He made it up, for illustration. It’s a lot easier to make a compelling looking case when you just make up the numbers to match the thesis!

Inference for proprietary models is a high margin business, most estimates end up with a 60-80% margin. I have never seen a credible technical analysis conclude that inference is loss-making, let alone these fantasy numbers. An analyst being ignorant of that is not worth paying attention to. An analyst aware of it but choosing to make up the numbers is worth actively avoiding.

In contrast to believing stuff written on some anonymous FIRE message board …?

I don’t think you have to believe anything he says. I see it as a more of a illustrative way of saying how @Mirager already summarized it:

Anyway, for those with too much time on their hands (like me), here’s a less doomer discussion on AI. I watched it because I value Ben Hunt’s perspective who runs a company that extracts narratives from all public information that can be scraped, i.e. extracting a view of what the public interprets from seeing the real data (and, 2nd derivative, how it reacts to the narratives already out there).

Summary by Gemini:

Based on the panel discussion, here is a summary of the key opinions from the participants regarding the state of AI, its profitability, and the progress of commercial deployment (skipping audience questions after):

1. Where AI Currently Is (The State of AI)

Participant

Key Opinion

Ben Hunt (Epsilon Theory)

AI is currently in a state where it requires massive constraint to be useful. Users must engage in context engineering to provide structure to the data and tell the AI how to think, rather than asking it open-ended questions, which leads to a “trough of disillusionment”. The true source of future alpha for investors is in the continent of unstructured data.

Jack Kokko (Alphasense)

The key technical challenge is verifiability. For high-stakes business decisions, AI outputs must include “scaffolding” and “guard rails” that allow users to trace information back to the original source to gain confidence in the conclusion.

Michael Cox (Piper Sandler)

Financial institutions are generally attempting to build homegrown systems (“Piper GPT”) for IT security reasons, but he believes this is a losing “arms race” and that the industry will eventually need to adopt package solutions from specialized external providers.

2. Whether it will ever be Profitable (Capex & Bubble)

Participant

Key Opinion

Ben Hunt (Epsilon Theory)

The spending is not a bubble, but a “train” that cannot be stopped. In the first half of 2025, AI capex contributed more to US GDP growth than all personal consumption. This massive spend must continue to generate a productivity boom to keep the economy out of stagflation.

Jack Kokko (Alphasense)

The capex is not overdone. Commitments to spend hundreds of billions on model training have no end in sight. He foresees a coming shortage on the inference side once enterprise adoption accelerates.

Michael Cox (Piper Sandler)

The industry is currently in the “pick-and-shovel” boom (capex buildout). The jury is still out on whether this will lead to a profitless bust, but he notes that we are still in the very early stages of its capabilities.

3. How Far Commercial Deployment Has Advanced (Adoption & Productivity)

Participant

Key Opinion

Ben Hunt (Epsilon Theory)

Low Commercial Advancement. We are “a million miles away” from having an autonomous agent that can make a trusted, smart, differentiated decision and fully replace a junior worker. However, AI is an enormous challenge to business models (like Big Law) based on overhiring at the junior level.

Jack Kokko (Alphasense)

Mixed Deployment. There is a lot of “wasted AI spend” and many internal corporate projects are failing. Conversely, in successful, specific use cases (like financial research), there is tremendous upside. The goal is to raise the bar and free up human staff to do more work faster, not to cut headcount.

Michael Cox (Piper Sandler)

Deployment focused on Enhancement. The goal is to use AI to raise the bar and put current employees to more productive use, not to replace them. The real commercial success will be found in companies and industries that use AI to drive incremental revenue or margin improvement (e.g., enhancing retail loyalty programs).

Enough with the FIREing, back to AI … (I know you were all anxiously waiting):

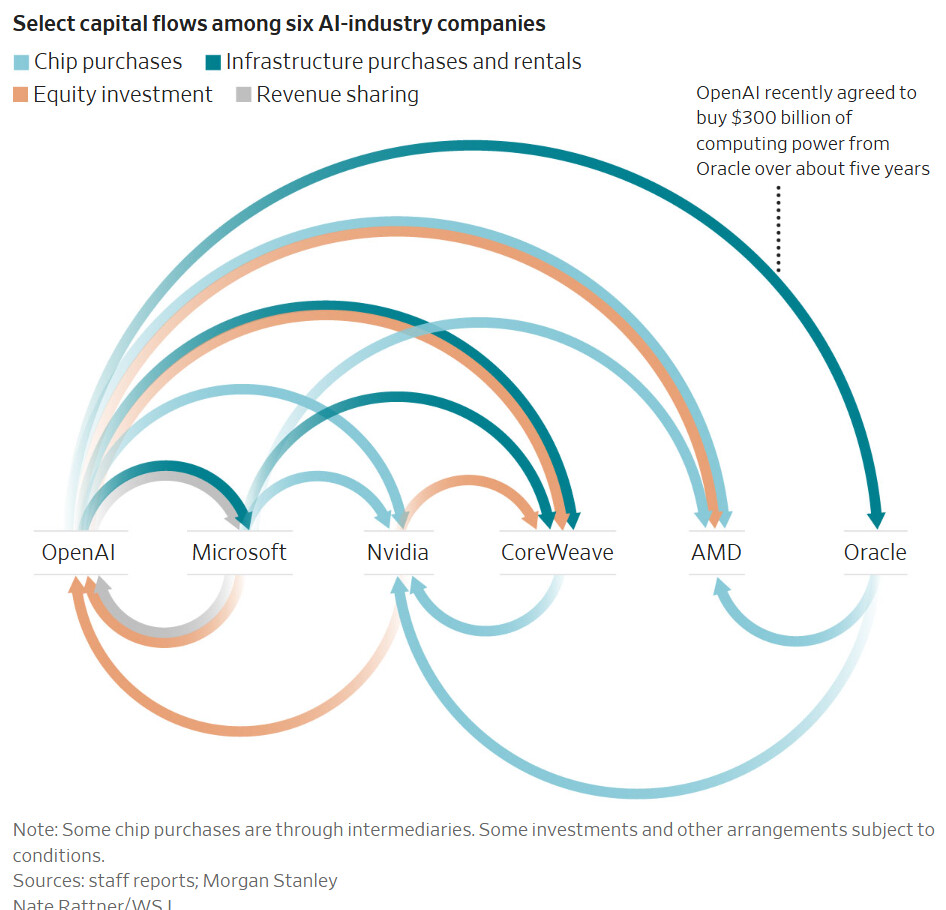

“Circularity” has become a buzzword in artificial-intelligence deals. Some investors have drawn comparisons between the megadeals of today and some excesses of the original dot-com bubble.

o “Broadly speaking, circular financing often goes something like this: One company pays money to another as part of a transaction, and then the other company turns around and buys the first company’s products or services. Without the initial transaction, the other company might not be able to make the purchase. The funding mechanism could take the form of an investment, a loan, a lease or something else.”

GameStop executed an 11-for-10 stock split and distributed warrants with a $32 strike price to shareholders,

[…]

On October 3, GameStop executed an 11-for-10 stock split. The same day, the company distributed warrants to shareholders at a ratio of one warrant per 10 shares held.

No 11-for-10 stock split happend. They only distributed a warrant for 10 shares.

Roaring Kitty returned with a $115.7 million stake in GME shares and $65.7 million in call options, reigniting meme stock excitement

I don’t think that actually happend. Not in 2025 I mean.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.