something I did for myself as well. I keep like 70% of my investments in VT, with large US stock exposure. Then like 20% in IMEU, with major EU exposure and 10% in CHSPI with mostly CH exposure. This is mainly driven by my currency appetite, as I honestly think that geopolitically all 3 regions are so globally dependent that if something goes wrong in one region, other 2 will be impacted.

But now I think about this strategy and it feels like having the last 2 for currency is just me losing the better returns of US stock due to my FX fluctuation fear

Thats a combination of less diversification and luck. Can certainly continue, but can as well reverse. If you ask me - you can add in some CHDVD but I wouldn’t go beyond 20% of your total Swiss Exposure.

If you want a more diversified bet, buy a combination of SPI plus SPI Extra, SPI Min Volatility, CHDIV and Credit Suisse’s non-weighted SPI ESG. Like 20% each. That would probably give you the best return you can get… but its probably a bit complicated

I was actually thinking about the whole Swiss and European exposure and somehow it feels discouraging to focus on these two markets. I know that many other ETF have a heavy focus on the US market, but eventually US stock has a better historical returns than European and Swiss one.

I am now thinking about some ETFs with world exposure (so mostly USD underlying currency), but traded in CHF/EUR. The whole FX exposure topic confuses me, but having some smaller fund in these two currencies somehow makes sense to me.

Most bloggers go for VT or other USD ETFs, but I have my doubts about future FX rate fluctuations and potential losses caused by the need to sell my stock and convert it to CHF

I think the fixation on trading value is wrong. I see what PF did to my VWRL that I sent from IB to them. They “changed” into anoter Ticker, but it’s basically the same ETF. It shouldn’t be a big deal, right? But then why they didn’t give me the VWRL.CHF Ticker? If I got it correctly, the only difference would be a neater PF interface, that is I would only see my belongings all under CHF instead of a bit CHF and a bit EUR.

The difference between this topic of the exposure and my post about CHDVD (or SPI etc), is that the underlying stocks are all in CHF, like the dividend they give. Probably just a laziness thing (no USD to exchange in CHF) or/and fear (no ETF part to sell to get some money ).

What about the dangers of currency pegged to another one. In this case it would have been bad to buy an EU ETF when the CHF was pegged to the EUR. Since USD/EUR and CHF are not pegged, I don’t see the risks.

You chose an MSCI World ETF among them. As you said: "some ETFs with world exposure (so mostly USD underlying currency), and…

…such an ETF traded exists: Amundi offer a EUR-denominated MSCI World ETF: FR0010315770 - and it’s been around since 2006.

