BRK’s PE is meaningless because under accounting rules they have to account for movements in their unrealised gains and losses in its investment portfolio - obviously this injects so much volatility that the earnings figure is now useless.

You now need to separate out the operating income from their businesses from their investments to get a useful picture.

Ah, so these two ETFs implement Quality factors, but keep the weights of industries (compared to the standard MSCI World) intact, hence “Sector Neutral”.

Perhaps there’s a reason there are no non-neutral Quality ETFs?

Sorry yes I meant the Avantis funds are capturing value and not quality. Two different approaches both of them potentially outperforming VT. For me the quality index is slightly preferred over the active value approach by Avantis, hence I am looking for such an ETF.

iShares can change the index it follows for any of their fund!

MSCI has multiple indices with ‘value’ in its title. Nothing stops it from launching similarly titled ‘enhanced quality’, ‘select focus quality’ indices in future, and ETF providers jumping onto new indices.

Not sure the “index” label (or any of its creators’ labels) can guarantee there is a 100% non-active approach involved.

Say SP600 (SCV variant of the famous SP500) - afaik a board decides what gets in and out.

Yes there might be some thresholded metrics and certain principles involved to pre-feed them, but there is certainly a human active decision too.

Is it the only definition of quality? (I don’t think so)

Can MSCI change their mind and rules (for better or for worse) without permission of iShares and you (the investor) - Yes

Can MSCI come up with new indices to target quality? (I think Yes, given they have multiple indices for Value).

Can iShares change the fund mandate from one MSCI quality index to another MSCI (or non-MSCI) quality index. (Yes)

DFA / Avantis are systematic active with their own definition and rules of quality / profitability that they try to target by including strategies coming out of the research they fund, some of which is likely published. They are not 100% transparent, but that is their business model.

You are looking at MSCI Quality vs DFA/Avantis from the lens of Cap weighted / passive index vs traditional active (one man/woman’s discretion). That is a wrong way of looking at it. Both of them are neither truly passive nor traditional active in the

Both MSCI Quality and DFA/Avantis are active. You can choose whose definition and implementation of quality / profitability you like / trust more.

There is not a single reference to any data in your reply and you summed it up by stating “to me” - i.e. your unfounded opinion. You might be happy with VT, that is fine. Investing in just the Market is suited to the majority of investors. And actively managed funds do historically not outperform the Market.

However various Factors have consistently outperformed the Market. They haven’t been “arbed away”.

If you take the time to read my earlier posts in this topic, you can refer to the actual data I provided from as early as 1978 on the annualised returns of some factors over various rolling periods. It isn’t “recency bias” - although you can argue that about Momentum factor, which isn’t one we discuss.

Your arguments are quite weak and you don’t substantiate them.

Warren Buffet, Charlie Munger, Mohnish Pabrai, John Templeton, Howard Marks, Joel Greenblatt and a few others prove otherwise. All of them beat the market in the long-term. Of course that’s a tiny fraction of managers, nevertheless it’s not 100% of managers that lose the game trying to beat the market.

Someone who thinks you get more concentration risk when trying to diversify over more risk factors cannot be reasoned with.

The top 10 of VT are already 20% of the index and you are the vast majority in large caps. You get AWAY from concentration risk with having parts over more capitalisations/factors. Also you are still fully exposed to the market factor anyway…

It’s clear they are on a biased crusade against factor investing (whyever this is the case) and you can give them any data and they will ignore it.

Also @Compounding arent you investing in managed futures/trend following? Those by definition try to outsmart the market… you aren’t even true to your own statements.

Factors are very much alive and always have been in international developed and emerging markets. Not as clear the last decade in the US, but I still think they are there as well. There is so much data on this.

Look at performance of VWO or ishares EEM vs AVEM or AVES just as a recent example.

For 3a, my starting point of thought was MSCI World. Value Weighted looked like a step away from US mega cap tech & other growth that has outperformed everything in last 10-15 years without going into vanilla value which can have negative momentum loading. Value weighted is then ‘another way’ to capture value using similar metrics and RAFI funds.

