Understood. Thank you for the details.

My CSPs still had 1-2 weeks of life left but they were assigned before expiration as they were deep ITM.

Understood. Thank you for the details.

My CSPs still had 1-2 weeks of life left but they were assigned before expiration as they were deep ITM.

Experienced that once, too, although the Put was only at the money or maybe a tiny bit ITM.

I remember feeling quite surprised, but I guess this is part of the American style option where the buyer can exercise before expiry if e.g. they need the cash.

Throw Goofy a bone and surely he’ll chew on it. ![]() *

*

I’m starting to chew on this bone and am slicing (breaking?) it across these three kinds of risks:

(quoted unhumbly from your mostly friendly neighborhood goofy dog, yours truly here)

Fundamental risk:

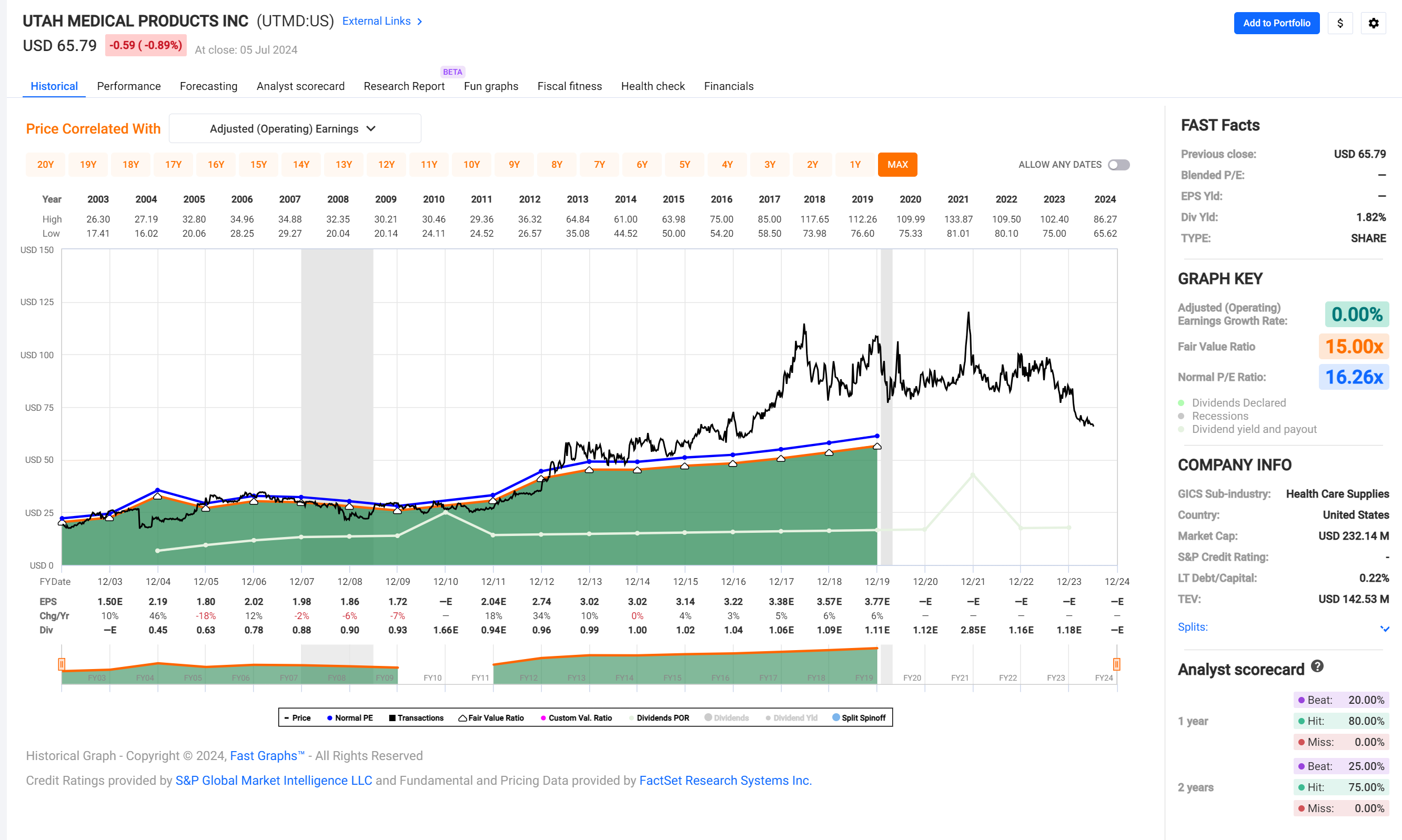

A little hard to tell given it is a microcap. It’s been in business since 1978 with a couple of murky episodes in the first couple of decades, but seems steady and growing for about the past two decades or so.

Their primary products are healthcare for women and their babies, they are geographically somewhat diversified (60% US, rest among other English speaking countries).

Conclusion after the whole exhausting 5 minutes of relentless scouring their Bloomberg description: doesn’t look like a whale oil or a snake oil company, not exactly $ES or $JNJ, either, but probably … or at least maybe, fine?

Valuation risk:

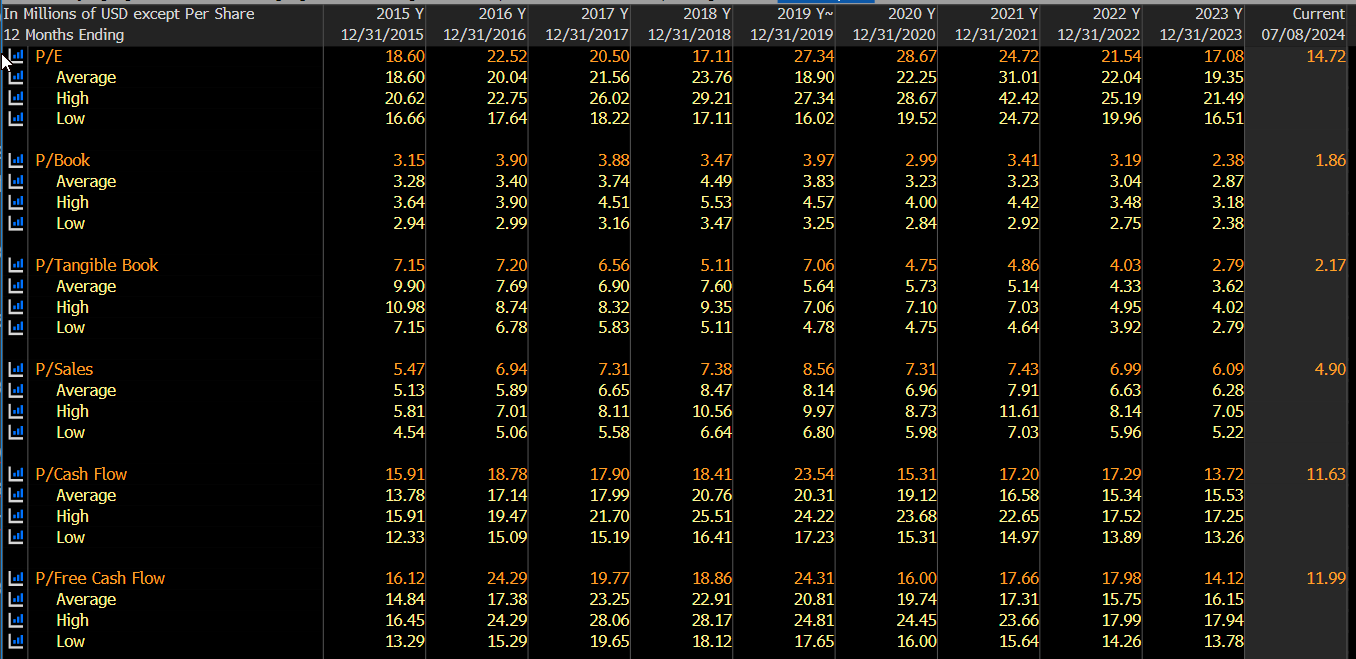

FASTgraphs is partially letting me down on this one as apparently FactSet doesn’t have any recent earnings data …

