Hello. I am a 40yo swiss resident with some assets invested in ETF on postfinance e-trading, plus all the 3rd pillar on VIAC. I am currently mostly exposed to VWRL, but I would like to allocate some money to a safer option and take advantage of the high interest rates of the short term euro money market. I do not care about EUR/CHF currency risk as I plan to spend a portion of my savings in euro anyway.

The latter can be bought on SIX, where it is quoted in CHF. This is good as I’d avoid converting the currency. But it makes me suspicious the fact that this ETF has apparently very rare exchanges on SIX. Why is that? Is there anything that makes it unsuitable for a swiss investor, apart from the unhedged currency risk?

Another option I have is to just move my VIAC assets to a similar asset type, but I don’t see a clear option that gives me exposure to short term euro money market.

I think the currency risk is reason enough that this is not a suitable investment for the average Swiss resident. And I guess that many people (or institutions) who want to invest in EUR bonds / money market, will do so using a broker with low currency exchange fees, in which case one might as well trade on an European exchange where liquidity will be higher (and exchange fees lower).

Also keep in mind that there are ETFs traded on SIX that are perfectly suitable for Swiss investors but still have relatively low volume (e.g. VEVE).

If your reasoning for investing in EUR money market is that you anyway will (also) spend EUR in the future, why do you think it’s better to exchange CHF to EUR when selling your EUR ETF instead of already exchanging CHF to EUR now when buying the ETF? I.e., you anyway have to do the exchange at some point, it seems reasonable to me to do this when/before investing in the EUR ETF. You’d likely want a foreign broker for that, though.

Assuming you don’t want to particularly bet on EUR, i.e., we assume the interest rate parity holds for your investment period, it would be better to invest in CHF bonds from a tax perspective. Have you already seen this wiki? Short guide to CHF fixed income options

Well, I can buy the SMART ETF on SIX in CHF at roughly the same price that I can buy it on XETRA in EUR. Does anybody know whether it’s possible to sell an asset on a different market than the one it was bought from? So I could in the future sell the ETF on XETRA for EUR and save on the terrible currency conversion fees of postfinance.

I know that IB would be much better but I’d prefer not creating another account. Apart from currency conversion, Postfinance is fine for me.

It’s possible in principle, as long as the share class (ISIN) matches. At Swissquote you have to pay CHF 50 + MWST for this (Börsenplatzwechsel). It might be the same at PostFinance, although they use a different term (Depotstellenwechsel). I would guess that’s the same thing but I’m not sure.

Hi,

If I understand correctly, if I left more than 10K€ in cash on my IBKR account, I will get 3.48 or 2.48% for the month so nearly the €STR minus the IBKR margin ? By the way how to identify the version of IBKR Pro or Lite ?

You basically get the daily accrual of the ecb overnight rate. So 4%/365 - 0.12%/365 cost = 3.88%/365

Check the graph on what it does.

The accumulating version is just a straight line up and the distributing version accrues for a year and then pays out the interest.

When you sell, you sell for more than you bought, corresponding roughly to above formula x amount of time you held.

So example: you buy 1 share for 100 at 01.01.2024 and then hold it for 6 months, it has ca. a value of ~102€ (slightly more than 3.88%/2, as it does compound on itself) on 30.06.2024

Unfortunately not. It‘s like any other interest/dividend in that sense. And handled like other accumulating funds as well.

You‘ll find the etf on ictax.

Of course if you buy it and hold it for 6 months, then sell, you have not held it technically on the dividend date and no capital gains tax. But this is the same as with other accumulating funds.

yes, that was my understanding. As long as I don’t receive any dividends and only use accumulating version to buy/ sell then there should not be any capital gains tax.

Sounds an interesting option for a high liquid euro deposit. I will definitely have a look at it.

