I am exploring the idea of buying vs renting in my particular case.

We are a family of 4 and in the canton we are located, to rent a 3 bedrooms apartment you need 3-4k per month for rent.

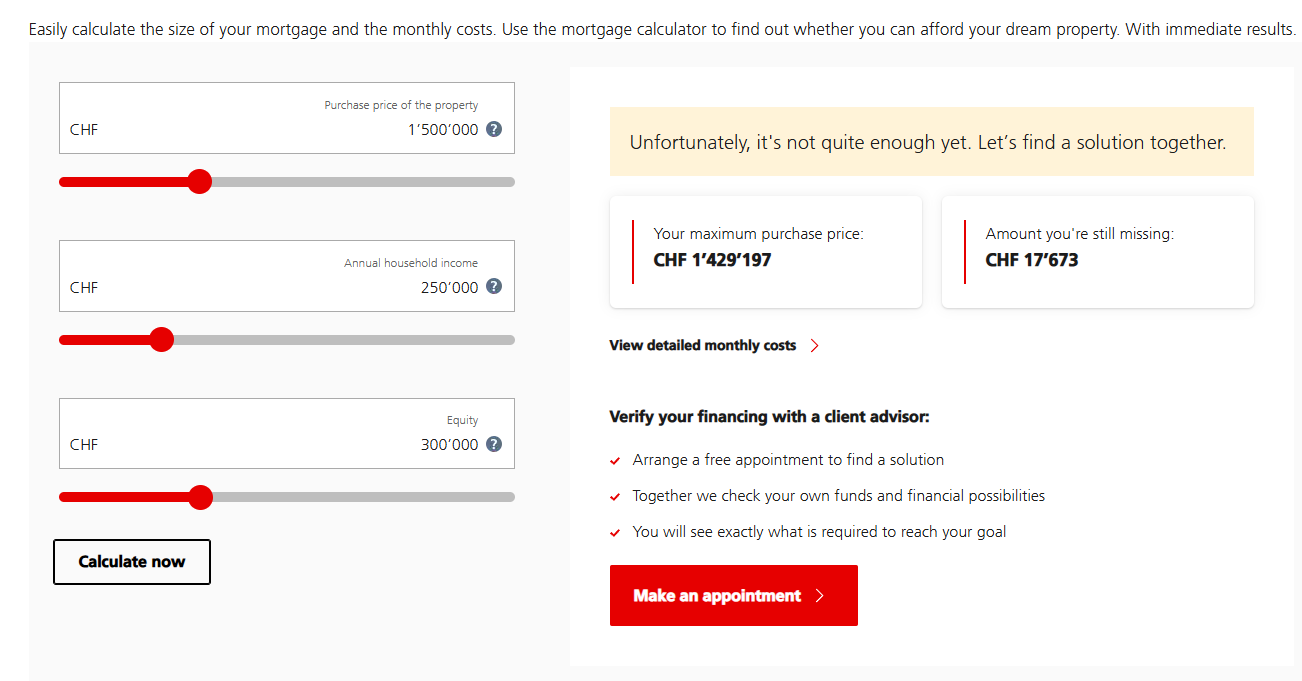

Let’s assume that someone finds a property around 1.5M and also assume that 20% is given as downpayment. Let’s also assume an interest rate of 1.5% for the mortgage.

This means 18K per year in interest payments or 1500 per month. This is a big difference compared to the 3-4K rent case.

Let’s also assume 10k per year for maintenance costs. Again this means 2333K per month cost of ownership.

What am I missing here?

My questions:

in Switzerland, how long are usually the mortgages?

is it true that only interest is paid back and not the capital? If not, what is the real case?

assuming a current wealth tax of almost 0, the property value will be used to determine the tax so this would be (0.5%) 7.5K per year.

(potential?) property taxes (depending on canton?)

own ownership tax

opportunity cost of locked in capital

tax deductions (favourable to the buy scenario, may change in the future)

taking on the risk of fluctuating interest rates

ownership hassle vs carelessness of renting (you are the one who has to call the plumber if a pipe breaks, maintenance costs are not regular, they’re 0% most of the time, then may be a big amount because you need to redo the roof, etc.)

potential issues with the neighbors that can get emotional and aren’t always easy to deal with as moving away isn’t an easy option.

