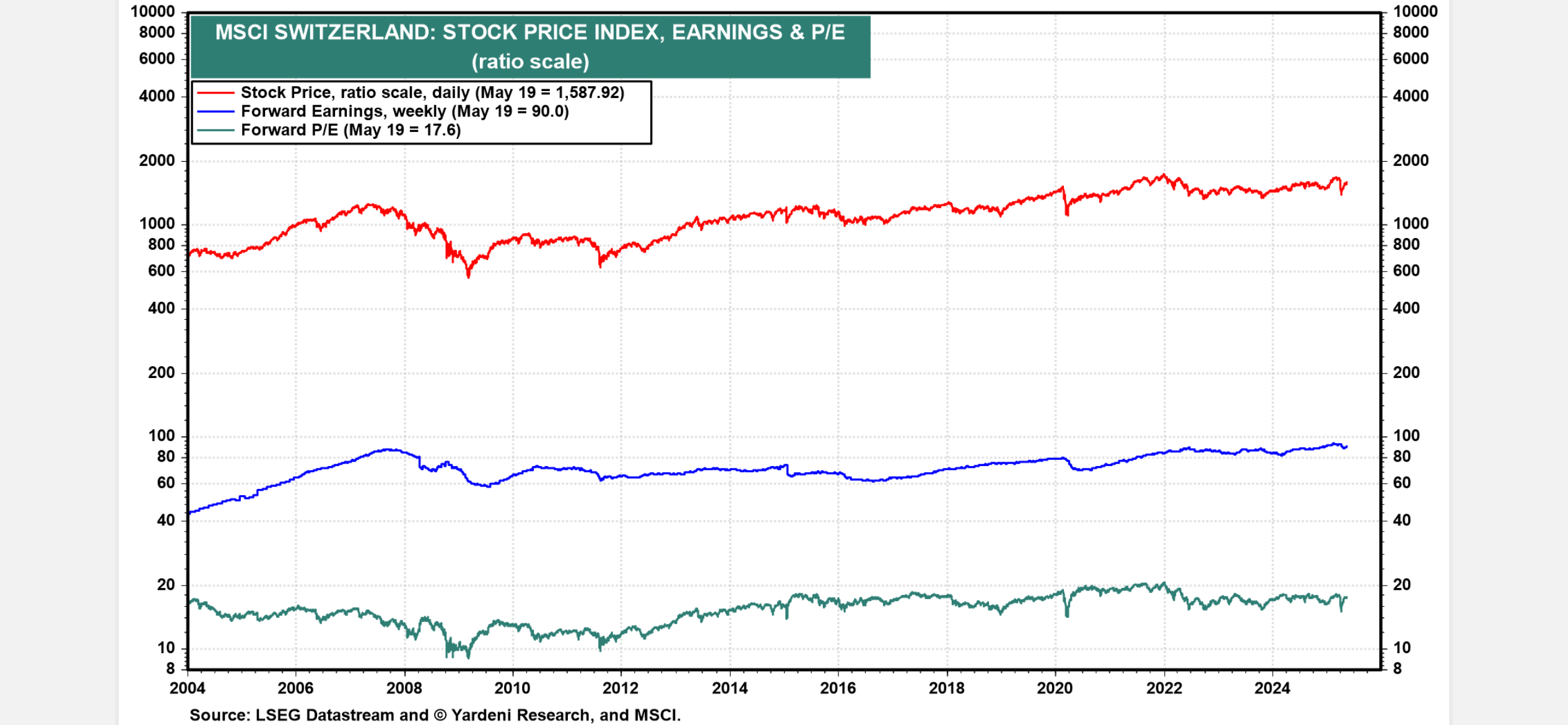

Which PE you are referring to?

It seem the Forward PE of Swiss stocks is not much different than historical numbers

US forward PE is 21.9

Which PE you are referring to?

It seem the Forward PE of Swiss stocks is not much different than historical numbers

US forward PE is 21.9

If that would be a consistent rule, it would mean great time for accumulators in the next 10y, as the big gainz coming after that 10y phase would be bigger than big gainz now (1-10) followed by drought (after 10y).

But I kind of doubt it is that easy.

backward PE I guess, mostly looking at PE in morningstar portolio tab and Switzerland Stock Market: current P/E Ratio . Forward (looking at at IBKR for EWL) looks still in the middle between VXUS and VTI (12.21 <=> 16.14 <=> 21.13), but it does indeed look a bunch better.

