A really great very in-depth and technical RR podcast episode on passive ownership, how big it is and how to calculate it and how it can affect the market.

Leaving aside market efficiency etc, this sounds so bizzare

From one day to another a company find additional source of capital and this new group of investors are “no questions asked” type and have no love for the company, don’t care what it does.

Even though I am passive investor myself. I feel scared with the dynamics of passive investing.

So a question for someone who knows the theory. We always say market efficiency will correct the price of the stock. But how does it actually work.

Let’s say a stock is overpriced because it just joined S&P 500 and it now has new passive buyers who don’t care what the stock is worth. How will active investor actually exploit this ? Wouldn’t it depend on the overall capital this active investor have versus the capital that is pouring in from index side?

I’m more “scared” by the dynamics of venture capital. Many of these people are “no questions asked” types with love for the companies that has little basis in facts, who don’t care what they do and their profitability prospects as long as they can display the attractive label they’re after (currently AI).

Edit: Plus, they play mostly with other people’s money.

I don’t have time right now (I’ll that paper over the w/e maybe, sounds interesting), but I recall reading it also triggered taxable events? It was a royal ol’ shitshow

Edit: it’s good to have a clean thread of mostly graphs, maybe?

I like to look at those companies which left as potential bargains. One reason I’m looking at WHR even though consumer cyclical may not be the best sector to be in right now.

SMCI was also a poster child for liquidity. Going from trading OTC to S&P 500 in a few short years and share price from $12 in 2018 to peaking at just under $1200 in 2024 just 6 years later (a 100x in 6 years!!). It still pains me to think how much I lost there by selling.

LNC was another one I bought in 2023 after it left the S&P500.

The more I think about the more it appears really weird to me.

You would think to first list the company on a public exchange and let the active investors bang their heads to arrive at the efficient market price and only then – after at least a couple of quarters – to include it in an index.

Also, active investors – the way I imagine most of them – will want to look at hard numbers like quarterly reports, etc,* or use e.g. factors to determine whether a company is mispriced.

Most of this data is not available when the company goes from private to public, so price finding is initially anyone’s guessing game,** but after a couple of quarters some data will be available.

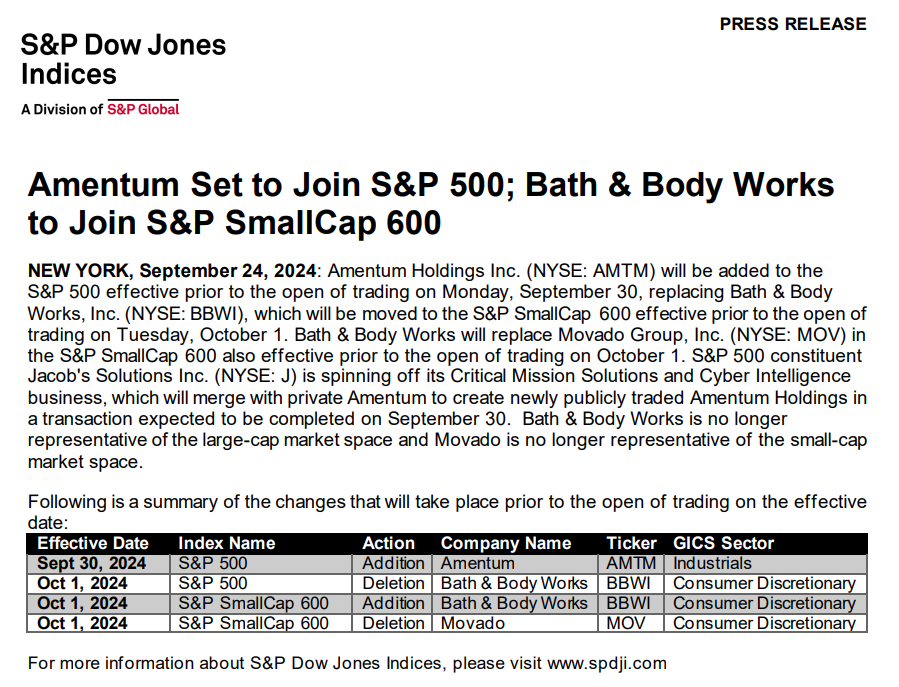

IIUC Amentum will IPO on Monday morning at the open (with some blocks of shares already allocated/sold to pre-IPO buyers) and the S&P 500 ETFs will buy at whatever the closing price is on Monday evening.

* Plus sprinkle a little active investor fairy dust on top.

** Ok, to be fair, investment bankers helping with the IPO will have taken a deep dive with the CFO to determine a “fair” offering price, but … well, I trust investment bankers a smidgen less than used car salesmen.

Probably a lot more accessible than the paper to many, and explaining many of the terms and e.g. why things are traded at market close, etc.

Also, great energy by the paper author.

I subscribed to the RR podcast.

(For folks preferring to digest dense info, the paper is probably still the way to go)

If the stock / broker / exchange allows for short selling: sell the stock short?

(I am frankly not entirely sure what criteria exist for allowing short selling – I am guessing it’s mostly a mix of the market maker / exchange who decide this, as they have to deal with the risk)

If there’s an options market for said stock – typically the CBOE will decide whether to list options, not sure what criteria they apply – then as a pessimist on a given stock you can buy Puts (say, at current market price minus at least 25%, citing your pricing scenario).

Absent these two instruments I don’t really know.

Gun to my head, if I were an Active Investor convinced of prices going down 25% over some short term, absent the above mentioned options, I’d probably buy and sell on a ladder basis, selling if it went up on that 25% ladder, buying if it went down, etc.

I’m pretty sure I’d be wiped out over the course of just a couple of months or so.

I think that it’s easier for active investor to make a difference by buying an underpriced stock but it’s very difficult to make a difference when stock is over priced

Most likely main options would be

A - active investor will simply not buy the overpriced stock.

B - go after the stock using short positions. This is most likely not done for every company. They pick their own fights. If they open a short position, then idea would be to wait till everyone else realize that stock is overpriced and then price falls.

what I am not sure is what happens on passive side. Let’s say this company X is 1% of S&P 500. So every time someone buys SPY and it results in net inflow of 100 USD, 1 USD is invested into this company X

If the share was held by active investor , they would ideally sell to passive because as per active the stock is not worth it.

If this process continues and more active investors will exit their positions, the supply of stock will reduce when the new passive inflow comes. With lower supply and continuous demand, the price will move up further.

How long can this continue ? And what breaks this cycle?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.