How much is due to central banks selling treasury/buying gold (ie tons of gold being held/bought) and how much is due to gold price movement?

1 Like

Well, I think:

• Central banks are actively shifting reserves

– Net buyers of gold for years, record purchases recently

– Some are reducing U.S. Treasuries → this is the main driver

• Gold price effect

– Gold has surged in price, so its share of reserves rises even without buying

Rough split: ~60–70% real buying / reserve shift, ~30–40% price movement

1 Like

Looks like this data is “complicated” (Ft Alphaville)

(There’s no official source of data, there’s some industry body publishing numbers, where they might also lump sovereign wealth fund with central bank)

I read the other day that the SNB had sold off a large chunk of its gold reserves not long ago and there was some popular attempt to try to stop this.

Isn’t this the cue for the big, scary “currency doesn’t matter” crowd?

My simple and simplistic mind says “if I make X% more in USD than I lose in USD/[currency I need] then it’s net positive”.

1 Like

You should add holding time and interest difference to your formula. Over longer periods of time sometimes the interest difference turns the forex gain into a loss and vice versa.

Anyhow, as I am one of the

When comparing to stocks the volatility of currencies are peanuts.

I am not that sophisticated, have internalised the 80:20 rule, and approaching most things with an Impact/Feasibility prioritisation matrix, so many years in consulting finally left a mark, all that corpo jargon has some practical wisdom!

1 Like

I would say the 20% of efforts that do 80% of the job when it comes to evaluating the value of our assets for our own spending needs is to buy an accruing ETF in CHF.

That way, you only ever see the value of your portfolio displayed in CHF and whatever fluctuations happen to the same stocks when denominated in USD or another currency simply never happened to you (as, in theory, they don’t even if you hold funds with shares denominated in USD).

Edit: the slightly more complicated and less fee efficient way to do it for those who want to see dividends distributed is to use a distributing fund and then immediately convert the dividends in CHF.

I would recommend to differentiate between investments in stocks vs bonds/USD.

If demand for USD goes down , it would mainly impact the forex rate. But the investment in a stock (company) is independent of currency in which the stock is bought.

Of course if stock returns are not enough to compensate for currency devaluation, then it will be a loss for CHF based investors. But I think the chance of stocks underperforming CHF savings accounts in long run (>10 years) is very low.

1 Like

The stockmarket of a country in aggregate is still correlated to its home market currency (isn‘t necessarily the currency you buy the stock in of course, but for US stocks, USD has a correlation). Depends of course on a trillion factors (and breaks down on individual stocks), but there is a big effect still in aggregate.

Cederburg could be seen as indicating this.

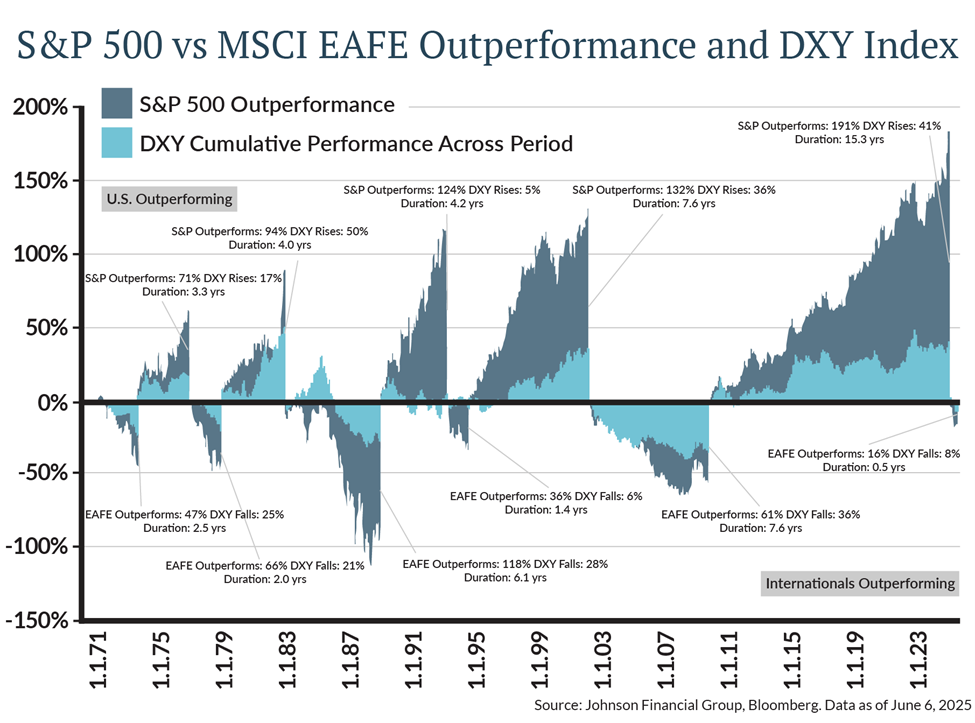

This chart is also pretty telling imo:

From here: The US Dollar and Why International Stocks are Outperforming YTD | Johnson Financial Group

3 Likes

Yeah, eyeballing it the area above the base line is about 3 or 4 times the area below the line.

