Financial institution, mainly pension funds, are one reason for the bubble. But not the only one. I would say immigration, land scarcity (mainly artificial due to some votings) and the good financial general state of Switzerland are the others.

Could not find the total value of all Swiss real estate, but found the average person occupies 45m2, the price per m2 is CHF 8’200 average and we are probably around 9 million people living here. That is 4582009, more or less 3.3 trillion. 2nd pillar in 2022 was 1.066 trillion, grows 8% per year so lets say it is now around 1.25 trillion. I suppose it will start to shrink sometimes in the future. And not everything is invested in Swiss real estate, let’s say 1 trillion. So it is about 30% of all Swiss real estate. That is quiet a lot!

There is a tendency to limit immigration and the birth rate is sinking. So that factor could cool down too.

Now, inflation and general problems in the financial industry and tariffs could hurt the good financial general state of Switzerland. We have not much industry left and almost always are the most expensive place to produce anything.

We still have enough building land but it is limited due to various votings. I don’t think politicians will touch that, so land scarcity will stay an important factor to support the sky high prices.

But only one or two of the four factors (pension funds, immigration, general good financial state and land scarcity) have to change to make the bubble pop. And then it will happen very fast, as the private debt is sky high.

P.S. to the pension fund investments one probably has to add debt, so it may be more. At 50% mortgage it would be 60%. That is scary…

Hmm, difficult question. We are definitively in a boom, 40 years of rising prices. The last part of a boom I would call the bubble, everything speeds up. No idea if we are there already.

I think you can say we are in a real estate boom. The bubble will not be in sight after it pops. And the chances for it to pop are highest when nobody says that we are in a bubble…