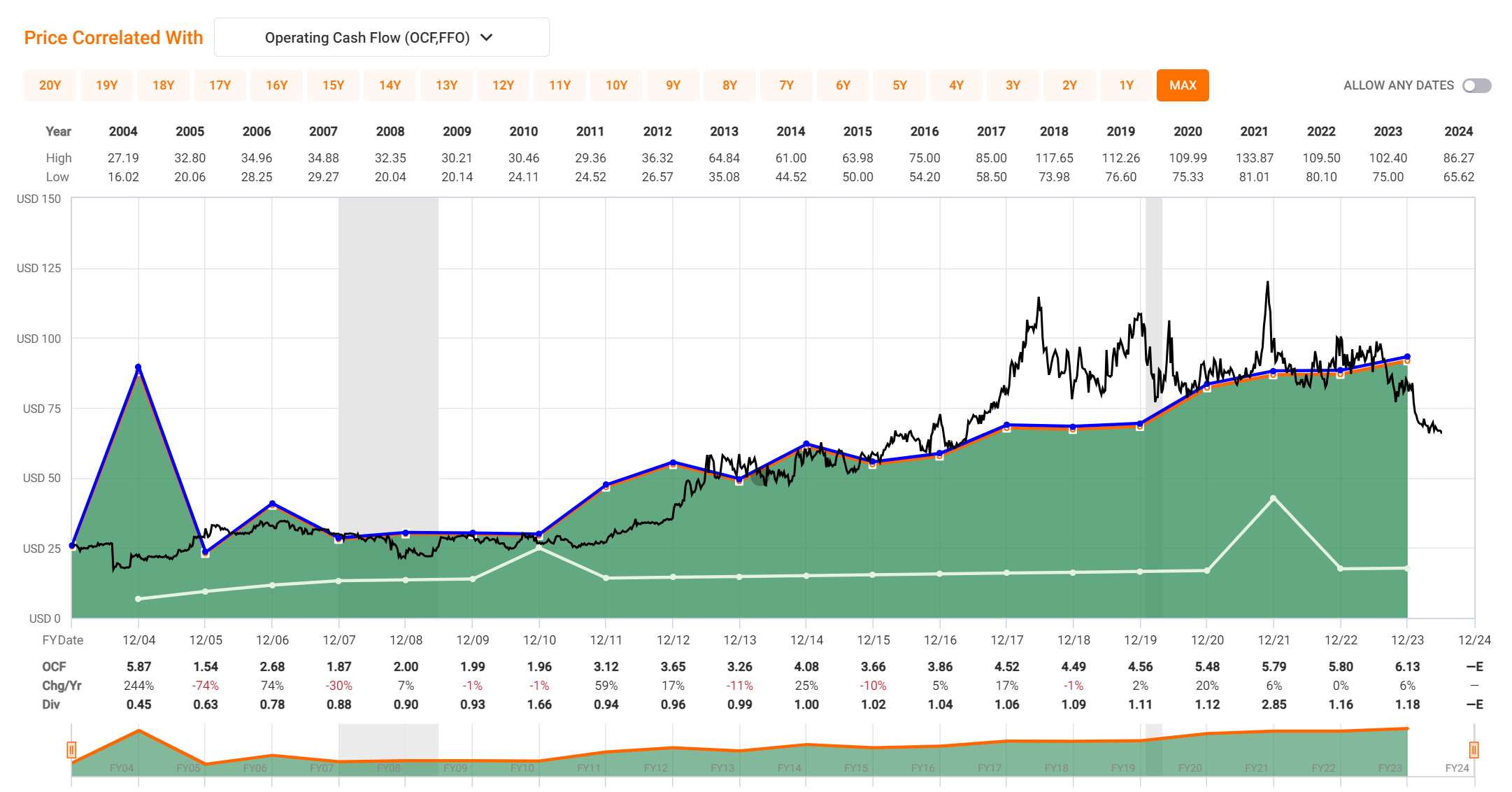

… but at least there’s some more recent Operating Cash Flow (OCF) data:

Looking already promising as price seems already below the anticipated (and probably fair) 15 x 2024 OCF (extrapolated by Goofy’s pea sized brain from the existing line on the graph).

