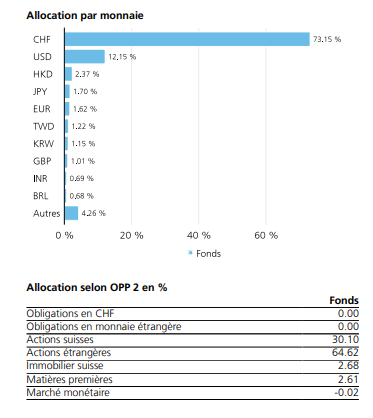

If Frankly is hedging 70% to CHF then it’s a big negative long-term performance impact.

3 Likes

Sorry, I wasn’t clear. 70% is in CHF, but this also included Swiss stocks.

Around 60% of foreign stock are hedged, which like you and I said has a big impact on returns

Thanks for the comparison.

Where did you get this information from? Could not find it on the website/faq.

Thanks

It’s an assumption on the parameters it’s written automatic invest as soon as the money is deposited.

But right, it’s written nowhere.

1 Like

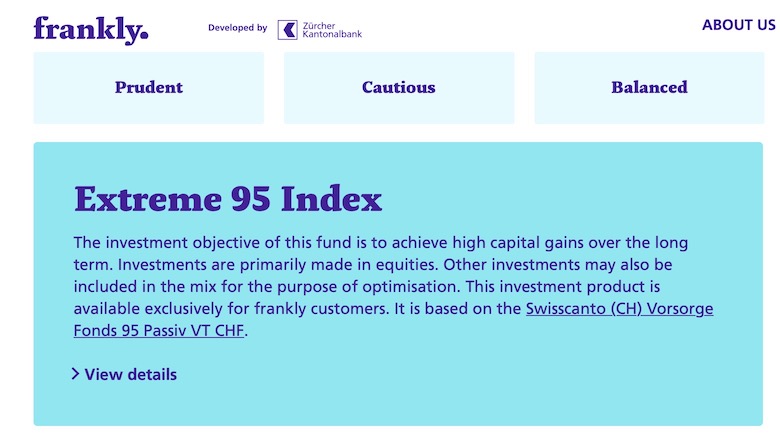

“At least 51% of the fund’s assets are invested indirectly via target funds based on the fund-of-funds principle”

https://products.swisscanto.com/products/documents/kiids/CH0511961424/KIID_CH0511961424_CH_EN.pdf

Am I missing something? ![]()