I think very long term average suggests 4-5% inflation adjusted returns from equities. For a 20-30 year period, I think that should be possible if world GDP continues to grow and don’t fall apart.

The thing is that equity investment history is based on growing population and a big part of it was in peacetime.

In addition, in past equities were considered risky and hence investors demanded lower multiples. But these days most people believe equities are the best place to be which kind of reduces risk premiums as they are not seen that risky and hence returns should also reduce (that’s an opinion)

We don’t know how it would be in future

Yeah.

Google „Yardeni charts“ which is a great source of market data and comparison of different metrics for multiple regions / countries

Oh come on doomers!

“Hey MP-LLM, set a reminder for 10 years” ![]()

I say it’s going to be 5.5% - my guess of the future is nearly as valid as theirs.

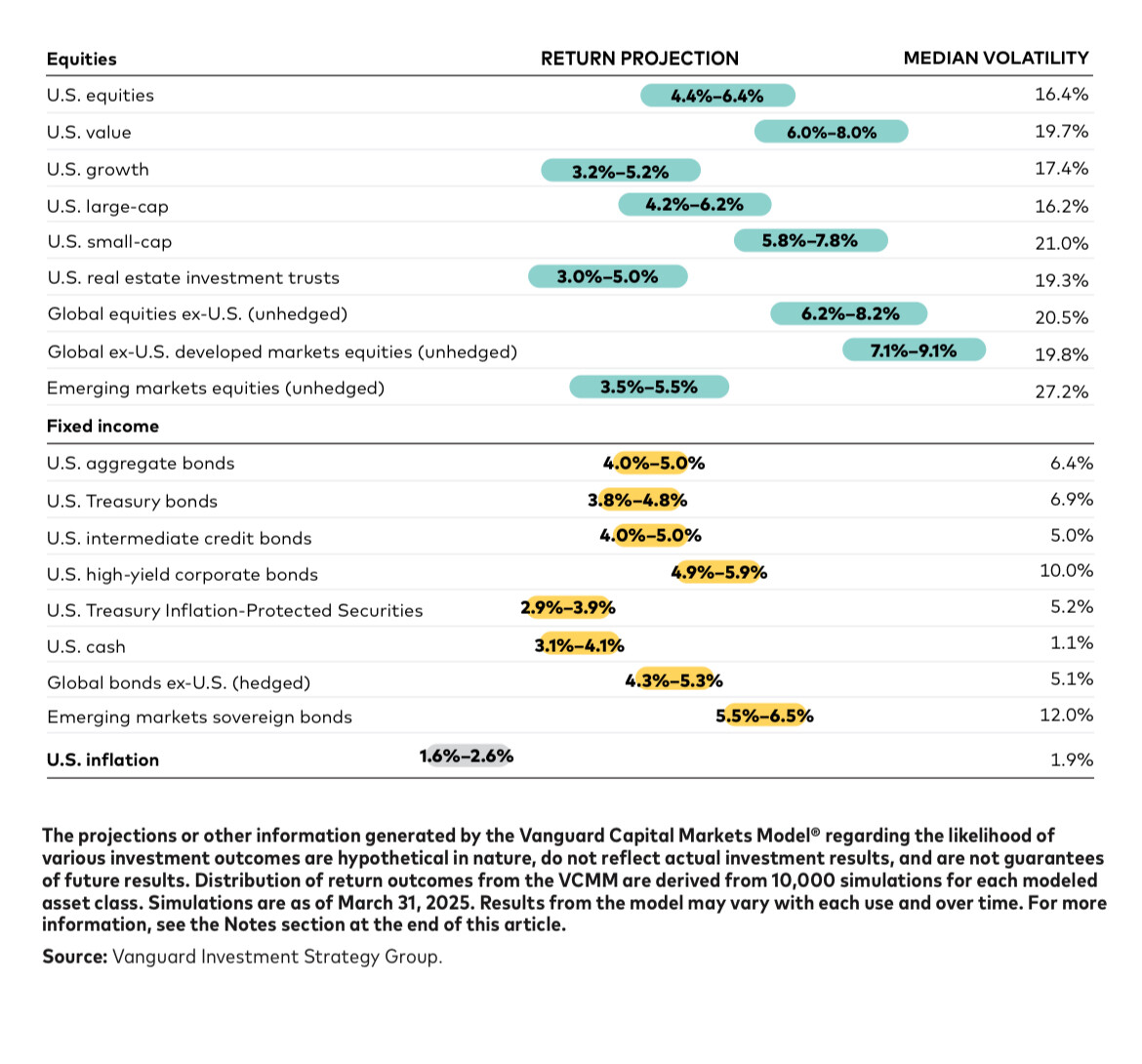

Their numbers indicate an appreciation of CHF against EUR of 3.6% p.a. and against USD of 3.9% p.a. over these 10 years at short-term interest rate differences of 1.6% against EUR and 3.2% against USD, if I’m not mistaken. I.e., they’re expecting EUR/CHF at 0.67 and USD/CHF at 0.57 in 10 years. Or am I making an error in reasoning?

While I also expect CHF to appreciate further, the numbers above seem rather extreme. Especially EUR depreciating over 10 years by so much more than the short-term interest rate differences.

I am not sure how did you come to this deduction.

If I look at their projection for Euro area bonds , in EURO terms and also in CHF terms then I don’t see such high differential. It’s 3.2 % in Euro terms and 1.7% in CHF terms. So differential is about 1.5%

Their paper doesn’t really say what the currency projection is. But I am assuming you are trying to establish that using return assumptions