Example in a co-ownership scenario: Problem with neighbor :) The same can happen for single properties regarding access (both to your house and from people passing on your land without your approval), the limits of the parcel, trees/bushes/fences at said limit, people not tending to their garden, etc.

Mortgage duration: 10 years are popular, shorter are possible, ultrashort SARON allowing for quick termination are offered by some banks (but not all, do check if your targeted banks do so before getting serious in working with them if you’re interested in them). You won’t find very long durations. Others will have more expertise than I do on the topic.

The general rule is that 2/3 (often rounded down to 65%) of the property value can be borrowed without a need for amortization. Any borrowing on top of that must be amortized within 15 years (1% of the value of the property per year if you borrow the max 80%). Actual conditions may vary (my bank is handling this in a pretty weird way for my current property, which they deem hard to assess the value of (older single property in a remote location)).

Are you assessing the wealth tax or the property tax?

What usually makes renting more attractive than buying for mustachians, and that people not interested in stocks often miss, is the opportunity cost. If you don’t take it into account and account for low interest rates, owning can very well come on top (doubly so for the average swiss person who doesn’t save a dime if they don’t have to, in which case, amortization can be considered forced savings).

I only mentioned wealth tax but indeed there is also property tax.

Concerning the opportunity cost, I am aware of it. However in our case we don’t have the hypothetical 30% in cash for a downpayment and we would have to sell a property abroad to use the money for the downpayment for a Swiss residency.

Just a word to the calculator: if you use debt it is more risk. If you use the same risk in other investments the (missed) returns over decades will be much higher than the ones used there. The return of a house (saved rent, saved taxes etc) is much higher in proportion then the debt interest. But this is the same with other type of investments.

They should compare apples with apples.

For the last 40 years we had a boom in real estate in Switzerland. Two generations have not seen a bust, but that does not mean there will be none in the future. Risk is risk and debt rises the risk… it should rise the long-term returns too, no matter if the investment is in real estate or in stocks.

We see the effect of mass immigration, the votes on limiting building land, the trillion CHF the 2nd pillar has to invest in Switzerland and the effect of inflation on building costs and so on. Some of those will not continue forever and so the real estate boom may end sooner or later. It was an extraordinary time for real estate in Switzerland and there have been many countries that had such a boom. But sooner or later they end.

Amsterdam has about 600 years of data on real estate and the result: it pays just about inflation rate, not much more.

Before or after leverage has been taken into account?

My feeling is that unleveraged real estate is somewhat safer than stocks. Backtest data in the US gave me something like a rough equivalent to 35% stocks, 40% bonds and 25% cash before leverage.

Leveraged real estate would be something like leveraging a portfolio comprized of 40% of a single stock with good history, that we would expect to still be there in 100 years (think Nestlé, though recent scandals have scratched their image - the Coca-Cola Company may make for a better comparison) and 60% safe and low yielding bonds: usually pretty resilient but tail risk can take everything away (and vulnerable to interest rate risk whether leveraged or not, though obviously more with leverage).

I have not found a single method for measuring risk in advance that works. After the fact however they do work and give hints. But the times they are a changin.

The risk of real estate is difficult to manage while the risk in stocks is somehow easier even to micromanage. You can diversify a stock portfolio and sell fractions of a position when needed, you cannot sell a house room by room. Once the value goes under the needed collateral value the bank will sell it for a garbage price and you may be left without a home and with debt. Now that’s what I call risk,

Of course you have the same risk in stocks or other investments, but as said, you can manage that while you cannot manage it with real estate. Even with the best management the worst scenario can happen, but it is more probable to happen with real estate.

Now, if your risk is lose it all or make some against lose some gain some, I would choose the latter.

