Hi guys! It looks like you are all doing smart things like buying the dip. Congrats!

What I don’t understand is this: I always thought that the best long-term strategy is to be FULLY invested, at least in theory. Therefore, I am always 100% in stocks with minimal spare cash (less than 10k). This means for example that when I got my 2019 bonus in January I immediately invested it.

Now, I know that currently it might be a good time to buy, but how? No cash left here, as theory suggests. The only possibility I have is to sell some assets that didn’t behave that bad, like a Gold Producers ETF, to rebalance and to buy assets that were hit more. The other thing would be to postpone some payments, like taxes, or to buy on margin, but I am not comfortable with any of these, as debt would ruin my sleep.

Anyone in the same situation or you were all so smart that you kept some cash to invest in the rainy days?

Great question. It always seemed a bit contradictory to me that you should “invest in regular intervals“ but also “resist the urge to sell in a market downturn and, in fact, invest more.” As you alluded to, if you’re buying in regular intervals then supposedly you don’t have “spare cash” to take advantage of such a situation.

I tried to figure out this (seemingly) paradox a couple of years ago by searching around on Google, but it’s still not clear to me. Best I can tell is that the advice is really only applicable to (the large number of) people who don’t actually invest regularly. Of those who do invest regularly, some may also choose to set aside something like 5% each month in order to have “spare cash” when an opportunity arises (be it a specific stock, a friend or family member starting their own business, or a market downturn).

So my conclusion is that you’re the smart one by investing regularly. Assuming it’s something like once a month, you’ll also likely take advantage of the dip. In the end, although you’re not investing more, you’re certainly buying more.

My impression is that a portion of forum members haven’t been fully/regularly investing because they perceived stocks being largely overpriced. This of course is unknown, timing the market, etc. And I think they’d agree it’s not always a rational decision, especially since a highly-likely outcome is that years go by and you haven’t invested at all.

But I’d love to hear more opinions on this because I’ve always felt like maybe there’s something obvious that I’m missing.

Who suggested this theory? In the end, it’s up to you to decide which asset allocation you want to have.

So you’re basically living from paycheck to paycheck?

I think it mainly comes down to two things:

how long is your investment horizon? If you are talking about 20+ years, your gains in the stock market most probably will be the highest (compared with other assets)

how much book value loss are you able to stomach? Can you live with your portfolio going down 50% or more in case of a stock market crash? Do you know 100% you won’t sell any stocks when everyone around you is going crazy?

Nobody has 100% stocks anyway (you need some money to live), but if you are ok with a wild ride and you don’t need that money for a long time: go for 100% stocks!

Over the past, 60% stocks and 40% bonds would have fared best (according to BigERN from EarlyRetirementNow), but that’s how it was in the past. With this AA, you could rebalance your portfolio.

Regarding 100% stocks and only a little money saved away: please don’t forget that if stock market is crashing, businesses will be affected as well. Do you have enough money on the side to be able to survive one year without income, because your job was cancelled and you don’t find a new one?

It might seem so now, but maybe at the end of this month, when you are scheduled to do your regular investment, prices will reach even lower levels. Or not, who knows? No need to change your habits around this.

Imagine how much even better the time might be, once we hit another -10 or -20 percent.

This is admittedly true for me.

And I’m still trying to make sense of it.

So far, the stock market is approximately at the same level as it’s been a year ago.

We‘re experiencing the early stages of a potential global health crisis, with infections growing exponentially in many territories and restrictions on mass events and travel being put in place that have been unprecedented in recent history. These just barely shaving off a year of stock market gains doesn’t add up to me.

I am still making my regular investments on a fund savings plan. Thankfully, my job should be fairly safe and provide so e sort of anticyclical protection. The greater the economic turmoil, the more I get to do (over the short to mid-term).

Stocks have already outpaced GDP growth considerably, over the last few years (I think I‘ve said it before on the forum).

That remains to be seen.

Deceased consumers are no source of growth or steady earnings. Companies defaulting and going bankrupt due to liquidity problems aren’t either (at least over the shorter to mid-term). We haven’t seen yet how well health systems in emerging economies are going to keep up with the virus.

Also, I doubt we‘ve really seen or heard the full effects on earnings yet, from companies.

Seems the next rollercoaster acceleration might come again - Futures are red today.

Hope it continues for a couple more weeks, until the new salary is in.

For now this number and demographic is pretty insignificant, on the grand scheme of things.

But we will fully know only once it blows over.

Weaker companies and their illiquidity are probably a larger concern, true.