Regarding USD, the returns expectations were not in the paper, but I found the US equivalent info. For CHF / USD it seems the expectation is indeed to appreciate quite a lot if I use similar assumptions

Having said that I don’t know exactly if the underlying regional allocation also assumes some sort of home bias based on location of investor when it says „global“

The 1.7% p.a. for Euro area aggregate bonds in CHF are hedged. With hedging, I would expect the return difference (1.6%) to match the EURCHF forward rates (funds typically hedge using rolling 3-month forward contracts or similar, as far as I know), which are based on interest rate differences.

For Euro area equities we have an unhedged comparison: 6.5% p.a. in EUR and 2.9% p.a. in CHF, that’s where my 3.6% p.a. appreciation number comes from.

The CHF vs. EUR/USD numbers are way above what I’d expect the reasonable inflation difference over the next 10y to be, and as such that you’d expect 4-5% real in USD doesn’t mean we get 4-5% nominal in CHF.

Honestly when I saw this entire thing end of last year I decided that maybe my 1-3% returning 2nd pillar isn’t such a bad idea after considering tax alpha. Obviously not all in, like these predictions aren’t that reliable, but also not a thing to avoid anymore.

Yeah that is another way to look at this. I always found the CHF expected returns from Vanguard a bit on low side versus other currencies. I am sure they know what they are doing but I cannot really explain how they come to these differences.

Only because we don’t like a 60/40 allocation and the the fact that with pillar 2, we cannot properly rebalance, it doesn’t mean it’s there. This is why we need to be able to have some control over the 2nd pillar.

Edit: And by the way, a 100% stock allocation is always balanced ![]()

