This thread is about hedging foreign equity, not bonds? The article also only covers hedging in the equity context?

Why on earth would I do that? (With perfect markets ok, but that would assume no taxes, no illiquidity, no transaction costs etc.) Keep it simple and just have (or convert) your bond in the currency you want to use…

I think hedging currency makes sense in the short-term if you happen to know that a currency is depreciating above average, which of course no-one knows, which is why for (private) investors it makes no sense IMO.

Hedging long term equity portfolio for currency risk is mostly meaningful with respect to peace of mind but not with respect to actual returns. Because if you expect higher returns then there is no research to back this up.

I see it like following

hedging is a cost , so it should impact returns.

in Swiss investor case, the idea of hedging always comes with assumption that CHF will appreciate against the world. What if it doesn’t happen?

I would be surprised if expected appreciation of currency is not already somewhere in cost of hedging . It cannot be the case that one can expect to always benefit from hedging

Looks like we need to getvthis conversation back to the basics aka Data. Hedging Shares is a very important tool to protect against Governments‘ Financial Repression.

In theory, Hedged and Non-Hedged Shares have the same return. This however only applies if the central banks allows the interest rates flow to their equilibrium. Once that is given, FX losses equate to the Delta of interest rates and there is no point to hedge shares.

If this is not given however, you shall hedge the shares into a currency without financial repression. What does this mean in practical terms?

EUR and JPY Yen domiciled shares shall be hedged (whether against USD or CHF dosnt make a big difference

EUR or JPY domiciled Investors shall still hedge a decent part of their shares against a non repressed currency (e.g. USD or CHF)

Make it make sense. You hold internationally diversified stock, most of it with equally diversified international economic activity. You want to speculate on FX, go buy futures. You can even lever them as high as it lets you sleep soundly (or even more if you enjoy that, up to a maximum of the broker margin calling and liquidating you).

Since VT (or VWRL) is highly promoted here on this forum. What does this mean for investors who invest in these funds? These funds include multiple underlying currencies but if one were to hedge some of them, then it would become quite complicated excercise.

I find it a bit difficult to accept that one would like to get diversification from international equities (because it is not so easy to guess which markets might perform) but at the same time somehow is pretty sure to be able to guess which way the currency pair might move.

For me it is simply not possible. And to be honest, few years back, JPY was safe haven currency too.

Maybe what I posted over in the 2024 outlook thread is better suited here, because when we’re already in the business of splitting the world into multiple region ETFs, it becomes trivial to currency-hedge specific markets.

To recap: currency hedging is universally seen as not worth it for long term stock investements. But I’ve found two articles for the Swiss investor that are not completely opposed to it:

The second article makes more sense to me, so basically one would put together a world portfolio with EMU hedged to EUR and Japan hedged to JPY, and then add the other regions without hedging?

I want to hit my face against a wall every time CEOs (!) of Investment companies say things like:

“your portfolio should be invested into different economic regions”

“a global portfolio is […] exposed to fx risk”

“this dilema is especially relevant for Swiss investors because the local stock market is concentrated in pharma and banking” (so foreign stocks need to be bought)

“CHF is seen as safe harbor and rises in crisis, this increases volatility of foreign stocks”

“the exchange rate risk from holding companies in foreign currencies can be secured with fx hedging”

So local multis like Nestle or Roche have no fx risk, because they are bought an sold in CHF. How convenient … how wrong.

But there are too many professionals that never questioned what someone else told them and continue to spread wrong information.

This volatility has nothing to do with the assets in your portfolio and everything to do with the CHF (or rather your consumption in CHF). It might look similar but it is not the same, and certainly has nothing to do with the denomination of your assets.

That can be true if you, as he recommends, hold a position less than 100%. If the long term expected return of two assets is 0%, but there is uncorrelated volatility, rebalancing actually gives you a positive expected return.

Two other nice facts are:

This can result in a positive expected return, even if both assets on their own have a negative expected return.

A position bigger than 100% on the other hand loses return from rebalancing (against the short position). This is also called volatility decay in leveraged ETF.

Link doesn’t work. Must be this one:

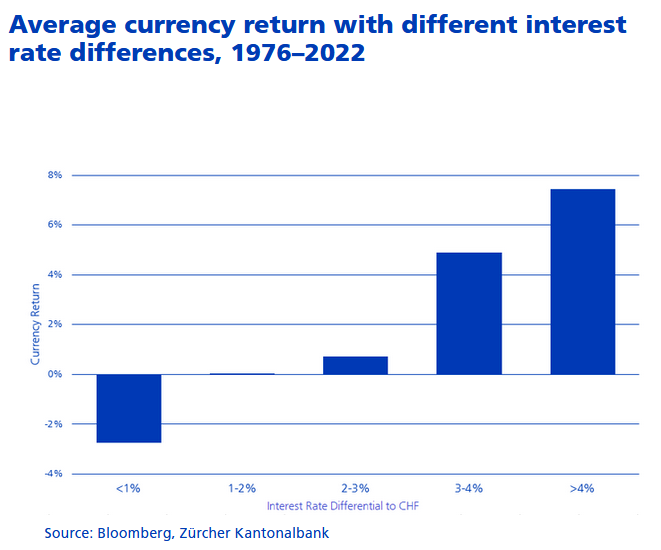

Their quantitative research shows that interest rate parity did not hold for the given period for large and small interest rate differences for CHF pairs:

I do have my doubts though. I see no explanation on why this should be so and continue to be so into the future.

If it were true, that would still not tell us anything about hedging of stocks. It only tells us that going long-short on currency pairs has an expected return different from 0. You should buy or sell contracts depending on the interest rate difference. I also don’t know if the risk adjusted return is on the efficient frontier, or if it pairs well with a given portfolio (e.g., 100% stocks).

