Because VIAC forces me to do it if I want to invest all outside of CH and Frankly. incorporates it in their solutions directly.

I do not currently own foreign bonds but I’d buy a globally diversified fund hedged in CHF if that was my intent.

Because VIAC forces me to do it if I want to invest all outside of CH and Frankly. incorporates it in their solutions directly.

I do not currently own foreign bonds but I’d buy a globally diversified fund hedged in CHF if that was my intent.

I both hold a certain percent of global shares in a currency hedged Index fund. This given that hedging or no hedging in the long run was a zero-sum game. The last few years, non hedged had beaten hedged yet things are bound to mean revert. And even if not, there is a certain rebalancing bonus.

Further, I hold hedged bond Index funds. Hedging for bonds in my view is a must; and it is as well a must to diversify beyond CHF bonds.

It made me think. US Government Bonds had a nice anti-correlation to US Stocks. Wouldn’t that potentially be undone by taking an additional (covered) FX position?

And isn’t the focus on hedging securities wrong? Whilst you actually try to hedge your idiosyncratic consumption at Swiss inflation. As always you can only hedge for unexpected changes.

Let me think. Your expected consumption should be hedged for the unexpected local inflation vs unexpected global inflation. Your Portfolio then only has one job: To generate money at an accepted risk. It should have nothing to do with your consumption. If FX hedging inside the portfolio can still improve the return (directly or by decreasing risk which you can lever up again), then it does so regardless of where you spend your money.

Some market neutral long-short of short-term ILBs minus normal Bonds? Not that I would do that, seems expensive.

I consider it a discount atm getting more ETFs for my CHF. Do expect the CHFUSD to keep lowering long term but it will go back to the slower rate and even out. Right now its a discount, is my optimistic thinking. Nor am I bullish on European and Asian companies outperforming, so not increasing VSUX/VEA allocation.

There are a few ways - the main ones I used are:

Easiest is probably to take margin (hold negative cash balances) in your target currency. But this is now very expensive with higher rates and inverted yield curve likely leading to negative carry

Another easy way is to hold short positions in the target currency. You can get currency hedging for free with long/short hedging. e.g. Say you want to buy Costco, you buy $1000 of Costco and then say short $1000 of Target. You eliminate currency risk, reduce your beta and eliminate sector risk to some degree.

If you buy foreign stocks, there can be a degree of natural hedging as a fall in the currency will normally result in a rise in the share price. This of course depends on the specific stock and its features such as whether its inputs are imports and sales are exports etc.

Another way is to buy real assets. I do this mainly as an inflation hedge, but it is also a currency hedge. So you can buy real estate (inflation hedge only), commodities (I buy oil & gas, metals and uranium) or companies related to those (energy companies, mining companies, uranium holding companies).

Last is not to hedge at all if you want to take the currency risk. Or viewed another way, if you want to diversify your currency exposure. In Switzerland a lot of stuff is imported and so one could argue that holding foreign currency of those imported products is some form of hedging. Now you have unavoidable local costs such as: housing, health insurance, taxes, local services. Some of these can be hedged away by buying a home, having a local source of income (such as a pension or local real estate) and is normally offset by earning a local wage anyhow.

Looking then more holistically at how you hedge risks and needs in your life and not just currency risk in your investment portfolio, you can view currency risk in a wider context. Personally I do the following:

Think about directly hedging your needs e.g. buy property, insulate, install solar panels, etc. This way you become more independent and reduce your future costs which can increase with inflation.

I am in the phase of setting up my asset allocation and I am deciding whether to own a currency hedged world-equity ETF, or an unhedged one.

By reading around, see e.g. this post, it looks as if (Swiss) investors don’t quite hedge foreign equity.