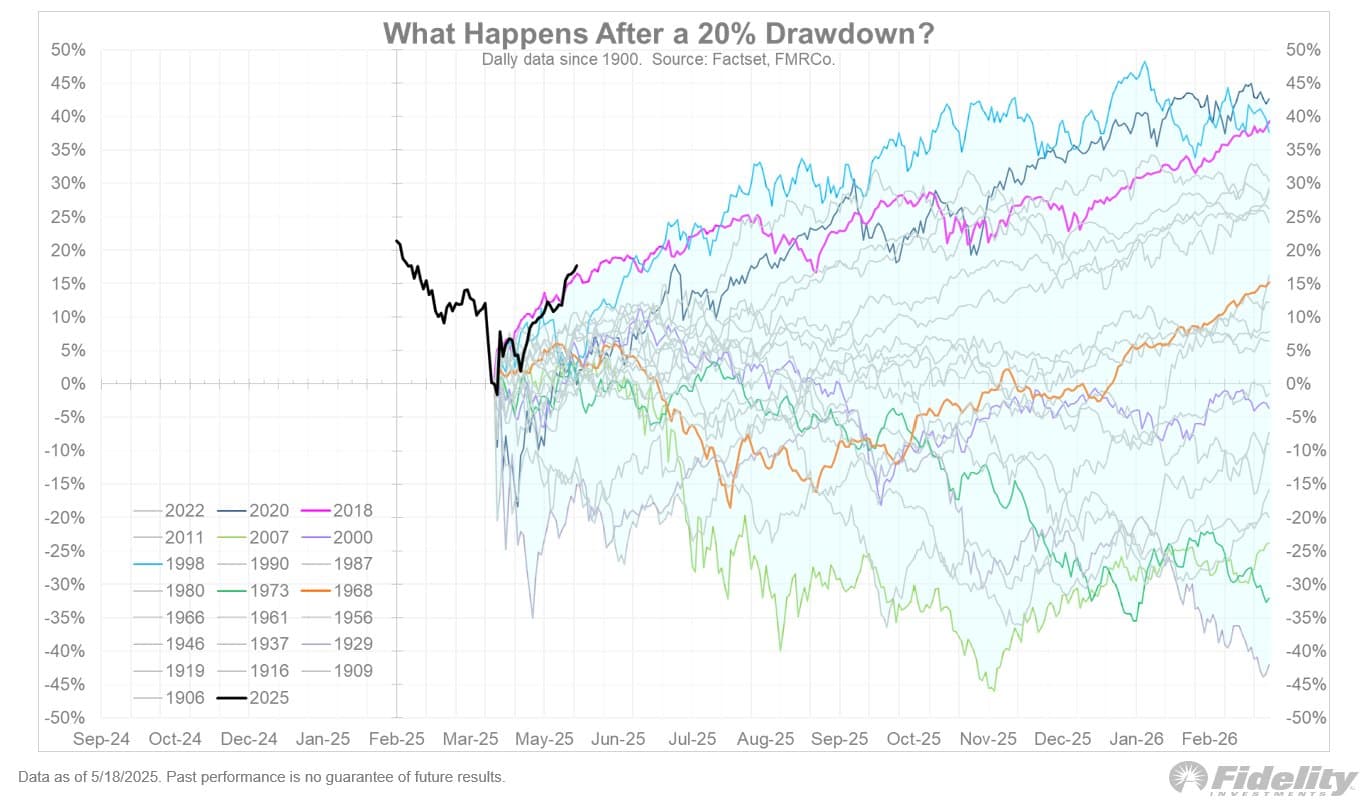

Since y’all bigly liked this beautiful chart, here’s the update two weeks later:

“For now, the recovery has been as impressive as the one following that 20% drawdown in the fourth quarter of 2018. That’s the pink line below. I certainly didn’t have a V-shaped recovery on my bingo card a few weeks ago when both the bond and stock markets were being stress-tested. But the markets won and the Put was exercised. It was not a 2018-style Fed put this time, but a put is a put.”

– Jurien Timmer

(Source)

![]()

OK. What happened? I just got back from kid’s swimming and thought maybe a good time to take some of the recent profits and log on to see a sea of red.

I wish hadn’t closed my LLY puts, but I hate holding short positions.