That said I own two nice homes. It is not all about money…

I think the historic Dutch real estate index is that one:

Excellent point but the question now is, how can families, that can’t afford purchasing a property, live in CH when crazy rents are only getting more expensive ?

Also, just by thinking how much rent we pay on an annual basis it makes me wonder if we should just return to our home countries with 1/5 of the Swiss salary but at least own our family house.

There are plenty of places with affordable rents in Switzerland. They don’t have the salary level of the bigger cities and not all economic activities can be performed there with the same level of efficiency. Big cities centers are out of reach for many. Each area faces different difficulties which means federal measures have low chances to affect that. The solutions are local.

At regional scales, there are plenty of places that have become too expensive for the people who have grown there to live in so they move out and rich people from, say, Geneva, Zürich or foreign countries move in/use it as secondary residency.

The answer, on a societal level, is zoning and local policies. For many places, this situation is a political choice to attract high income/net worth people at the detriment of less wealthy locals. In some places, the locals are ok with that because they can afford to live in another place nearby and the wealthy folks are an important part of their economy.

On a personal level, a solution is to select a place to live in that we like and can afford. It can mean moving further away and comuting, it can mean rebuilding our center of life elsewhere. We can evaluate whether the places were we can work would be affordable to us with our expected salary when we choose our career path. Very high income professions should be able to afford higher rent, lower income professions require us to think twice before rooting ourselves in high cost of life areas.

For local people who can’t afford to live where they’ve grown, the solution is to band together and lobby their local politicians and/or get into local politics themselves. Some places just haven’t the land available to build more affordable housing but for some places, it is really just a matter of policy. Policies are slow to change, but they can, and if an active and vocal majority of the population wants them to and puts actions to their words, it gives much better chances for the process to happen quickly and efficiently.

None of this is easy and several actions would need time to deploy their effects even if taken now. Some of the choices we’ve made are in the past and we are left having to deal with them. That being said, we do have some level of agency still.

I’ve seen 30% float around. I don’t know what the official metrics would be. Leeway remains for personal choices (one can afford a higher rent if they have lower expenses elsewhere or might choose to live in a less comfortable place with lower rent in order to afford other expenses and/or savings).

FWIW in a city like Zurich, the goal is to increase the amount of non-profit managed housing (Genossenschaft), I think it’s currently 25% of apartments with a long term goal to reach 30%.

Those apartments won’t appear on the regular portals/offers, you need to use something like Baugenossenschaften | Stadt Zürich (sometimes there are waitlists)

the banks for the affordability calculate that housing costs (amortization + interests + maintenance) must not exceed 33% of gross income (not net).

I think roughly the same can be considered for rent.

I understand the calls for “affordable living” in Switzerland. But you cannot have it both ways: either the market decides or the politicians do. Guess what comes out better…

When I started my second job in winter I had to live in a small flat without bathroom. To take a shower I had to go to the public indoor pool. I just could not afford a “normal” rental place at first.

I spent summers in the Zurich camping ground which charged CHF 5 per tent and day. You had to pay for the shower, but it was right by the lake so no need.

The real estate boom may come to an end, but the rents probably stay high because they are highly regulated.

Today, at the all time high of a real estate boom that lasts already almost 40 years, buying is more expensive than renting. You have to use debt the same way when calculating returns of several asset classes, and there real estate loses.

So, because of this real estate bubble and (too) much regulation, renting is actually cheaper than buying. This may reverse once the bubble will pop. Didn’t happen for 40 years but will happen as sure as the sun will rise; it will happen when all the banks and all the analysts shout out that it is impossible. Like it always did…

But I’m less sure it will happen anytime soon with a big pop: much of swiss real estate is owned by insurances, banks, etc. and required to invest in Switzerland.

As only ~40% of swiss residents own their home, you would need a lot of them in need to sell quickly to make any difference in the market price: difficult with the much more stringent requirements for financing WRT the end of the 80s/90s.

I would rather see the market go sideways, losing value more because of inflation than a real drop in prices like in the 90s.

Of course nobody knows about wars/pandemics/social unrest/climate catastrophes/etc…

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.