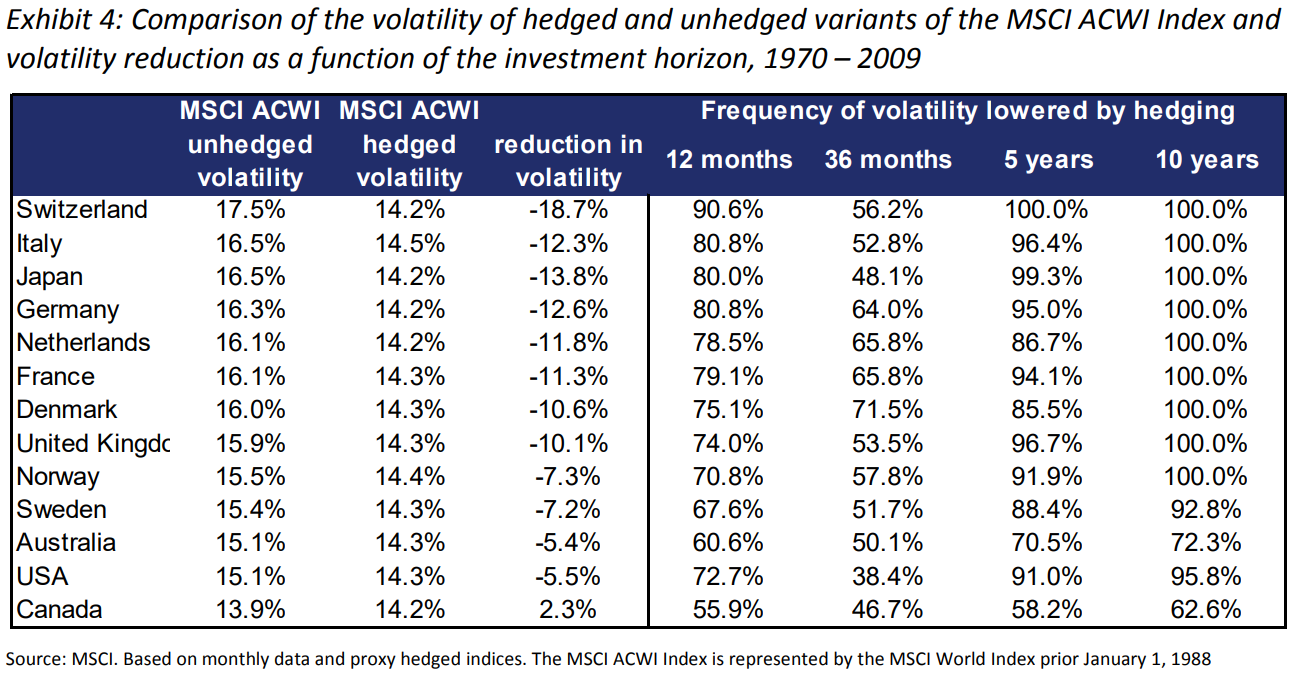

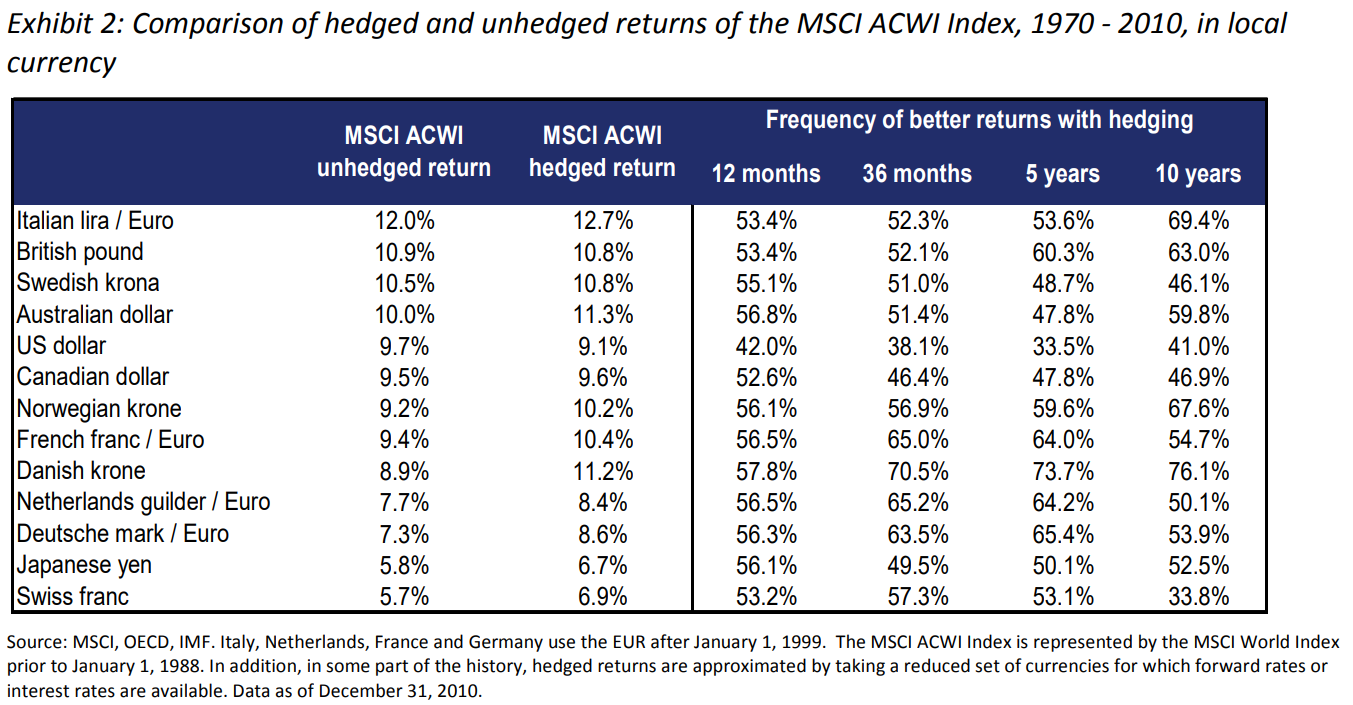

However, I don’t understand why. Consider this paper from MSCI. For the MSCI ACWI index (a world stock index), it seems that a Swiss investor, at least historically, could greatly reduce volatility by hedging:

From a return point of view, returns from the hedged version seem slighly higher:

Summing up, for a Swiss investor, historically:

So, why NOT hedging?