EDIT: Link corrected to VT units, but same wording

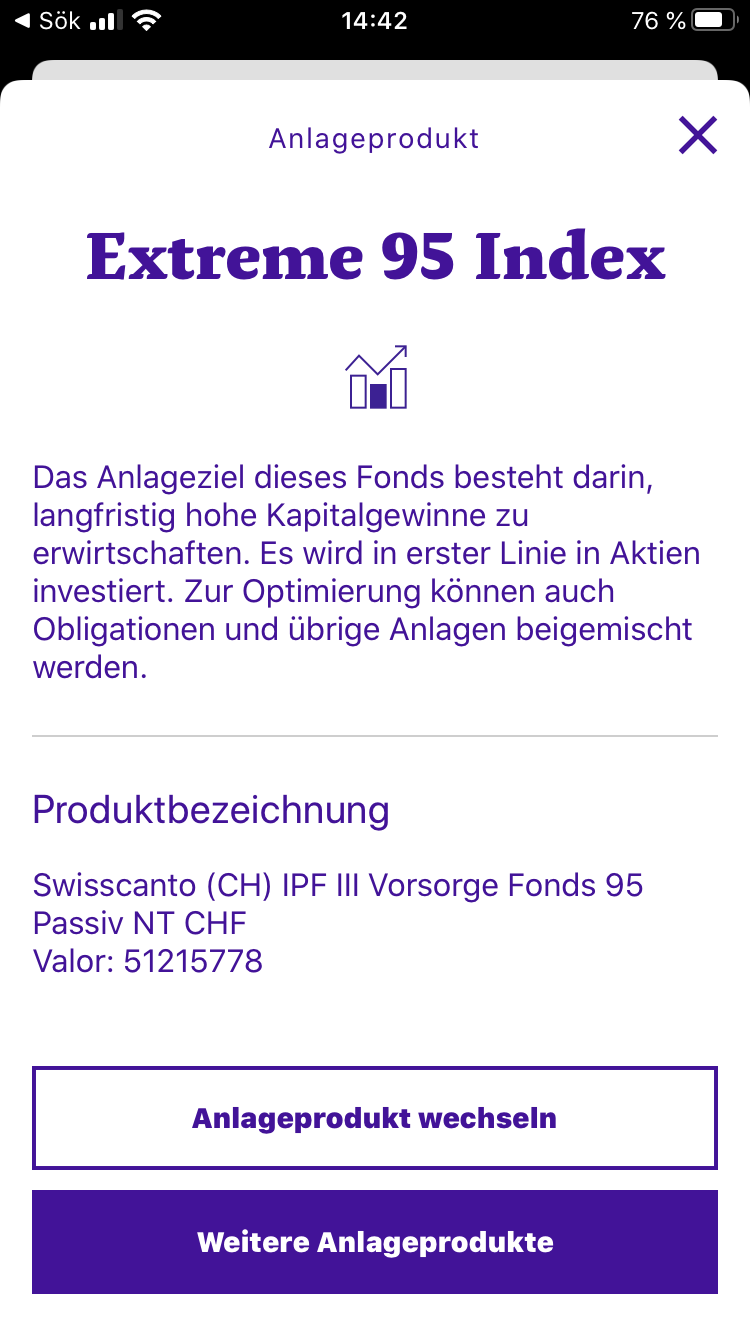

If I understand correctly, it is NT not VT that is used by frankly.

I agree. But my girlfriend is using VIAC 100%, so I am considering to have some of my 3a with frankly. The reasoning is just to never have everything in one basket. What do you think? You can call me stupid if you want.

@wapiti

https://twitter.com/frankly_zkb/status/1240925548836196352?s=21

I don’t get their response. How should one ensure to have the sufficient account balance when everything is invested in the automated investment mode (can be chosen in the app).

@OrientExpress

Yes, NT is the correct share class. After checking again, it seems to be a fund of a fund, but the current structure has no impact on the fee.

It seems, they are using:

- Swisscanto (CH) IPF III Index Equity Fund MSCI® World ex Switzerland NTH CHF

- Swisscanto (CH) IPF III Index Equity Fund MSCI® World ex Switzerland NT USD

I agree with not all the same eggs in the basket, but 3a is quite secured.

There answer is not clear, I would assume they sell to have liquidity for the fees.

Yes, hedging will have a big impact

Agreed - based on the research above as well as frankly’s website, VIAC still seems to be #1 choice.

1 Like

One aspect which I believe has not been discussed is the fact that Frankly charges 0.48% on the total amount of assets. If you for some reason choose to only invest 50% in a fund, then, well, the fee is still on the other 50% cash too (aka negatives rates). That’s a huge limitation. You can really only be 100% invested in Frankly, holding cash would be very expensive.

I maintain it is the VT units:

- Its IBAN CH0496470938 is part of the link on frankly’s investment products page, please also refer to the screenshot below.

- Swisscanto’s detailed sales prospectus states as such: “Anteile der Anteilsklasse VT CHF sind thesaurierende Anteile, bei denen die Beteiligung den folgenden Institutionen der beruflichen Vorsorge (2. Säule) und der gebundenen individuellen Vorsorge 3a vorbehalten ist”

PS: OK, the web site does give conflicting information, according to language version:

German language version referring to NT units

French language version referring to VT units

English language version referring to VT units

Seems frankly a bit amateurish, for a supervised financial product by one of Switzerland’s most reputable and largest cantonal bank (pun intended), after all that pre-launch hype they tried to create.

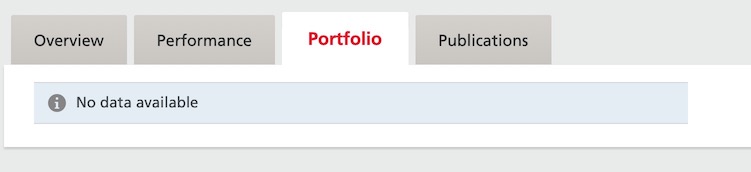

Also, the fact that “portfolio” data is unavailable for the funds on Swisscanto’s web site doesn’t inspire much confidence in me.