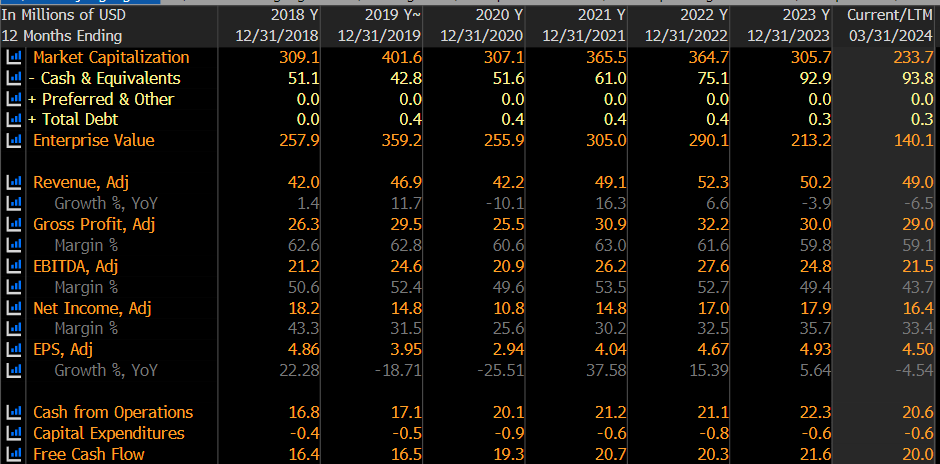

Luckily there’s other data providers, just not in the nice graphical visualization as I prefer it. Based on the earnings metrics data from your link as well as mighty Bloomberg tell us that the company continued growing since 2019 (with a bump or two):

while the PE and other multiples sank (as desired), especially recently:

The only thing that I would want to dig deeper on is that their trailing twelve months cash flow seems to be at (only) $5.69 (per share) versus their 2023 number of $6.13 (or $6.14 according to Bloomberg). Maybe some seasonality with a stronger second half of the year?

Volatility risk: well, my more sophisticated friends on this channel call this the sequence of returns risk, but I like the blunt term volatility risk better as it’s IMO closer to the reality of life where you need to unexpectedly withdraw a gazillion k of your (volatile) investments because of unexpected life event X regardless of the valuation of your investment(s) at the time instead of just withdrawing your planned 3.967614% (rounded) of your holdings in that year.

Anyhow … volatility risk is probably mostly out of your control even with decades of backtesting, as your specific case of needing cash in year Y isn’t included in the historic set of data for backtesting safe withdrawal rates.

Maybe, constructively speaking, the less volatile your specific investment (say, again, $JNJ) the less exposed you are to this, even when the surprise withdrawal is triggered exongenously.

UTMD isn’t in the $JNJ category here – no surprise, given it’s a microcap and somewhat more volatile fundamentals – but you also don’t have to put 50% of your investable income into it.

Diversification is your rescue boat here.

Goofy liked this bone, but is holding off buying into it for now.

Woof!

* In ernest, I like these potential throws and truly enjoy taking a stab at them with my tools at hand!

I’m trying to reduce stocks but finding it hard to part with them. I’m at 75/25 stocks/bonds and want to get back to 60/40 or even 50/50.

What criteria do you look at for your individual stocks? Balance sheet, management, or any technical indicators? Or several at the same time?

Off topic response because point is interesting: Gen X and to a large extent Gen Y (I guess I fall here) grew up in times of huge optimism that big problems for the world seemed to have been solved (Cold War drawing to a close was a big one). Yes, we were worried about AIDS and drugs but I clearly remember being told that it can’t “just happen” to someone, they need to make poor choices to fall into drugs or get infected with HIV. Growing up in Greece in the 80s-90s there was constant bombardment of anti-drug/safe sex information, I believe some of it stuck with us despite being pretty basic (“don’t accept a cigarette making rounds, don’t accept anything by anyone in a party, drugs are not cool, always wear a condom”)

My guess is that Gen Z has seen that the boomers (the real boomers, not what is used to describe anyone who can string 2 sentences without grammatical or spelling errors) royally fornicated with their future, so they say “who cares, the world is going to scheisse anyway”.