I can see a few reasons, please let me know what you think about them, and feel free to add more:

As I understand, hedging causes significant costs in the long-term.

This article from ZKB has some explanations and nice charts Link

I wouldn’t call it a “cost”, rather, a return. It can be both positive or negative.

Anyhow, the article targets not foreign equity but foreign bonds, as far as I understand.

Over the long run, returns from hedged and unhedged foreign equity (but also bonds) should pretty much align.

Best of both worlds could be to hedge only part of your portfolio, to reduce volatility.

If you don’t need to report your Assets Under Management in CHF on a, say, monthly, or quarterly basis, measured against some CHF hedged benchmark, what’s your benefit from reducing volatility in CHF?

I can see why it matters for a “professional” portfolio manager. They’re measured on a monthly or quartely basis against their hedged benchmark and their job & salary depends on not deviating too much from the CHF hedged benchmark.

But why would you care about volatility?*

You (IMO) in essence pay insurance for a smoothed out CHF value curve … which doesn’t matter if your horizon is years or decades?

Might also be worth looking at the sources advocating for hedging. Of course fund/ETF providers will happily offer you hedging and even tell you it’s great e.g. for reducing volatility … and equally great for them to make an additional buck or two for the hedged share class you’ll buy into. ![]()

YMMV, of course

P.S.: This topic has been discussed before on this forum.

* I could see hedging perhaps making sense if your asset allocation is 99% non-CHF, you’re quickly approaching retirement and you want to reduce currency risk (you’ll still pay for reducing that currency risk).

“Frequency of better returns with hedging:

Swiss Francs: 10 years: 33.8%”

In other words: 2 out of 3 times (measured in 10 year intervals), hedging performs worse.

Another datapoint from the newest edition of Gerd Kommer’s “Souverän investieren mit Indexfonds und ETFs”: when looking at the MSCI World Standard Index from 1975 to 2022, it would have been beneficial to hedge CHF against the USD…

But, and it is a big but: this does not include costs for hedging.

Is this scenario regular hedging, i.e., against the listing currency of each stock, not just USD, or is this partial hedging of only USD stocks, or some odd CHF-USD hedging of all stocks even for stocks that are listed in EUR, GBP, JPY?

With hedging costs, do you just mean the spreads of the forward contracts and possibly higher TER of the fund? Or do you mean that this completely excludes the price of the forward contracts (i.e., the interest rate difference)? The former shouldn’t make a huge difference (if an inexpensive hedged ETF is chosen) but the latter would make this data completely useless, as far as I can tell.

I don’t know exactly, I would think only USD stocks are hedged?

To your second questions, I think he refers to the average 0.3% TER hedging adds.

Here is the same content from the chapter about hedging on his blog (in German though):

Well hedging certainly does cost something, it can influence the return, but still a cost, like an insurance premium. The article doesn’t once mention bonds?

According to the ZKB article: “The appreciation of the franc against the USD has been at an average of 1.5% per year for almost 50 years. Hedging the USD cost an average of 2.7% per year during this period – in line with the average interest rate difference between the USD and CHF. The continuous appreciation of the CHF was therefore not sufficient to compensate for the costs of currency hedging. On balance, there is a loss-making transaction of 1.2% per year on average (=1.5% appreciation minus 2.7% costs of currency hedging), which accumulates into significant losses over time.”

Conclusion: “If the interest rate difference is higher than the expected currency appreciation, it is not worthwhile to hedge the currency due to excessive costs. As we have determined in our analysis, currency hedging is not worthwhile if the interest rate differences are greater than two or even three percent. In the event of interest rate differences between 1 and 2 percent, the result is neutral”

Okay, thanks!

Just to add on your points:

a smoothed out curve might make someone sleep at night and not quit their investing plan, this is more on the behavioural side but it could play some role.

Yes, but as @oslasho points out, including more data in the time window makes the return bigger. Could be interesting to see the same column with “20 years” instead of “10 years”

@ternes11, the ‘cost’ of hedging (for some countries other than Switzerland it’s a ‘positive cost’), tends to bring the interest rate of the country you’re investing into (bonds), close to the domestic (bonds) interest rate, there’s nothing around that:

(bonus: and according to real interest parity, all “domestic” interest rates are equal after taking into account domestic inflation… there is no arbitrage opportunity in the long term!).

Your argument is (?), if I don’t hedge, I won’t have this cost, so my interest will be the one of the foreign country.

But this is wrong, because if you don’t hedge, you’re taking up a different risk (currency risk instead of hedging risk). And the same paper mentions that

investors might expect a similar result when remaining unhedged over the long run, with currency returns producing a similar adjustment for underlying fundamental differences across markets

Here is the source btw.

Onto the ZKB article I believe that their reasonings make sense for short periods of time. Say you have a bond, and you want to use that bond in e.g. 2 years to buy a house. In that case, I believe it is beneficial to do the kind of reasoning that ZKB is doing (hedge if the interest rate differential is…), so that you don’t lose money in the short term, which is the horizon that interests you.

For stocks, refer to my original post.

PS: can you please point to where the topic has already been discussed?

I did a search before posting (probably not thorough enough) and I couldn’t find anything.