Thank you for posting your thoughts. I’ve fixed the link.

When comparing the same index/fund with and without hedging, the differences are usually there but not huge, and the two variants regularly trade places on what’s performing better. For Japan however, the difference is staggering: the CHF-hedged MSCI Japan gained 82% in the last 4 years, while the unhedged MSCI Japan in CHF gained just 24%.

Meaning going short JPY and going long another strong currency. Normally you‘d do this with high interest currencies. It just happens that the CHF is strong and appreciates rather than paying interest.

And you are effectively doing that trade when currency hedging your Japan exposure.

No, I don’t mean the crash last month, but a steady depreciation of JPY vs. CHF last what, 10 years?

The problem with hedged equity that I see is that there is an equity investment overlayed with FX options. While I may believe that hedged equity can have a lower volatility than the unhedged one, I don’t believe that you can have higher long-term returns with hedging. Hedging is an insurance. You don’t earn with insurance, you pay for it.

By themselves, short term FX fluctuations vs. the expected long-term trend can go in either direction. Most probably this time it was pure luck that JPY systematically depreciated against CHF more than it was expected. I don’t see a point in making any kind of theory out of this.

I would be glad to be corrected, as always, but until I am convinced in something, I am happy to use the efficient market razor and stick with what is known to work.

If futures are used, it can’t be paid insurance for both sides of the trade if there is no spread. But if both sides are hedgers, one side has to win if the other pays.

In a closed system the total return must be 0, but we don’t have a closed system:

on a first level, every day investors enter and exit subsections of the market, some of them leaving losses or taking gains from it

on a second level, outside factors like taxes, fees, or inflation, demand influence the value of your assets

on a base level, production minus consumption is different from 0

There can even be improved return for both sides in absolute terms (given they find anti-/un-correlated assets). Let’s have a look how “hedging” part of your portfolio with uncorrelated pairs can improve returns. We will go one full circle with asset values and exchange rates ending where they started, but our total value having increased.

Stocks move

CHF/USD move

Stocks price [CHF]

CHF/USD rate [USD]

Unhedged [CHF]

Hedged [CHF]

Total [CHF]

Start

100.0000

1.1500

50.0000

50.0000

100.0000

Market moves

1.0100

0.9990

101.0000

1.1489

50.5000

50.4565

100.9565

Rebalance

101.0000

1.1489

50.4783

50.4783

100.9565

Market moves

0.9901

1.0010

100.0000

1.1500

49.9785

50.0224

100.0008

Rebalance

100.0000

1.1500

50.0004

50.0004

100.0008

How rebalancing works should be clear. The unhedged position just moves with the market. The hedged positon is a bit more complicated:

Basically the position moves by whatever stocks move. But we have an additionally big notional position in CHF/USD futures. This gives us the difference of whatever the rate moves in USD. Since we calculate in CHF, we still need to divide this return by the rate.

Some remarks:

Numbers are rounded.

I used anti-correlation, rates move the opposite of stocks. The returns will be negative if the correlation gets high. Even just a correlation of 0, will give a slight negative return.

If the volatility of our futures contract is much higher than the stocks, return is also negative.

I assumed no difference in interest rates. But as the expected total return on the futures contract, even with such a difference, is still 0, it shouldn’t matter much.

This is basically arbitraging anti-/un-correlated volatility. This has nothing to do with stocks or currencies.

Trading friction would probably eat the meager return and then some.

This is just mathematics, one could probably derive multidimensional graphs, splitting the vector space in areas with positive and negative return. Once it’s shape is understood intuitively, qualitative answers about where there is a rebalance premium, and where there are pitfalls, could be given with more confidence.

What about currency hedging in other context than stock/ETF investments ?

Most of my wealth is long-term into my business which has a big, unavoidable USD cash position (like it’s about 70% of my net-worth). USD/CHF exchange rate is very volatile and I am feeling less and less comfortable with such a big USD exposure as a Swiss resident.

I’d like to hedge at least a part of it. What are the best tools for the job ? Margin borrows ? Forex futures ? Options ?

In terms of costs, I’m aware that I probably will have to pay at least the USD-CHF interest rate differential (Already 4% atm ).

It explains common approaches for SMEs. This can help to understand concepts. To actually execute , you would either need to use your brokerage account and do it yourself or use one of the structured products offered by Swiss banks.

If you choose to use structured products, I would suggest to shop around a bit because you might get better conditions.

@tokzoo if you are interested in how Forex Forwards work, have a look at this video Link

I have never done it myself but for you it might be useful as you have business operations

There are many things that could be done about this cash position. But that very much depends on the reason for this. Could you be less mysterious and explain:

why this business needs so much cash that cash becomes 70% of your net-worth? What would happen if it was less?

I assume your business has some return on the capital invested. Did you take its value for net-worth calculation directly from the book?

What is the remaining 30%?

Depending on your answers hedging could even be a very bad idea.

Thanks, you actually made me realise that it is a common problem for any business with client/suppliers abroad. So it’s probably worth reaching out to some experts.

Sure, it’s basically the collateral for some niche trading business (algo trading). It needs to be in USD, I cannot directly use CHF collateral. The returns are quite high and more than justify the opportunity cost of other regular investments. You could maybe argue that the best is simply to not bother with hedging since the high returns would make up for FX losses long term. But still, the long term outlook for USD/CHF is down only. I regularly have great PnL month in USD but then big losses in CHF terms (e.g: USD is down 5-6% since late july…)

The remaining 30% of my wealth is mostly regular equity ETF.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.