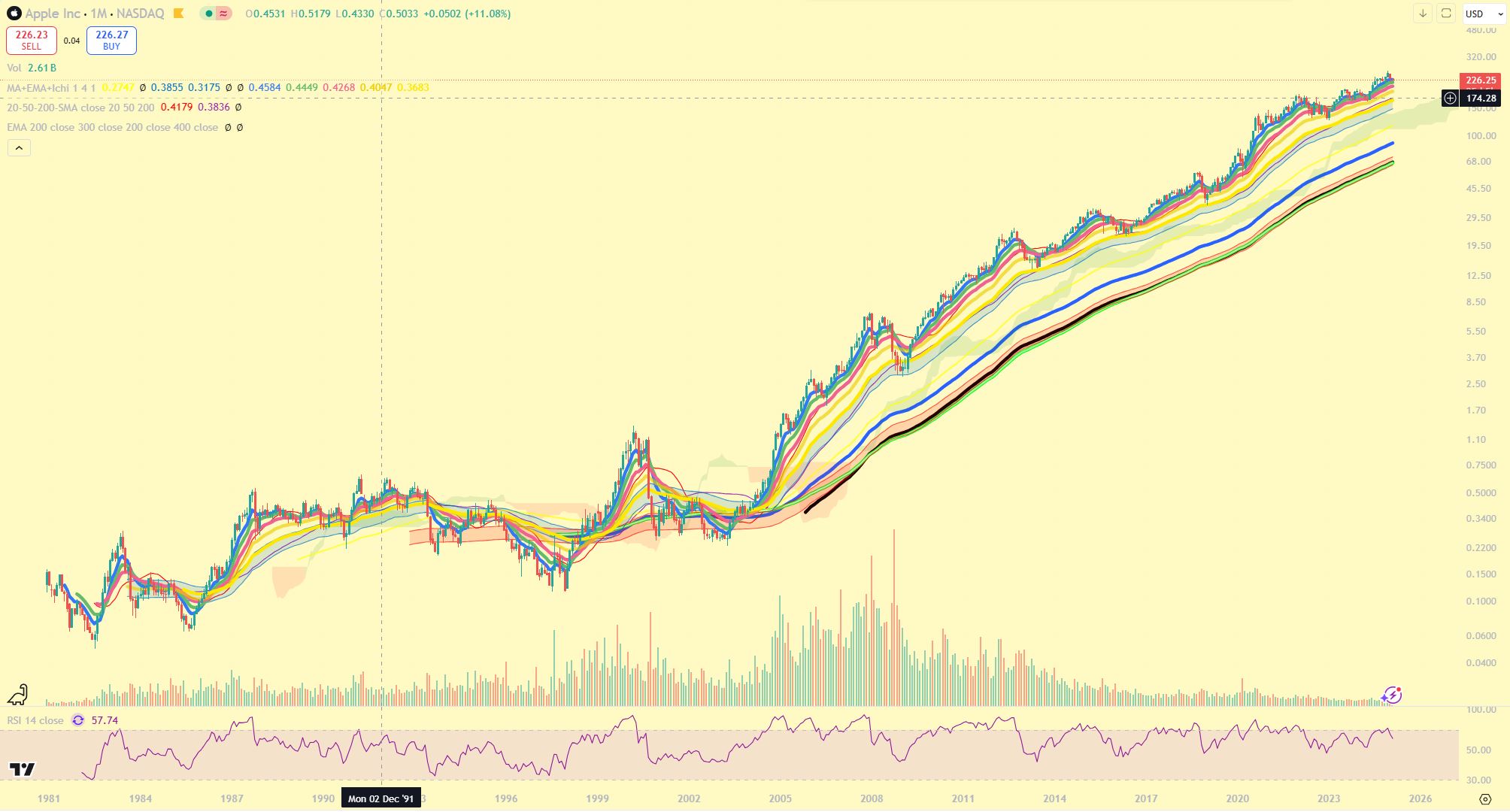

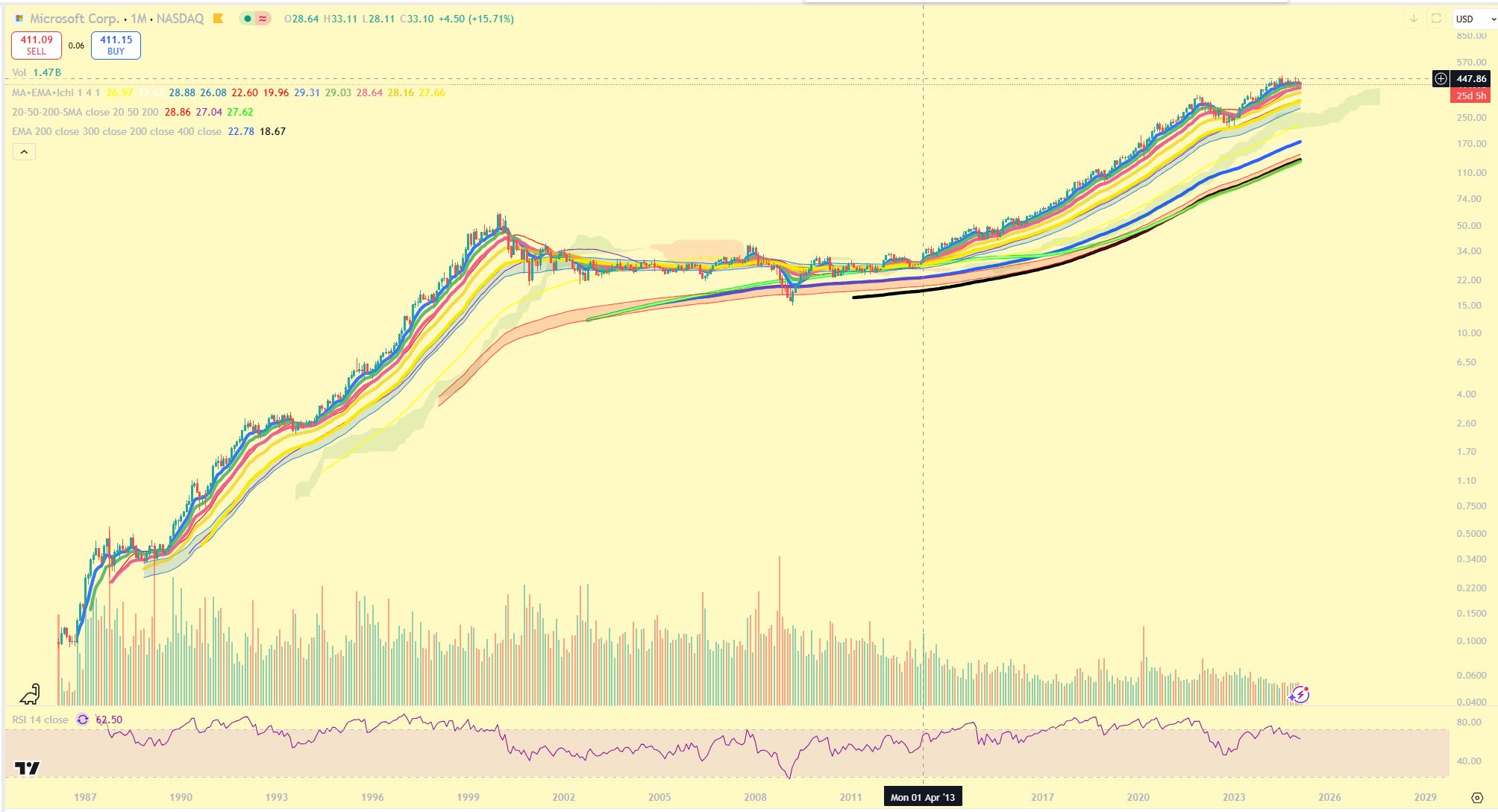

I show some pictures of a longterm logarythmic chart - Bitcoin (who most think that is a bubble), Apple, Google and Microsoft. On a longterm logarythmic chart they all just look very strong and none of them like a bubble. So maybe the Swiss real estate market is just really strong, with constantly additional financial potent people coming to Switzerland and pushing the prices up and up.

Looks nice, but to repeat, comparing apples with apples including returns (that would be saved rent) and with the same leverage, stocks did way better:

On 20% capital many people buy real estate in Switzerland, that is a margin of 500%. Deducting mortgage interest the return would be more or less the same like stocks at 100%. But at what risk?

With 100% margin on stocks you can hardly go bankrupt. With 500% margin on real estate you can… and will if there is a bust. You end up without a home and with debt.

And as I said, even if you go to more than 100% margin on stocks, you can micromanage the risk; you cannot do that with real estate you are living in.

Thanks, for that info. of course you are right. TradingView can compare including different currencies, didn’t know that feature, here it is in USD and CHF:

With 100% margin on stocks using a margin loan on standard terms, your position can get liquidated the moment the market blinks 1%. It is a rather risky position to take.

Of course, way higher leverage can be achieved using futures, options or other products.

I think once the external factor which makes the bubble burst it on the table, some might want to sell quickly while no one wants to buy. AFAIK prices can also sink like a rock because the demand is gone and then no extra supply is needed

