You can only pull it out when you officially retire (ie: not RE), so currently that’s minimum 58 years.

Yes, you get a discounted rate when you pull it out (1/5th of normal income tax rate).

But with the upcoming swiss vote on retirement reform, the whole situation might change…

That’s exactly what might change if the new law passes. If you don’t work anymore, then vested benefit accounts need to be closed at official retirement age (65 currently), which then become taxed once upon closing (at 1/5th of income tax rate), and every year thereafter (as wealth tax).

Well a lot will change in the next 30+ years. Maybe withdrawing several 3rd pillar accounts in different years will be taxed the same as withdrawing them all together.t

That’s exactly why I’m still not sure whether 3a or voluntary 2nd pillar contributions are really worth it until shortly before retiring (or in case of buying property).

I really regret not having dumped all my 3a & voluntary 2nd pillar contributions into VT…

you save income taxes (for me it’s around CHF 1’500 per year)

no wealth tax

income such as dividends in 3a is not taxed

With today’s solutions (finpension, VIAC, etc.) you can have up to 100% invested in equities and almost replicate VT, and in most cases it’s a no brainer to contributre to 3a.

Makes sense. However, since you are due taxes when withdrawing 3a, you pay taxes on the whole compounded stock-growth, which might be huge if you contributed 3a since your 20ies. But then again, you can counter that disadvantage by having various small 3a accounts, correct?

And: What about early voluntary 2nd pillar contributions? Depends on your income, i guess?

Gross net worth (so everything included, including real estate, for which I’d use an imputed rent to calculate my theoretical expenses - so not too flashy a home but one on par with the one I currently rent). I’ll adapt when I reach there if I realize my taxable resources can’t carry me until normal retirement.

As stated by SwissDan, the vesting benefits account is for between the date of (very) early retirement and the one at which 2nd pillar funds become accessible. The actual date of withdrawal of the vesting benefits account depends on the availability of taxable money (or lack thereof) and tax optimization.

That’s a different assessment to make since you can’t invest them freely before early retirement, self employment or leaving the country. If you need more “fixed” income in your allocation, I’d take it there. If you want more stocks or other assets, that would not be an option with regular 2nd pillar (no idea about 1E plans but those have other limitations, like investing horizon since they would have to be rolled back into a regular 2nd pillar plan if you change employer and the new one doesn’t offer a 1E).

Yes, but the withdrawal tax rate is pretty low in comparison, e.g. in ZH if you have 500’000 you pay around 37’000 and if you split it in 5 accounts with 100’000 each, you pay around 25’000 in total.

Or as a separate asset class by itself. I have run an analysis of my 2nd pillar returns (there is one data point per year, so not many of them) according to this template:

And here are the results: CAGR 2.85%, arithmetic rate of return 2.86%, annualized volatility 1.1%, correlation coefficient with MSCI ACWI IMI in CHF 0.9!

If one thinks about it, it actually makes lots of sense that the returns of the 2nd pillar are strongly correlated with stocks market returns. It is not relevant that the 2nd pillar returns are always positive, even if the stocks market return are negative. What it says is that the 2nd pillar return tends to be higher than average if the stocks market return is higher than average.

So not a bond and not a good diversifier. 2nd pillar decreases volatility of your wealth, but it is not going to provide you with more than average return when the stocks market returns are bad.

To be prudent I exclude locked investments which are bound to increasingly expansionist monetary policies.

If your 2nd pillar still has a significant value at retirement age, it’s great. Just don’t include it in your planning. I consider it as a bonus.

