We’re borderline politics again … but I do admit I am personally curious, too, who will cave in first.

We’ve already seen that the bond market has … a tight grip on the … well being of the wanna-be mafia boss and will make a … ballsy move if necessary.

I personally think so does the equity market, but if a single company like Walmart can withstand an orange utan beating his chest … we’ll find out in due time.

The majority shareholder in Walmart – the Walton family – is worth about a hundred times more than the other guy, so maybe that plays a role, too.

If anything, the other guy will help with a more attractive entry price for $WMT which has been on my watchlist since I started it but always seemed too expensive:

(I’m afraid that even halving the stock price still only brings it to its normal valuation of about 18xP/E, which is still not a bargain, but perhaps a fair price for a wonderful company or so)

Here’s something he apparently also said a little while ago:

“After causing catastrophic inflation, Comrade Kamala announced that she wants to institute socialist price controls . . . Her plan is very dangerous because it may sound good politically . . . This is Communist; this is Marxist; this is fascist.”

(Source)

Market doesn’t seem to be overreacting to the US credit score downgrade, possibly because Moody’s is just in line with the other two. I was kinda hoping for a buy day, but let’s see until later today.

US credit rating is pretty meaningless in my opinion.

They control the world reserve and the market knows everything there is to know about the US and its budget.

A rating agency won‘t know anything more or influence anything more than the market already does.

For smaller/less inportant countries it‘s likely different.

This is why the 2nd pillar should always be included in the asset allocation calculation, so the asset allocation does not need to be changed from one day to the other.

Someone who never invested before, shall in my view under no circumstances take the money but just the normal pension. Pensions are actually quite a good deal - yes, there is no inheritance but at the same time, you still get a very decent withdrawal rate. Yes, its not inflation adjusted but it is still between 5 and 6%. Compared to an inflation adjusted, safe withdrawal rate of 4%… 5-6% in a world with 0.5% to 1.5% CPI is a good deal actually. Clearly, when you invested all your life, the situation is different and you can take on more risk.

With regard to asset allocation. The point of having a multi-asset allocation is to have the option of re-balancing. You simply can’t rebalance with second pillar money. Therefore, I don’t think that second pillar should be considered as part of your overall asset allocation. If you can chose your asset allocation of your second pillar (aka in a vested benefit account), you should roughly have a comparable asset allocation than outside of second pillar. Yes, you can tweak it a bit based on your liking… but you shouldn’t go extreme because as said, you can still not rebalance nor eat these funds until you retire.

My second pillar is (don’t quote me on the precise figure) I think about 40% of my total, investable assets. If I considered it in my asset allocation, logic would call for a 100% shares only portfolio (so that total Asset Allocation was roughly 60/40). But seriously… a 100% shares portfolio was a major mistake for me, particularely in case of a downturn (as I couldn’t re-balance anymore).

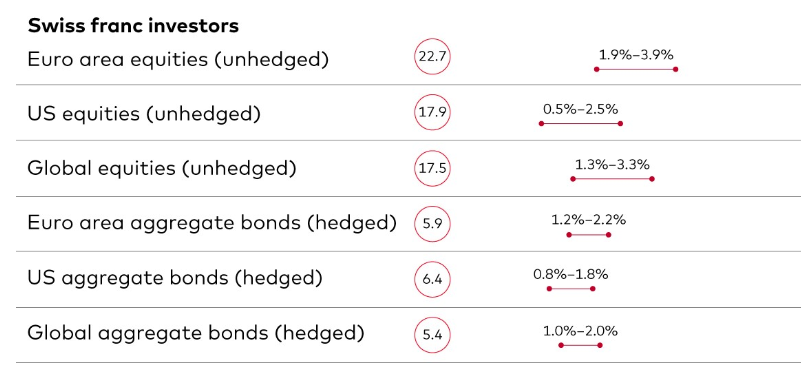

Numbers in circle represent Volatility & the range reflects expected return over next 10 years

Tough life for CHF based investors as always. Expected return for 60-40 portfolio is about 2%

They don’t really separate CH stocks. They just have the breakdown mentioned above. Perhaps Swiss stocks expected returns should be similar to Euro area.

Note that Vanguard tends to weigh valuation relatively heavy (just like Research Affiliates which tends to really like value investing), so the US return expectations are lower than most other predictors.

Talking valuations, Swiss PE ratios being way up there almost with the US definitely doesn’t make me a very happy Swiss equity investor (vs. going ex US in general). Wonder at what point the tax advantages are not worth it anymore.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.