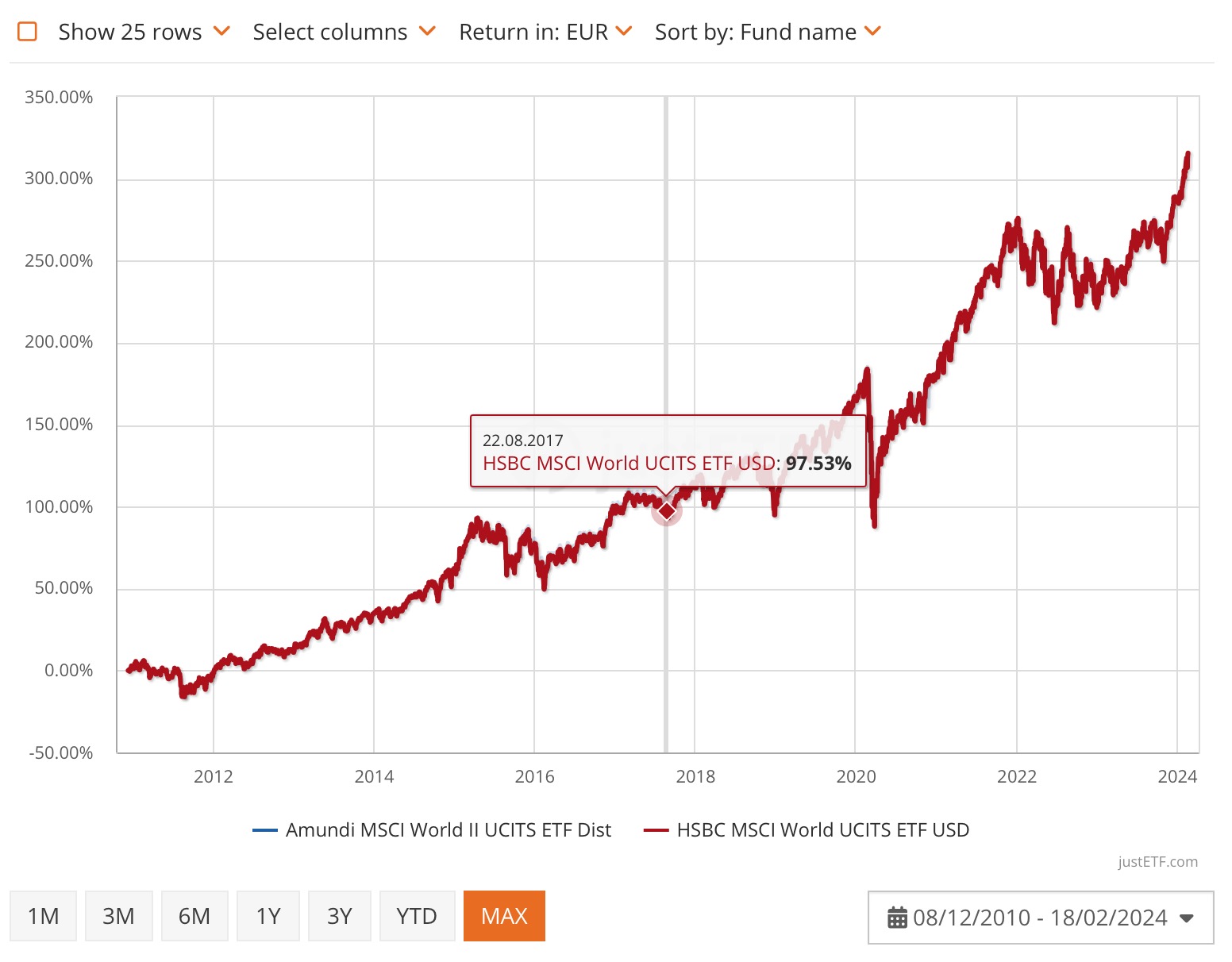

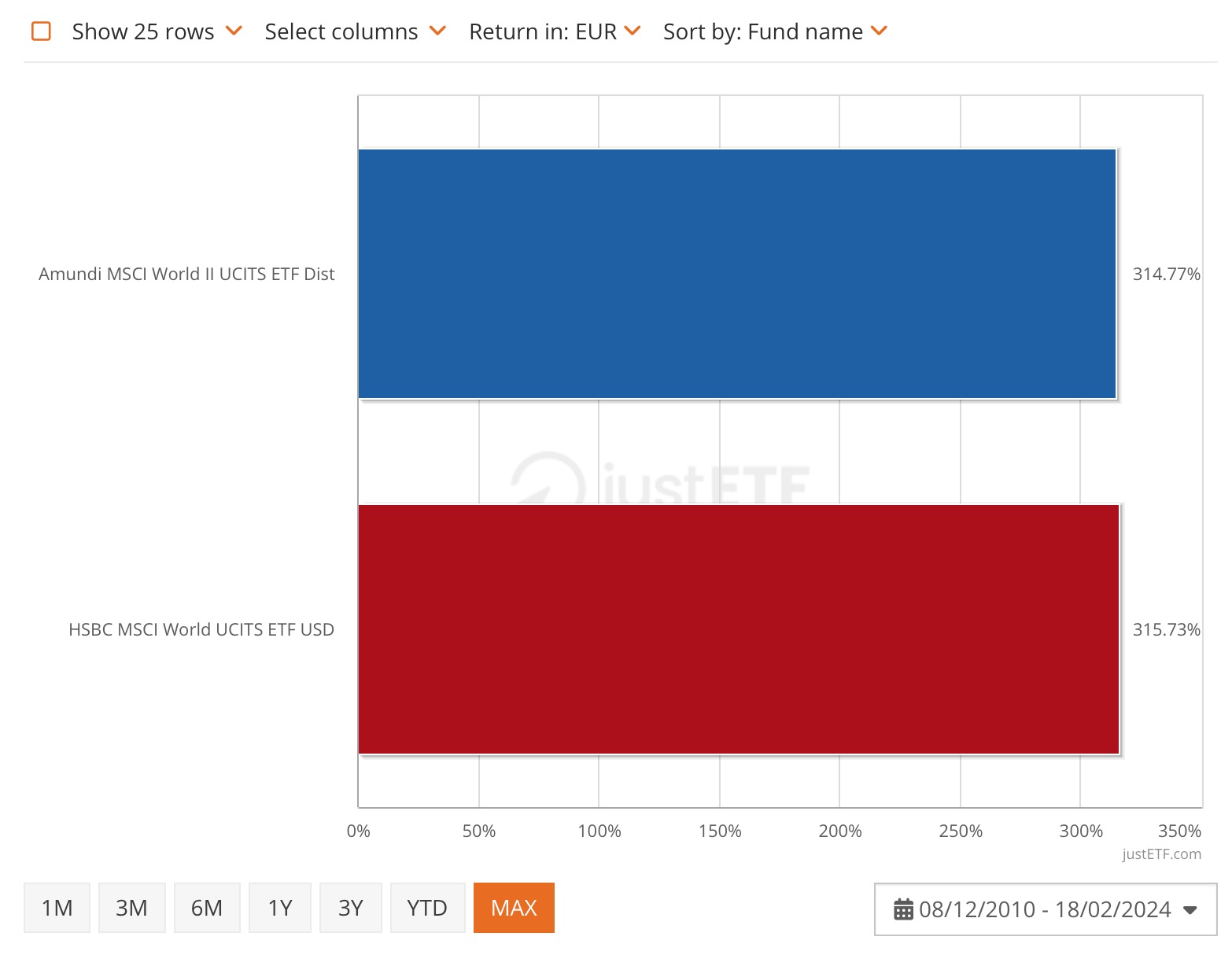

You can add them to the comparison and compare them against the USD-denominated HSBC ETF that tracks the same MSCI World index. This is what the difference in performance in EUR over the last 13 years looks like (Admund’s EUR-denominated ETF in Blue, HSBC’s USD-denominated ETF in red):

These graphs basically show the difference between…

a) Having bought an ETF traded in EUR 13 years ago and selling it in EUR today vs.

b) Having exchange your EUR for USD 13 years ago, buying an ETF in USD, selling it for USD today - and then converting back into EUR

(disregarding taxation, which is basically the same on both, and transaction costs (negligible difference), while reinvesting distributions)

Obviously for currency conversion - but arguably still negligible in the grand scheme of things, when it a round trip can be had for 1% or so.

Are you going to worry about 1% or 2%, after having received a 315% return?

That said, that’s looking at it from a long-term holder perspective. Recurring currency conversion when shifting your portfolio multiple times will eat into it more.

Admittedly, I too may feel some pain when paying 1 or 2% costs on a six-figure portfolio transaction. But ultimately, as your net wealth grows, you should realise it’s not that important. It’s the equivalent of a trading day’s performance.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.