This period gave me the stimulus to do some further thinking and better planning. Once this shitshow is over and we make ATH again I plan to shift more to dividends for the plain purpose of feels that my money is actually working rather than being speculative. This period is really golden overall for personal development (as an investor!).

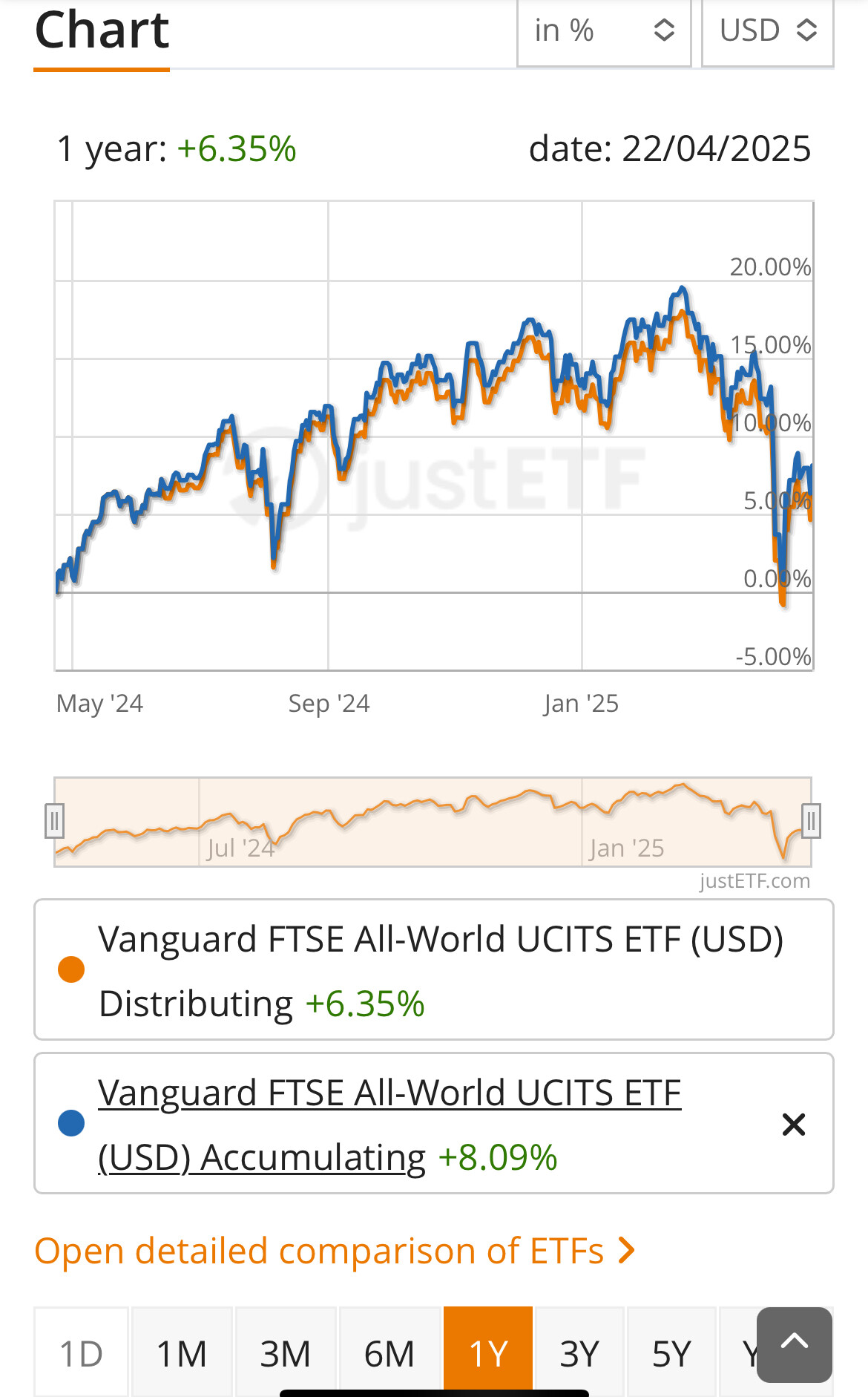

Looking at VWCE - the accumulating version of VWRL - this shitshow has set an investor back by a full calendar year. 13 months for VWRL. This feels completely unacceptable to me, really unacceptable. What was the benefit of holding either for these 12-13 months? VWCE returned exactly nothing, and incurred the same taxes in Switzerland, whereas VWRL allowed me to buy a few BRK.B shares “for free” in the same time period. I know it’s not really for free, but the feels is that these were bought with money I’d already mentally committed to be away from my hands for a long time, so I really consider it free cognizant it’s mental accounting extraordinaire.