It that what you meant to distill out of the chart?

![]()

Well, I think it might be correlation but is it really causation?

An appreciating currency is often a sign of economic resilience and real growth. But I think the underlying factor here might be economic growth rather than currency vs stock market correlation.

This is not to say that S&P 500 is guaranteed to outperform CHF savings accounts over the next decade. But I think the chances in my view are quite high. US has debt issues and political instability but not sure if it’s enough.

No, that part of the performance difference is the USD strength and that USD strength (or weakness) generally correlates with over- or underperformance compared to ex-US.

The article makes some causal links as well.

Might be part of it.

It’s not conclusive by any means and it’s not always the case as well definitely. But I do firmly believe currrency over a whole stockmarket has a lot of influence.

This breaks down on the individual stock level for sure.

Huh. I see. Interesting.

I’m too simple minded to notice a difference versus what I meant to say (“US overall outperforms the rest of the world in the past 50 years or so [USD denominated or not]”), but never mind. I don’t have the data to prove it.

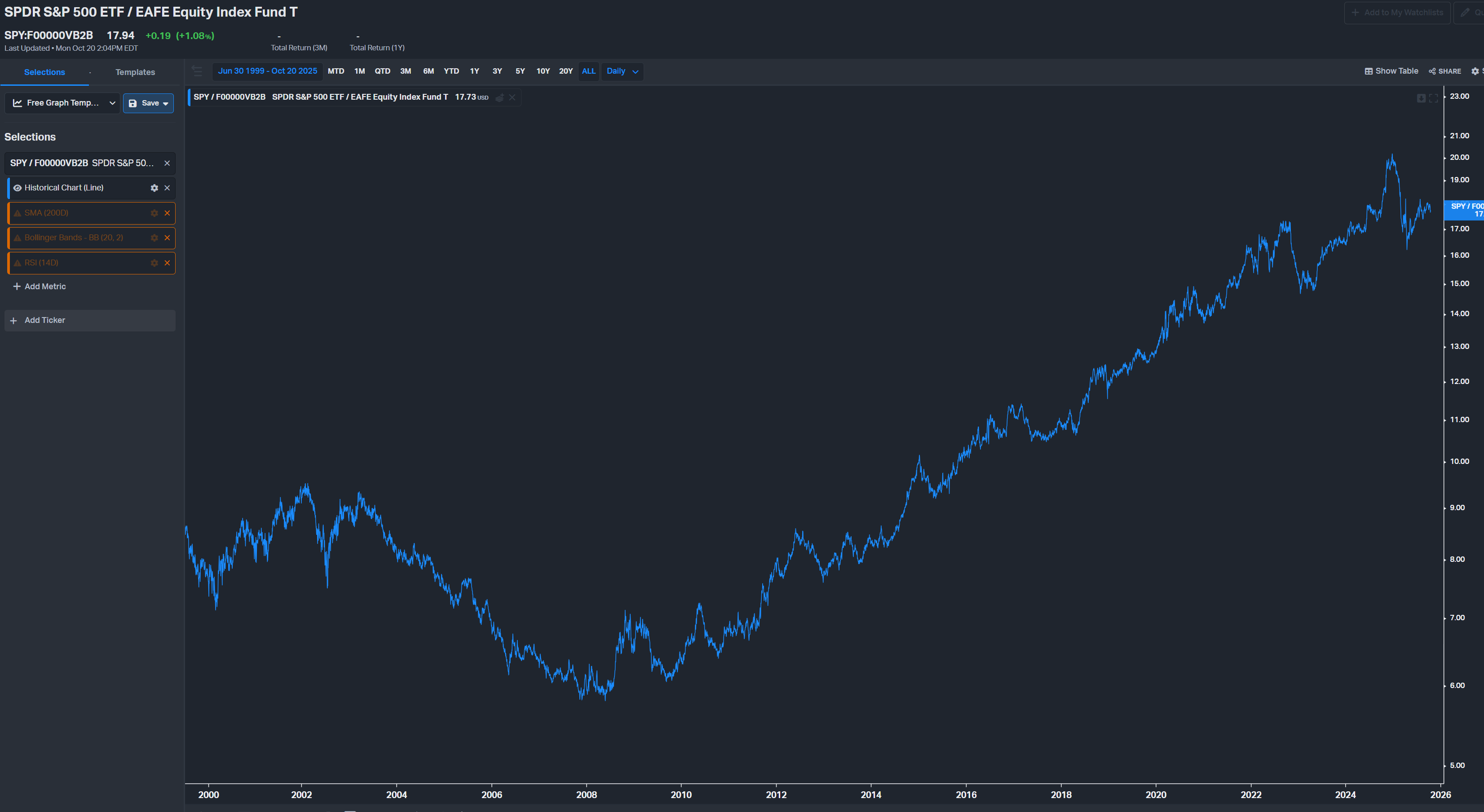

Looking at SPY/EAFE in koyfin for the max period available (since mid 1999 apparently), we seem to have SPY outperforming EAFE at close to 3% p.a., resulting in a well, over 2 x total (price) return over EAFE over the period.[1]

Note that this includes the dot-com bubble.