Sorry, my English: with “margin of 100%” I meant no debt. A margin of 500% means 20% down payment, 80% debt. Probably there is a better word for that. I remember the word cash margin, which was used as a multiplier, 1 or 100% means all cash, 500% means multiplied by 5 as 100% cash and 400% on debt.

Actually I think with stocks “margin” is the collateral. So probably I should use “margin multiplier”? But then collateral is always 100%, so I left out the word multiplier.

Actually, it’s my mistake: I tried to adapt to your numbers (I use leverage mulipliers myself, that work like your margin % and that I find easier to grasp) and failed to consider that by that logic, 100% margin means x1, so no leverage.

I’m no specialist but by my understanding, margin is the collateral. It applies to the total assets so someone who owns X stocks and borrows X ends up with 2X assets and X collateral (or 2X/2), for a margin of 50%.

OK, in my wording it would be a margin (collateral) multiplier of 2 aka 200% (actual value divided by collateral). In your wording the collateral is compared to the total value in reverse and therefore it would be 50% (collateral divided by actual value). Both are OK for me, but probably somebody can help with the exact wording…

My last job was with oil tanker shipments, involved futures, insurance and regular re-evaluation of margin during the transport time. But it is so long ago, I cannot even remember the correct wording. I think it was like cash margin, (actual value divided by collateral). But it is too long ago, sorry.

My broker, Interactive Brokers, says I have 800% stock trading margin available, portfolio margin. So it seems like they use the same wording as I do.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.