Another interesting point is that someone bothered to make this post on reddit, with which I wholeheartedly agree, showing the exuberance in the dividend subs vs other subs I noted here a couple of weeks back.

First of all, I have nothing against dividends. In fact I like them too because I think at the time of retirement, having dividends could be useful vs accumulating version because it would help in avoiding transaction costs.

VWCE & VWRL returned more or less same money . The only difference between these two is that VWRL dividends have freedom to invest wherever.

Dividends of VWCE were used to buy VWCE (underlying companies) shares and that shows in performance because VWCE have higher return in 1Y period vs VWRL,

Dividends of VWRL were used to buy BRK shares (by you)

On paper you’re right, and can argue that buying a better performing asset (than VWRL) with the dividends is pure luck, and you’d be right again. But that’s why I highlighted the “feeling” part.

Exactly, and here’s the rub: I can’t really care about 1.74% difference over 12 months, it IS real, but it’s also immaterial considering the vastly different feeling. My post was all about feelings, specifically the feeling of being an idiot I’d get if I’d held something for a reasonable amount of time and seeing it cancel out any gains. I know the accounting difference, don’t get me wrong, I’d even argued against covered calls funds on this forum with pictures showing what % of total return is taxed vs what’s untaxed in CH between JEPI and VWRL. The numbers are clear, but I wanted to point out that the difference in emotional impact can’t and shouldn’t be discounted.

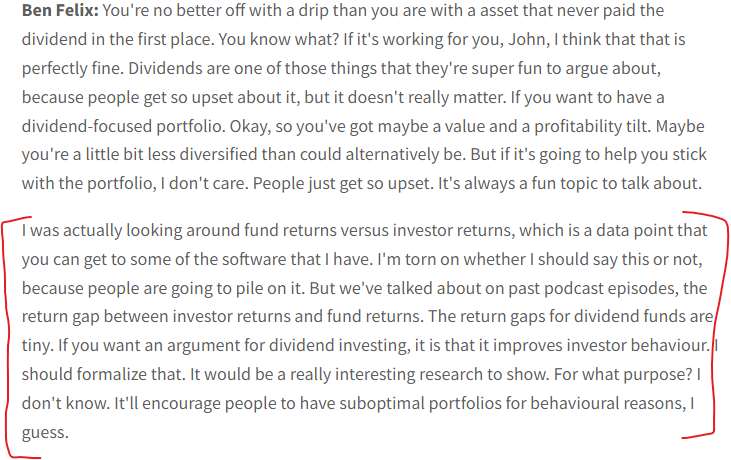

I think Ben Felix’s finding about the fund vs investor returns gaps is very important, as it illustrates that in a perfect scenario investors would get the index returns (minus fees, taxes, trading costs) but it alludes that in a real world scenario investors don’t, for psychological reasons.

Now that I have experienced two bear markets in my investing career, I have also learned some lessons which apply to me -: I am not built for 100% stocks due to very high volatility that comes with them & I also don’t feel comfortable with too much exposure to one regime & I should continue to learn about diversifiers (so far only Bonds & RE funds in my portfolio). When stocks go to ATH, and most likely Gold recedes , I might add gold to my portfolio too.

In summary , I think wealth management firms in Switzerland might have high TER costs but if we look at their allocation strategies, they have some learnings which can be leveraged by DIY index investors who are Swiss residents . I used to ignore them but I can see that their portfolios are well thought off.

There are no dividend funds in the comparison. The smallest gaps are in allocation funds, which we don’t have ready, unless you make one with a robo advisor, which is expensive.

The opposite side, investment as an entertainment:

I also see a psychological benefit to dividends. My 200 shares of CHDVD paid out nearly CHF 1000 (before WHT) in dividends in the last 6 weeks, which made me look like my avatar.

(That it’s up 5% YTD excluding dividends is also nice).

The fixed income should be in your “native” currency, in our case, CHF. I know only allocation funds in USD and EUR, besides shitty expensive funds run by Swiss banks.

The UBS Vitainvest Passive funds have a reasonable TER of 0.25%. They do invest 40% of the equity allocation in Swiss stocks, though, i.e., heavy home bias with a relatively high percentage of Nestle/Roche/Novartis. With the Swiss domicile, withholding taxes for at least US stocks are not optimal. Other than that, they seem to be a reasonable option, maybe even the only single-fund option that is still cheaper than the cheapest robo advisor (excluding promotional offers).