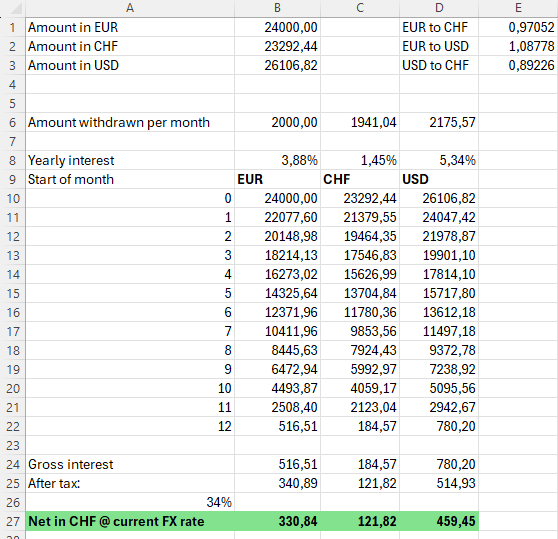

Let’s image to start with 24’000 EUR, I was expecting that the final amount (in any currency) would be always the same, because of the currencies being efficient.

That’s what I learnt from this forum: if USD is returning 5.34% it also means that it is losing value agains CHF (which is returning only 1.45%). So, in the end, the only difference between short term investing USD or CHF will be taxes.

I ran a simulation on Excel and what I found is contradicting the above statement:

I start from 24’000 EUR, that are converted using yesterday’s FX rates and then invested. During 12 months I DCA and at the end I pay taxes. Finally I convert everything to CHF.*

Surely there is something wrong in all this. Because if it was like that, today I could buy 1000 USD with 890 CHF, make it compound at 5.34% and convert it back to CHF earning more money than what I would make sticking to CHF only.

*I know in 12 months the FX rate will be different, but not that different that 121 CHF will be equal to 514 USD!

That’s likely true only over larger amount of time due to FX changes. You can’t assume that over shorter durations.

(and yes, there’s expectations that USD should continue losing value over time, but there can easily be some +/- 5% over short period of time that will trump the interest rate differential, that’s the main reason why fixed income is usually hedged)

You forget the depreciation of the principal vs CHF. The efficient market hypothesis suggests that with this rate differential EUR is expected to depreciate by 0.2% per month vs CHF. So:

EUR interest per month: +0.32%

EUR depreciation vs. CHF: -0.2%

Result in CHF: +0.12%

CHF interest per month (yes, you have guessed it right): +0.12%

Now add to this the fact that income is taxable but the capital loss due to the EUR depreciation is not tax-deductible.

And, most important, this is nothing else than analysis of the current market expectations about the future development of exchange rates and central bank policies. Within a time frame of 1 year, the FX rates can easily change by +/-10%.

So, if you want a capital preservation, foreign currency position is not a way to go.

My suggestion: put your CHF into a savings account.

You forgot that you shouldnt compare the 121 CHF to 514 USD, but actually the 24121 CHF (24000 + 121) to 26621 USD (26107 + 514).

So if you start with a conversion rate of 0.919 (24000/26107) you have to compare this to the endpoint which would be a conversion rate of 0.906 (24121/26621).

That would mean you would win if the USD lost less than 1.5% (0.906/0.919) in relation to CHF, and you would lose if it lost more than 1.5% to CHF.

Seems like a plausible scenario to me (>=1.5% lost).

AXA Trésor Court Terme C is a low-risk mutual fund, which provide returns in line with short-term interest rates, which can include benchmarks like the Euribor (Euro Interbank Offered Rate).

In other words, as long as there is inflation in the market and the interbank exchange rate is high, this product gives a relatively high interest rate.

I know I could be investing in VT, but I would like to have a part of my cash that is invested in something where I can cash out easily and with little volatility.

My friend is living in Spain and he is investing via Myinvestor - a spanish broker. He can buy AXA Trésor Court Terme C and if he wants, he can withdraw his money straightaway, no waiting time.

My question : where can we buy this product if we live in Switzerland ? I’ve looked in Interactive Brokers but I don’t find it.

Any piece of advice is welcomed - if you happen to know similar products that we can easily buy in Switzerland, please also let us know.

Note: as discussed in previous threads, EUR short term investments will be exposed to currency risks (expected to lose value against CHF by the interest rate differential). If your expenses are not in EUR it likely doesn’t make sense due to the volatility and extra taxes.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.