I’m dense, I admit, but what did you mean to express with the chart cited? I read said article, and all I took away was Drake Dorfner speculating on some patterns that international stock allocation will help with volatility in the overall portfolio?

D’uh?!

Apologies if I missed the finer points.

1 SPY/EAFE

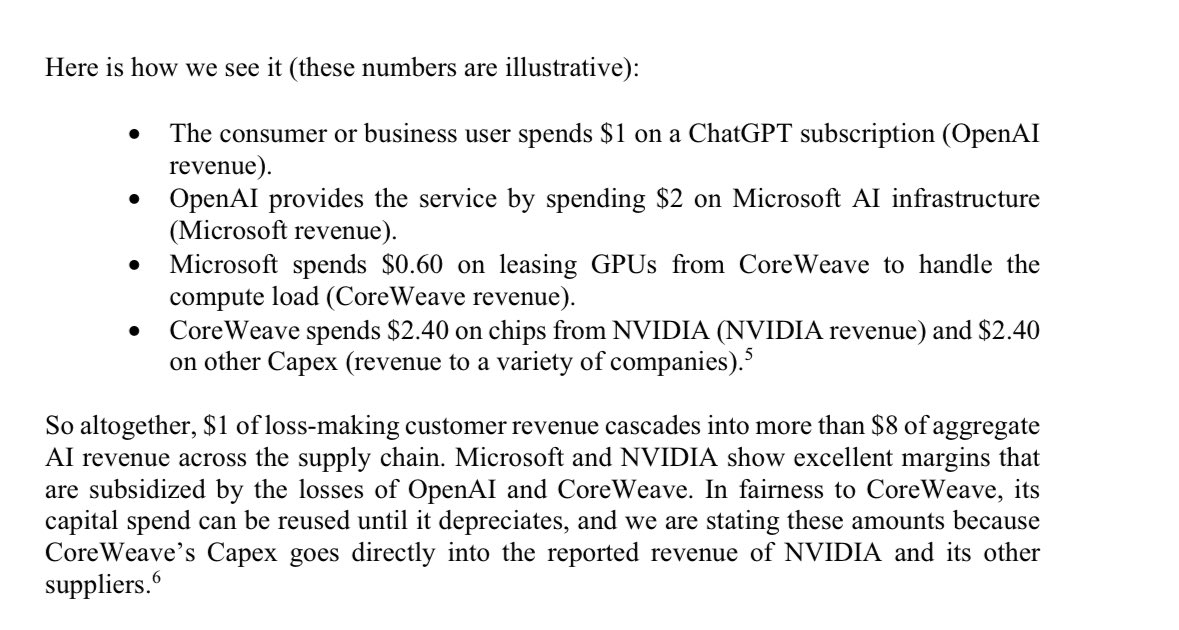

More from David Einhorn (apparently via a letter from Greenlight Capital to its clients).

(found here)

5 Likes

Where does he get his $2 figure from? Paying customers are a small fraction of total users, so cost of serving paying customers is just a fraction of the cost of serving all customers.

I take it more as an explanation of how literally passing a buck around is recorded as a ton of business being done, and almost none of it is profit.

I’ve been wondering since these spaghetti diagrams started circulating the net if this will be know as our time’s Lehman Brothers and Enron moment. Edit to remain balanced: Enron was plain criminal fraud, and Lehman was overexposure to toxic products. Maybe neither is the case in this AI revenue Krebs cycle? Maybe financial fraud and shenanigans attenuate over time like viruses do and we get, at worst, a protracted soft landing?

3 Likes

Recent article in the Economist (paywalled) picked up on the life-span of server assets of the big spenders from an accounting perspective, and how changing those policies (which they apparently did in past years) impacts earnings by several percent.

"if all these servers lose their value in three years rather than however many each company assumes, their combined annual pre-tax profit would fall by $26bn, or 8% of last year’s total.

At the five companies’ current ratio of market capitalisation to pre-tax profit, this would amount to a $780bn knock to their combined value."

I’m not an accountant, but when I wanted fancy equipment in my youth, I certainly did justify the price tag with how long I’m gonna be able to use it.

Question remains, what is a realistic life-span for this stuff, leaving other considerations like taxes etc. aside?

1 Like

Hopefully the business has found its holy grail. Porn will apply the correct multiplier.

The day we get full body sensory VR I am gone from the world. Of course pr0n will be where I’ll spend about half my time, and games will be the other half.