I wasn’t thinking of ‘set and leave’ portfolio, but rebalancing once a year or when it moves 5-10% in either direction

I am slooooowly warming up to the idea of buying a profitability / quality only factor fund. Ideally it would be a combined quality + value fund. But in case of finpension 3a, having value weighted + quality seems like a decent option.

Note: I am aware the the any global quality fund contains a lot (I mean really a lot) of tech and healthcare that have done well in past decade. the same thing that has been putting me off.

And in 2023’s letter, Buffett specifically and categorically called Munger the “architect of Berkshire Hathaway”, again categorically noting that it was Munger who pulled him away from Ben Graham, cigar butts and pure value investing.

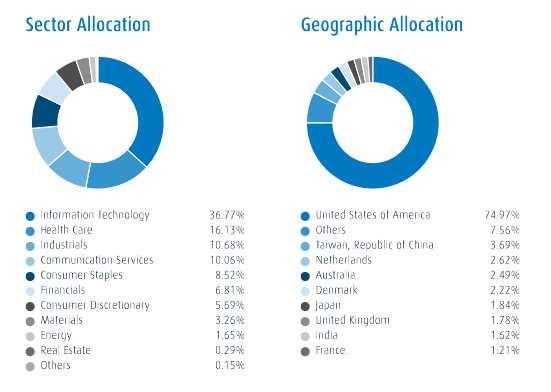

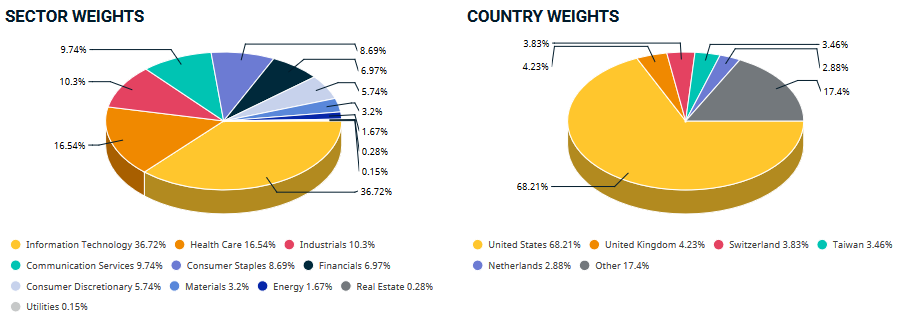

Sectors for quality seem to be similar enough, but the USA is weighted even stronger. We can also see that EM is included (ACWI = World + EM). The Sectors differ much from the standard MSCI ACWI.

I also add MSCI World Quality to the comparison. All index data is taken from those factsheets. It is GTR (Gross Total Return) in USD. ZGQ is inclusive its dividends before L2TW taxes on them.

Year

ZGQ

MSCI ACWI Quality

MSCI ACWI

MSCI World Quality

MSCI World

ETF

GTR

GTR

GTR

GTR

2023

32.33%

33.03%

22.81%

32.97%

24.42%

2022

-24.03%

-23.42%

-17.96%

-21.90%

-17.73%

2021

22.42%

22.50%

19.04%

26.10%

22.35%

2020

24.06%

25.38%

16.82%

22.73%

16.50%

2019

35.75%

35.96%

27.30%

36.70%

28.40%

2018

-7.92%

-6.95%

-8.93%

-5.06%

-8.20%

2017

27.86%

29.02%

24.52%

26.64%

23.07%

2016

5.05%

6.08%

8.48%

5.12%

8.15%

2015

0.29%

1.98%

-1.84%

4.25%

-0.32%

AVERAGE

12.87%

13.73%

10.03%

14.17%

10.74%

GEOMEAN

11.06%

11.95%

8.90%

12.54%

9.60%

Looks alright. We got 3% additional performance for the indexes. The ETF still managed to get more than 2%. The index hugging MSCI World Sector Neutral Quality only got about 1%. I would have done a more direct comparison, but that data was NTR.

Additional thoughts

Canada is not ideal from a tax perspective. The USA will take their unrecoverable 15% L1TW on the majority of all dividends. Which would have been avoidable by having a US domicile.

Then the Canadian government takes another 15% on everything. If you can convince them that you are entitled to the reduced 15% withholding taxes, else you pay 25%. Possibly a broker can handle that for you.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.