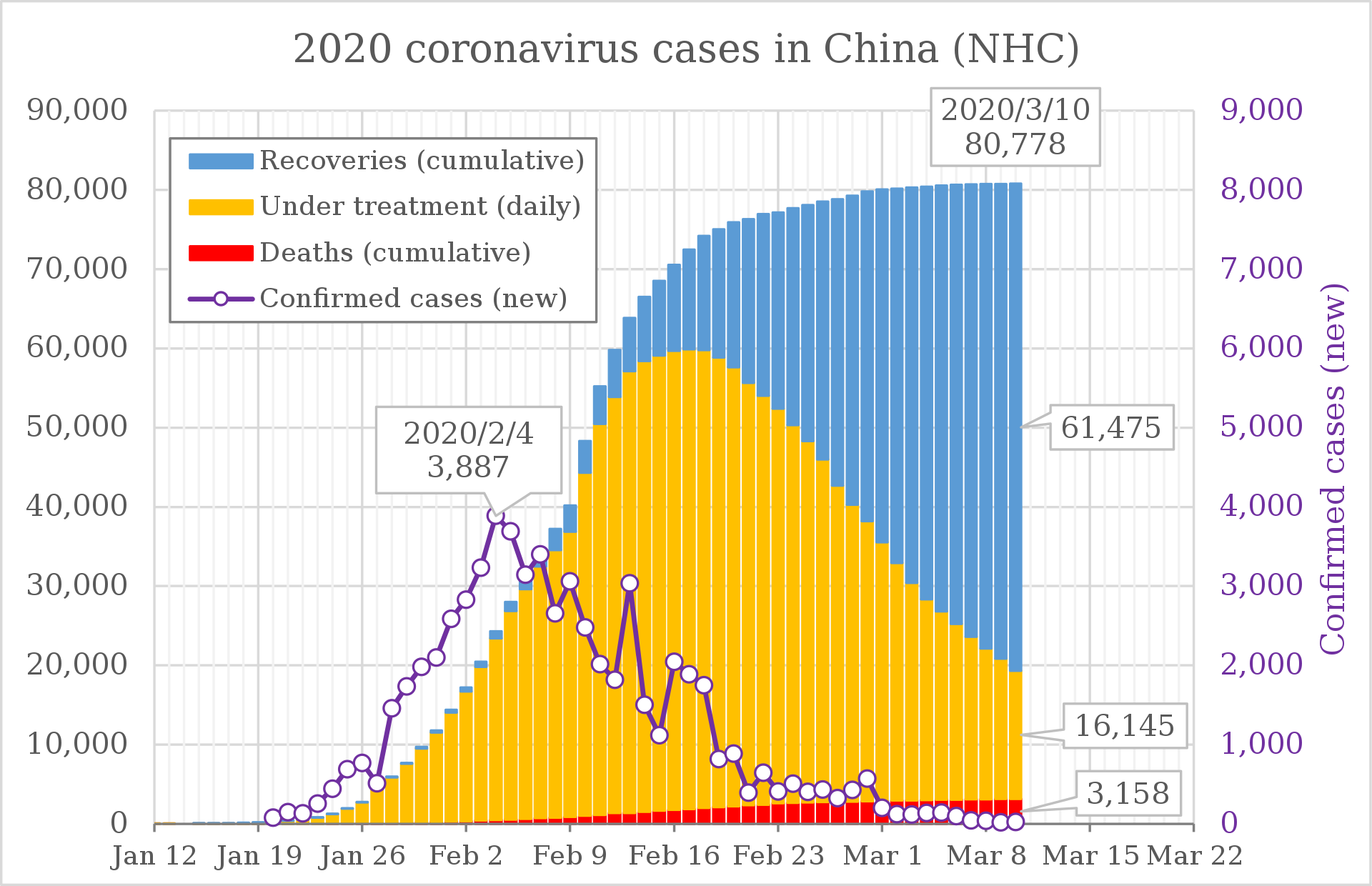

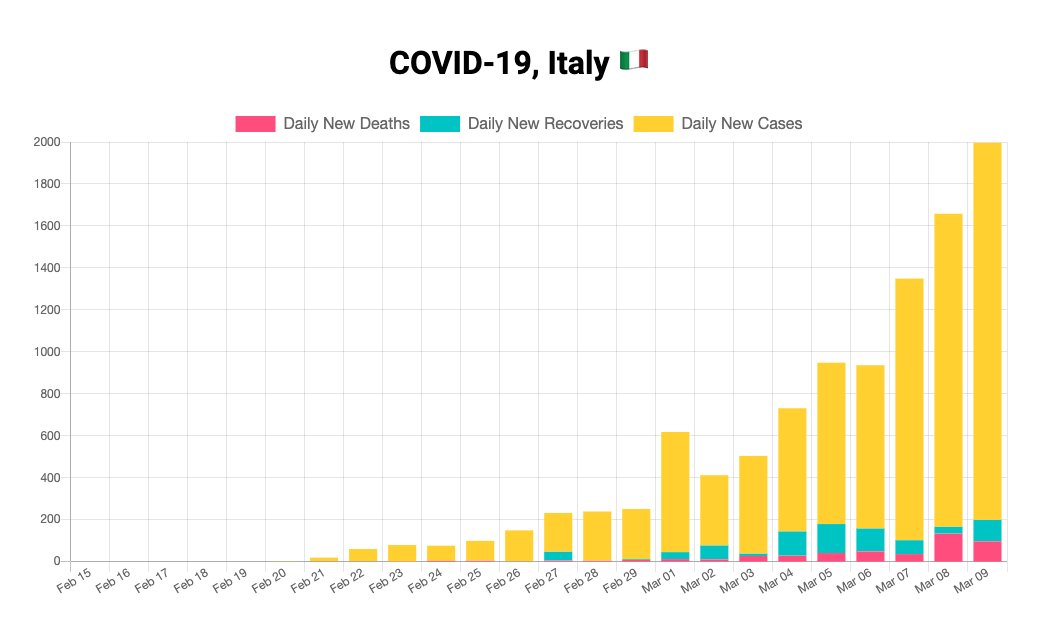

Switzerland and many other European countries are about one month behind China (it’s been 15 days since the first case on 25.02). Italy is a few days ahead of Switzerland (cases picked up on 21.02). No idea if we can take China as a model for predicting the future, but if we try, then you can see it places us around where China was between Feb 2 and Feb 9. If that’s the case, then I expect that in one month we will have around 500 people still under treatment and 1500 already recovered. So yes, we are still in early stages, and there are many unknowns, but the most likely scenario is that in one month we will be where China is today.

Stock price and GDP are not the same thing. Both are around $90 trillion, but the former is value, the latter is just a single year output. Stock prices include not only predicted returns, but also the value of infrastructure, resources etc. Just a thought. Is it widely accepted that stock market value should grow proportionally to the GDP?

Even if in terms of epidemics we are one month behind China, our governments went nowhere as far as China did to contain the virus. I do not see people forced to stay inside, with ration tickets allowing you to go outside every second day for less than two hours to do your groceries. That’s what it took China to contain the virus.

Other inputs:

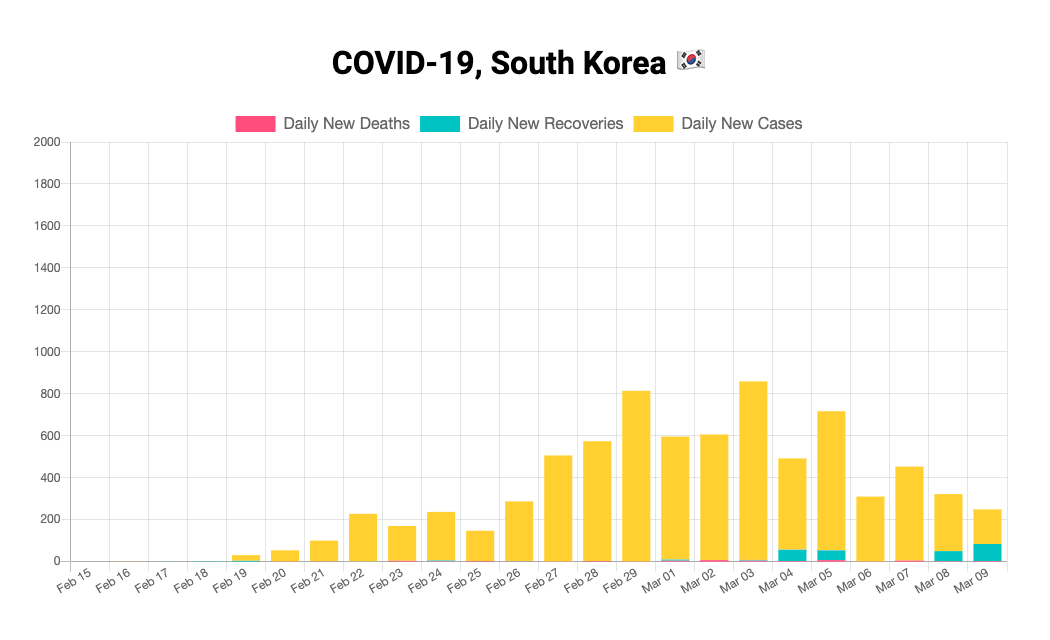

number of cases tend to grow 27%-28% per day in Europe

the symptoms tend to show 14 days after incubation, so the number of discovered cases is a small part of the real number of cases. In particular, today there are 491 official cases in CH, but i would guess the real number is 491 * (1.27)^14 = 14’000 cases. If this is true, then unless the government forces us to stay at home, i do not see how the whole population would not be infected.

Especially, they have spent their cash reserves for stock buybacks (distorting the share prices to the upside) and even accumulated debt doing so. Now they have weak cash reserves, tons of debt. Houston, we have a problem… Frankly I’d wait a bit before sinking my cash into the stock market. For instance what happens if companies stop their buybacks, or even begin to reverse them?.. Perhaps it is already happening now?..

Their measures, especially in Hubei prince, have been draconian. I‘m not sure how replicable they are for western democracies - and what the economic fallout would be.

To be fair, I didn’t bring up GDP in my reply.

However, with the measures that have already been taken or are about to be, it „feels wrong“ that this crisis will just shave off a year‘s worth of growth from the stock prices and then going back to business as usual.

Will you keep DCA’ing back in according to your plan then? Or will you wait? Given that you timed yourself out quite well, I want to see if you can time the market back in as well

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.