PPS: Ignore the first part of this post. They must have quietly changed in on their web site, and the German version might still have been in my browser cache, indicating the NT units. However as of right now they are linking two different fund units (NT and VT) on their german version:

“Details aufrufen” is still linking to NT units as I’m writing this:

…whereas the text link in the preceding paragraph links to VT units.

Okay, it’s a mess then. Inside the App if I check the account details it says NT as well.

NT would also correspond to what they write in their FAQ:

Is the administrative fee and the TER (Total Expense Ratio) of the funds available in frankly 0.0%?

The administrative fee is included in the all-in fee and is therefore 0.0%. The frankly investment products may also invest in Swiss real estate funds for income reasons. These exchange-traded funds in turn affect the TER. This means that the 0% cost funds used by frankly can also have a TER between 0.01% and 0.03%. In order to avoid charging you twice, we set the all-in fee lower accordingly from the outset. We promise to review the TER of real estate funds annually.

It’s the same for (for example) Moderate 45 Active:

https://products.swisscanto.com/products/de/Produkte/BVG-3-Anlagegruppen/Gemischt/CH0238052978

https://products.swisscanto.com/products/de/Produkte/BVG-3-Anlagegruppen/Gemischt/CH0497631165

Sure, their wording of the “investment product” “being based on” the RT/VT unit class fund doesn’t mean that’s exactly what I’ll be getting (which might in fact be NT). But frankly, I might be too lazy to inquire further. Just tell me straightforward what fonds my funds are going to be invested in. ![]()

The past performances of the NT class are the same as the VT + fees. At the end, it’s always the same fund. The classes are just created to apply different models of fees between the customers (individual, pension funds, institutionnal, ect).

Their answer seems quite weird. Because the fund hold 2.5% of “ZKB Gold ETF AAH CHF” with a TER of 0.40%. So technically, you will pay twice the fees.

Sure enough.

The difference is in the fees.

And that’s the exactly question: Which one am I getting and which fees will I be paying?

Cause fund-of-fund structures charging fees more than once isn’t exactly unheard-of.

It doesn’t need to be that hard and confusing to tell (and advertise) to me.

Also, it shouldn’t be that hard to find more about the portfolio I’ll actually be getting than just that:

Found this in-depth review: https://investinghero.ch/frankly-zkb-3a-review/

Most of the things have been discussed here already. But the screenshots might be helpful if you want to get an overview.

“you’re correct. The real estate funds do have an impact on the TER of 0.00%. This impact is around 0.01% to 0.03%. That you don’t have to pay any fee twice, we’ve set the all-in-fee already slightly lower. Regarding the Gold funds, there the issue has been resolved.”

Answer from Frankly, so I was right. The real cost is higher than 0.48%

However it’s don’t understand the second sentence.

Also, don’t know how they have “correct” the gold ETF issue.

My answer to the last question: ““we’ve set the all-in-fee already slightly lower” Lower than what?

Is the total cost 0.48% +( 0.01% to 0.03%)?”

Their answer “lower to 0.48%. The total cost will be 0.48% + 0.01% to 0.03%. If you have any further questions, please refer to our FAQs https://frankly.ch/en/faq.html”

For me, the 0.48% all-fee cost is not the reality. Advertising this number is misleading.

Either I’m dumb or more probable they don’t understand their own product. If someone understands their answer, please explain ![]()

3 Likes

I don’t get it as well. Thanks for being so persistent and asking them on Twitter.

I started a standing order that will be first executed on 1st of April to gain some experience. Maybe we’ll understand better then.

The AGBs are more clear:

Der Vorsorgenehmer ist eigenverantwortlich dafür besorgt, dass sein Kontoguthaben einen für die Gebühren- und Kostenbelastung hinreichenden Saldo aufweist. Andernfalls ist die Stiftung ermächtigt, zur Schaffung der erforderlichen Liquidität allfällig vorhandene Wertschriften des Vorsorge- nehmers zu veräussern, wie wenn der Vorsorgenehmer der Stiftung einen entsprechenden Auftrag hierzu erteilt hätte. Hält der Vorsorgenehmer zum Zeitpunkt der von der Stiftung initiierten Veräusserung mehrere Wertschriftenanlagen, werden diese anteilmässig veräussert, basierend auf dem jeweiligen Gegenwert in CHF.

1 Like