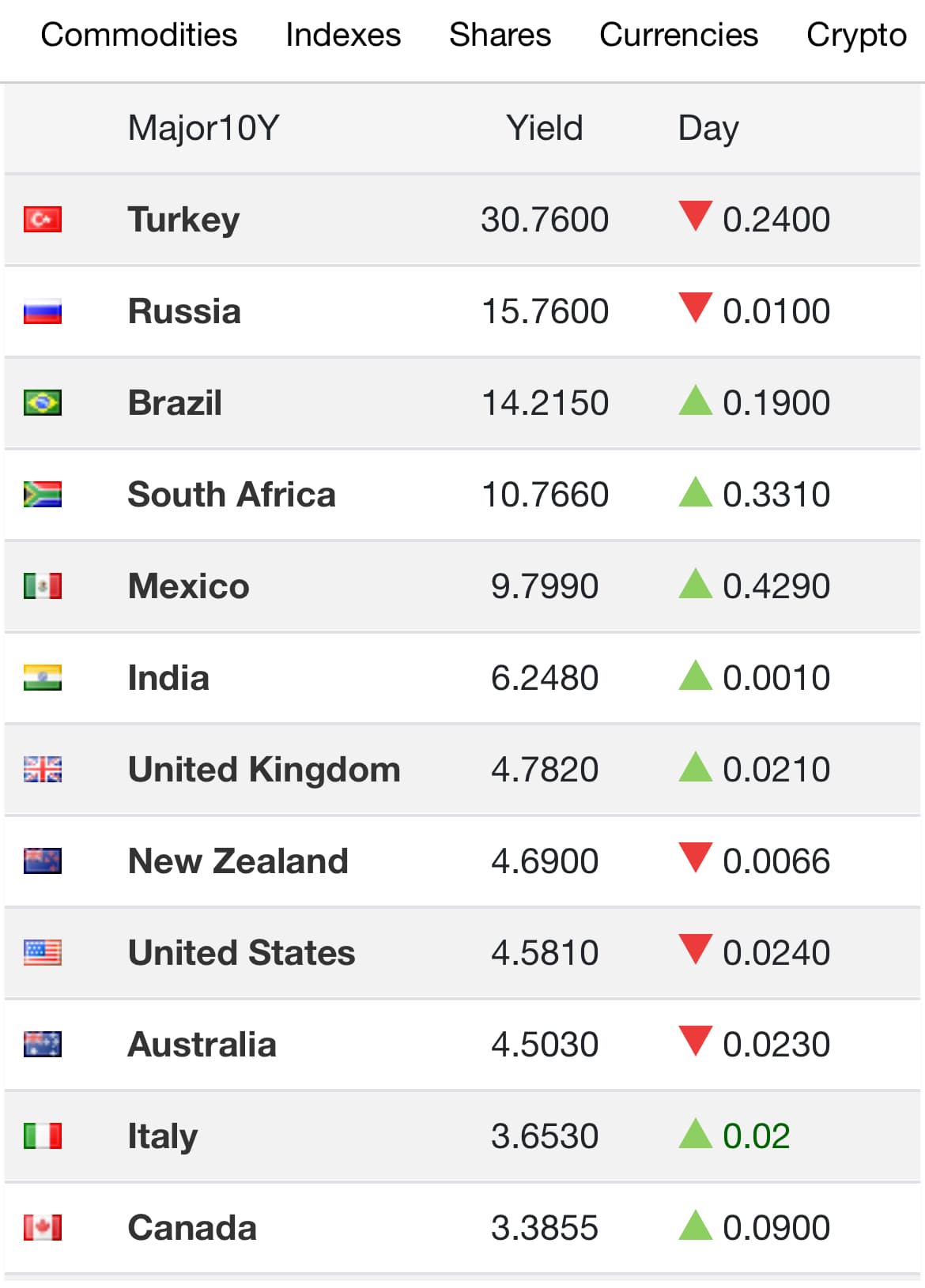

US treasury bond auction

May 21 (Reuters) - The U.S. Treasury Department saw soft demand for a $16 billion sale of 20-year bonds on Wednesday with investors worried about the country’s increasing debt burden as Congress wrangles with a tax and spending bill that is expected to worsen the fiscal outlook.

The poorly received auction, which saw stocks and the dollar sell off while U.S. Treasury yields rose, shows intensified investor worries about the country’s ballooning debt that could spur bond market vigilantes who want more fiscal restraint from Washington

Just the bond vigilantes. For a moment, I thought it was something serious like Cortana investing more ![]()

Who would have thought during Greek crisis that one day all of the IGPS countries will have lower 10Y bond yield than UK & US

Some good insights from this panel discussion. Head of Kuwait investment authority & Howard Marks

Key points

Anything with Howard Marks is great, but for me the memorable quotes from the panel discussion were by Sheik Saoud (probably because I’ve listened to Howard Marks so many times already and have heard his great quotes already multiple times).

Anyway, Sheik Saoud:

“In public markets I would identify the main risk is index investing.”

“It might sound counter-intuitive, but you’d reduce your risk by increasing your tracking error.”

“Private equity is in trouble.”

Although, in defense of Mr Marks, this summarizes how I think about AI, so, obviously§ the best quote:

“AI knows everything that’s ever happened, and how stock prices reacted to everything that ever happened, so they can emulate the path to success that worked in the past.”

Thanks for sharing the link and your summary, I really enjoyed it!

That’s going to cost you a couple of followers on this forum … ![]()

(FWIW I agree with the statement)

[§] ![]()