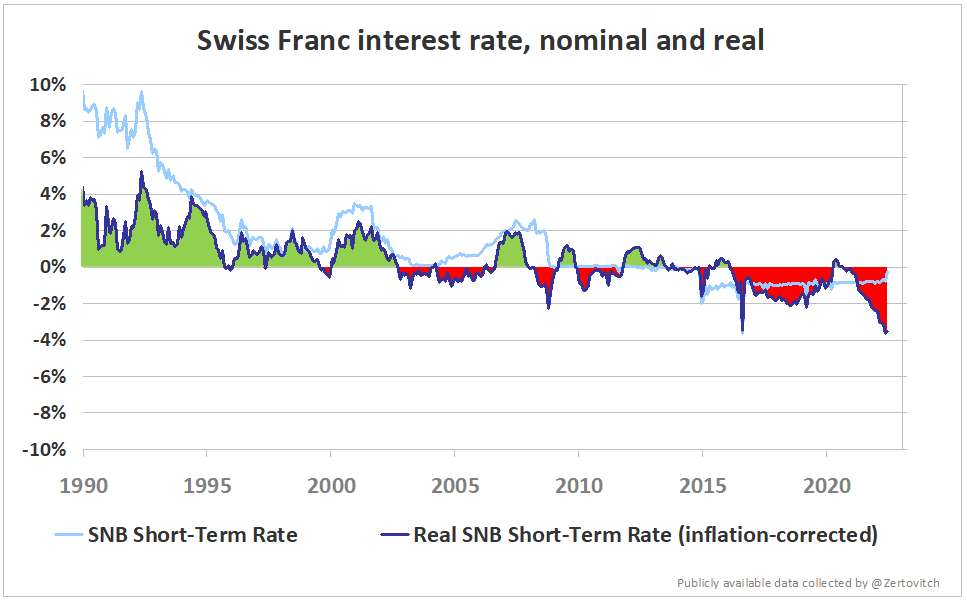

The interest paid by pension funds is typically higher than the SNB short-term interest rate, though. Before 2022, inflation was below 0.5% p.a. for quite some time (rolling average over 5 years) while minimum BVG interest rate was at least 1% p.a… Difficult to predict how it will be in the future but the chart above is irrelevant, in my opinion.

Just because an investment loses (or is expected to lose) value is not a good reason to exclude it from your net worth.

Even if you have limited control over your 2nd pillar, it’s still part of your assets. Wouldn’t it be better to count everything, taking into account asset allocations (e.g. equating 2P to bonds while in pension fund) and expected return of all your assets?

Also, you can choose to allocate your 2P to stocks if you stop working, use the money to buy a residence, or reduce taxes via buybacks. These possibilities impact your asset allocation and expenses and both are key aspects of FIRE.

From the ‘expansionist monetary policies’ perspective, why stop at the 2nd pillar? If you go into that rabbit hole you end up with crypto and gold bars only?

2nd pillar money has a) limited ability of generating above inflation returns and b) restrictions against access:

The first you can mitigate post-FIRE by investing it at e.g. VIAC, from that point until full withdrawal this should not be a negative. In fact there may be financial advantages in that phase as well, as discussed already in this forum. Pre-FIRE it is what it is, so lets get to FIRE asap, shall we?

The second is more tricky, here we either need some basic trust that politicians don’t screw it up and nationalise / merge into 1st pillar bevor we can withdraw the cash or emigrate in time… I don’t expect this to happen, but if you have 30 years to go this might be a risk you need to mitigate somehow.

It is the same rabbit hole as the SNB, which describes its own policy as expansionist since the mid 1990’s. And clearly the trend is (in order to stay, for good reasons, consistent with the ECB and the Fed): more of it!

and some stocks and rental real estate (with a mortgage, you get on the right side of the monetary policy (taking a mortgage was suggested by Mario Draghi at an ECB press conference!))

Article about taxation of Kapitalbezug at normal retirement age of your 2nd pillar (choosing one-time capital payout instead of monthly pension).

gives a nice overview of current tax rates per Canton for various amounts.

discusses potential competition between Cantons resulting in possible reduction of today’s tax rates in future (don’t count on it, but on the other hand this “competition” between cantons did already result in a strong reduction in inheritance tax in the past decades).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.