It seems they are available at Swissquote (but I haven’t actually bought any). I don’t know whether they are available at any other broker that has at least semi-reasonable custody fees.

Looking at it in another way, you might feel WORSE with a dividend stock heavy stache in a market crash during accumulation because your shares won’t be up as much

Maybe a more significant difference would come from a practice of detachment and stoicism.

I agree basically one can get an asset allocation fund for 0.25% TER. It would be very good for passive investors who want automatic rebalancing between asset classes and regions. Of course one needs to be fine with UBS investment strategy for these funds.

They have different level of equities (50, 75, 100)

Factsheet of VITAINVEST 75 is here

Ironically it’s much better to buy this on Swissquote & hold versus buying on UBS directly

That’s quite funny! I don’t plan to have it, but I recall there’s a list of UBS ETFs/mutual funds which have reduced or zero costs when held in a UBS account, would be…odd to not have these funds in that list…

Great post. I agree with this. I think dividend investing gives you the superior investment mindset as you’re not just asking what your return on capital is, but what is your cash return on capital.

As noted, when monitoring metrics of Yield on Cost and Dividend Yield/Portfolio Yield, it naturally leads you to counter-cyclical investing and value-investing.

Investing for gains is somewhat speculative as it requires selling into volatile markets to realise gains. This also leads to a degree of ‘illiquidity’ when it comes to realising gains as in down markets you ‘cannot’ sell. This leads to various maxims about stocks for the long term, but this somewhat masks this pseudo-illiquidity aspect.

Without the stark disadvantage of income vs gains in Switzerland, I’d be much more heavily into dividend stocks (and my portfolio yield is already >4%), but maybe it makes sense to pay the tax for a smoother ride.

That’s a special level of irony. You’ve found psychological safety in the fact that your dividends enabled you to purchase shares in a company that paid a dividend only once in its history (10c per share in 1967). Had that dividend not been paid, the distribution of ~USD 102k would have been worth USD 3.1 billion in 2023.

During these times there is a mismatch between your feelings and beliefs.

My feeling during March was, no all my gains from the start of the year vanished.

In April oh no where is this all going. Will everything change. Is the US going to self destruct.

There is and was quite a lot of fear. This was also fueled, because I stupidly followed the news to closely taking a lot of time leaving to little for recovery.

But I bought twice this month, because of my beliefs. I might not have bought at the right time, and it might go lower still. But I believe in people.

During Corona, my believe was that the governments will help the people, because its a rare event and that is a job of the government, to ease such events. Sure production was lower due to the lock downs. But for me that was a temporary problem. After it is over the people will go on as before.

Right now the belief in people is so that this is caused by a small group of individuals. They currently have a lot of power and are willing to risk chaos. But there are other people with money/power inside and outside the US that will do the right things during those times. It may show flaws in some systems, which may be corrected after such times. In the end this also will be temporary.

My grandmother used to say, you can’t know what good fortune will arise from bad times.

While I understand that feelings don’t answer to reason and that is the whole point of this thread, one way to look at it is to reverse it: stocks from April 2023 to April 2024 generated 2 years of returns so you had already banked on them and are simply now in the boring no returns part of the two years returns of April 2023 - April 2025.

Edit:

Or stocks from the end of January 2023 to the end of January 2025 generated 3.7 years of returns so you’d be good if stocks were back at the level they had in January by August 2026.

In one situation, you had a positive returns shaped period of non-existing returns (stocks grew then fell) and in the other, it is negativeley shaped (stocks tank then would rise). If you didn’t need the money in the mean time, they would be functionally the same though they would not feel the same (the second one creates anchoring that can be devastating if stocks are still down by August 2026, unless you can then take a higher view and go back further in time to gauge your returns.

One easy graphical way to do it is to zoom out on a returns chart and take the 5Y or All view.

Edit 2:

Incidentally, if you think you have a clear view of the allocation you want going further and are ready to adopt it for the long term, I don’t think it’s necessary to wait for new ATH to implement the change.

If this is a bigger drop, we’re still early in it. If this is about as low as it will go, changing allocation now is not that different than changing it one year ago, when we were at all time highs (if we want to nitpick, it would be different. The actual point when the changes should have been applied at an ATH would not be 1 year ago but should be calculated more accurately. The point is, there was a time at an ATH in the past where it would have been functionally the same in terms of returns up to now if you had implemented your new strategy then).

The fact that you were oblivious to it then, possibly because returns were plentiful and everything was looking rosy, is something I’d want to dig into in order to shape my future investing strategy.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.