Incidentally, I was amazed by how many people smoke in CH.

Edit: interestingly, I can’t help but think back, so many things being discussed by my parents and their friends in the 80s as potential world problems in the future such as immigration, nationalism, climate change - I can’t remember the discussions because I was a kid - were sort of glossed over by economic boom times, and came roaring back as huge problems in 20XX onwards.

I’m using your CH reference as an excuse to look at some Swiss companies with the only tool in my toolbox: the FASTgraphs hammer!

I skimmed the 200+ SPI constituents and came up with a sobering short short list.

I’ve concluded that stock picking for me isn’t really about picking stock, it’s about being picky about stocks …

Only three companies that I would consider today and maybe a good dozen that I would put on my near term watch list.

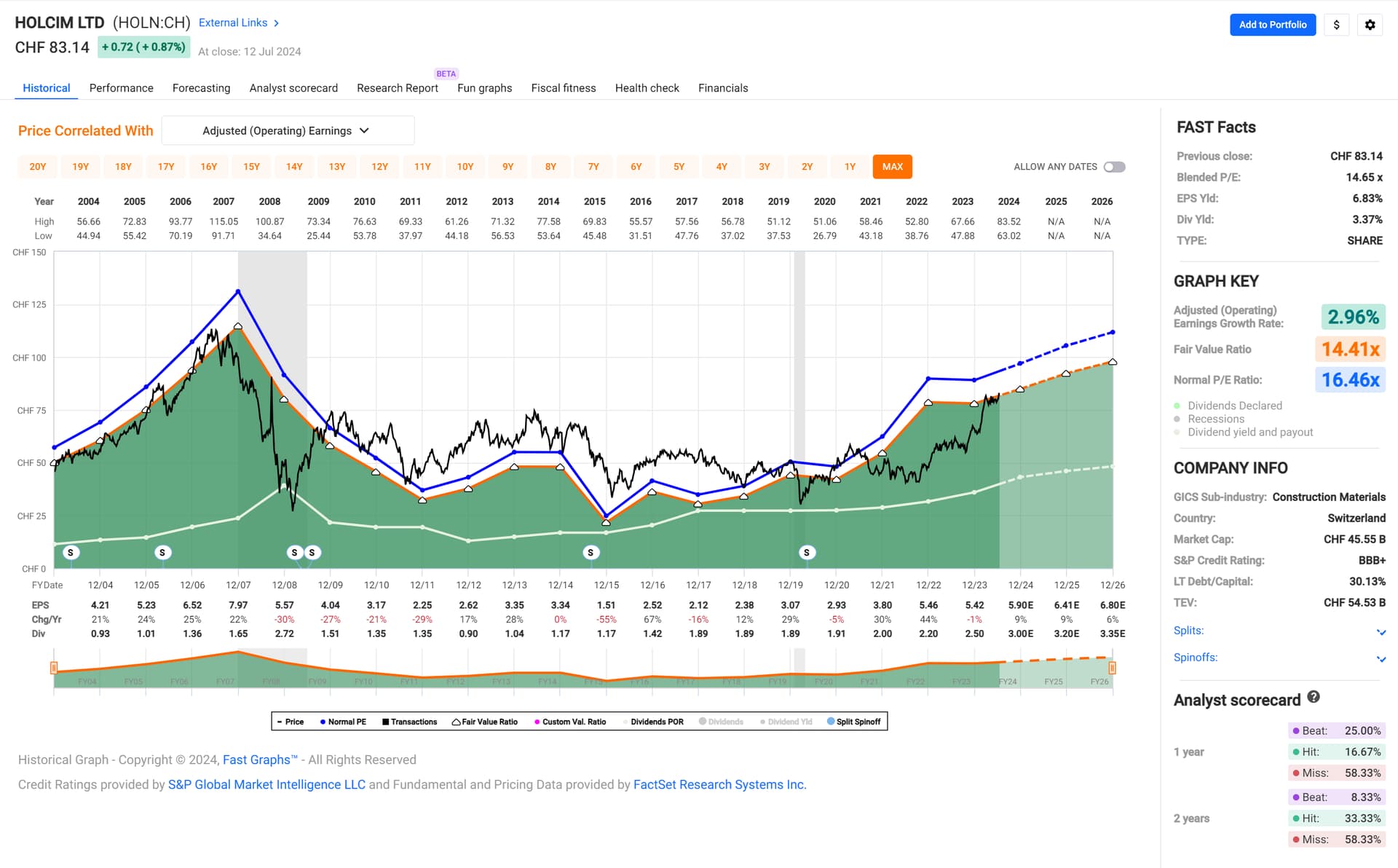

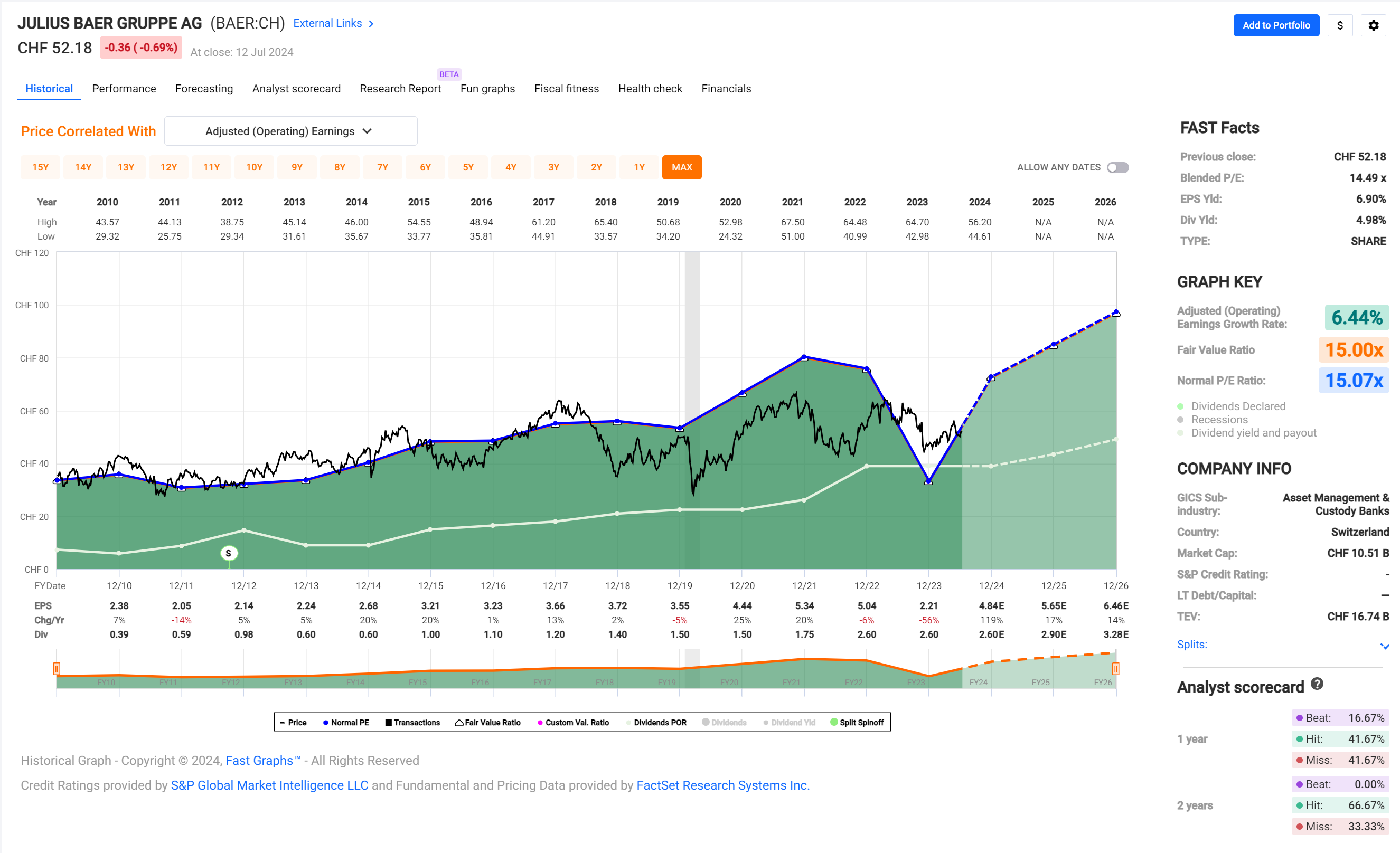

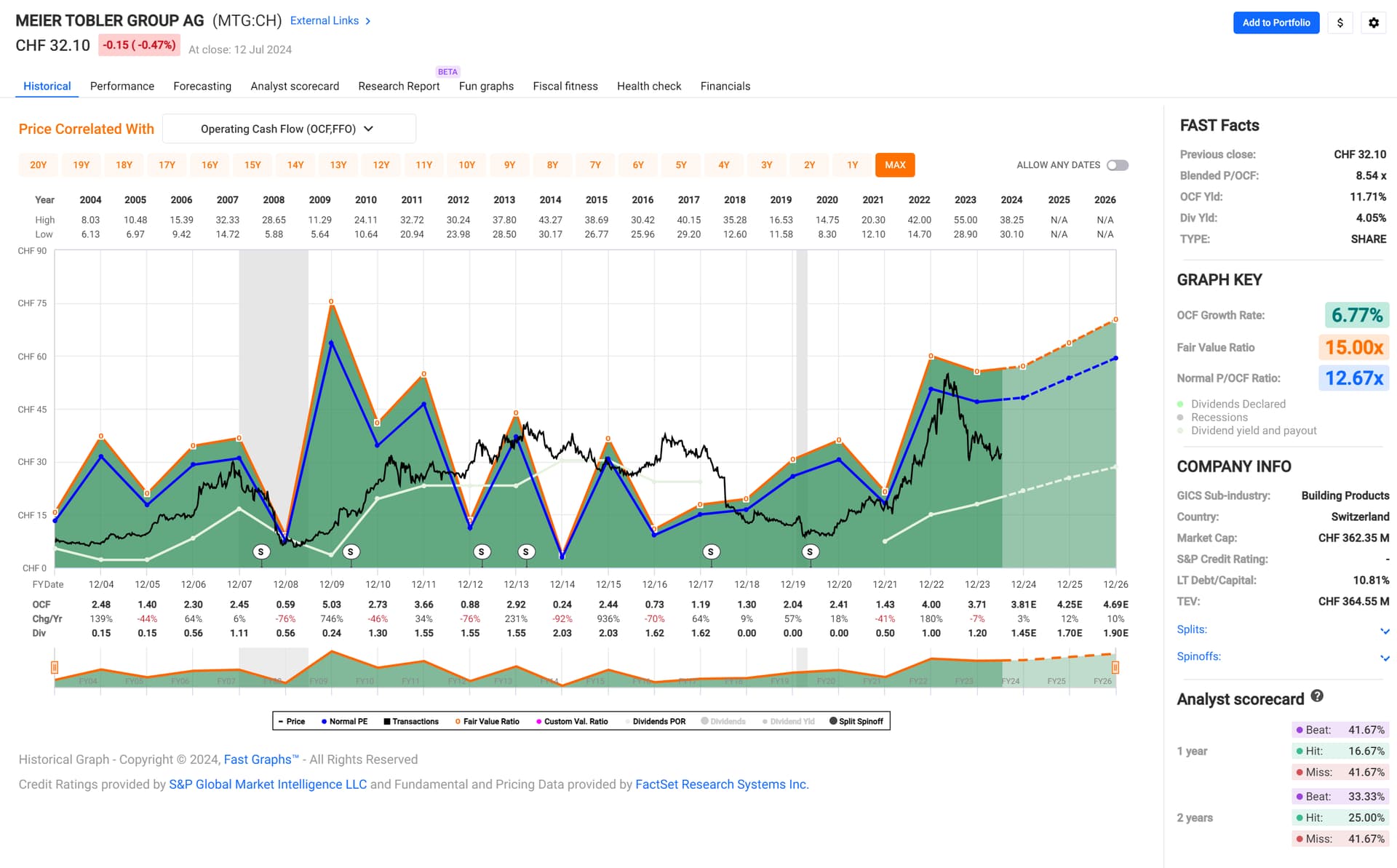

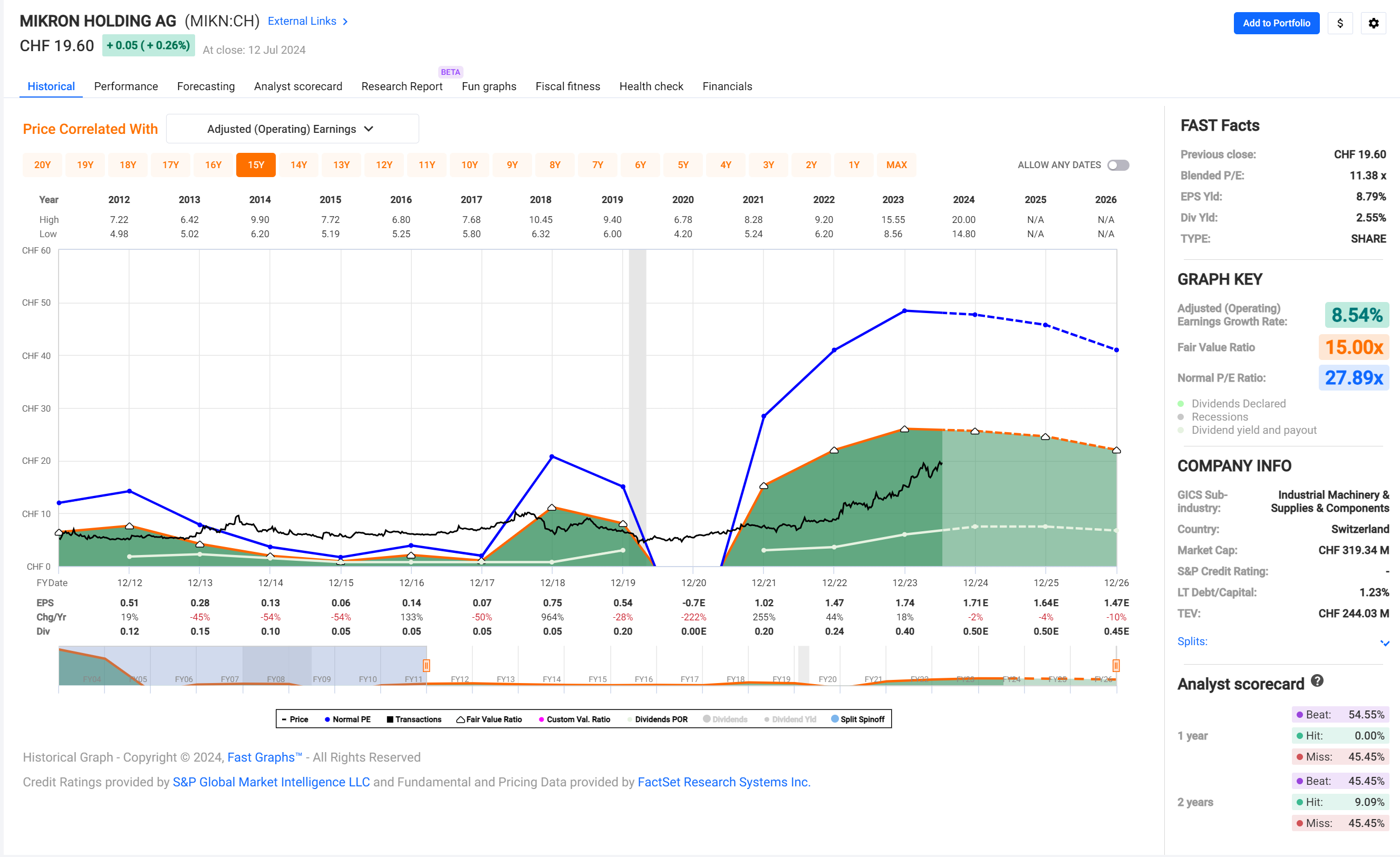

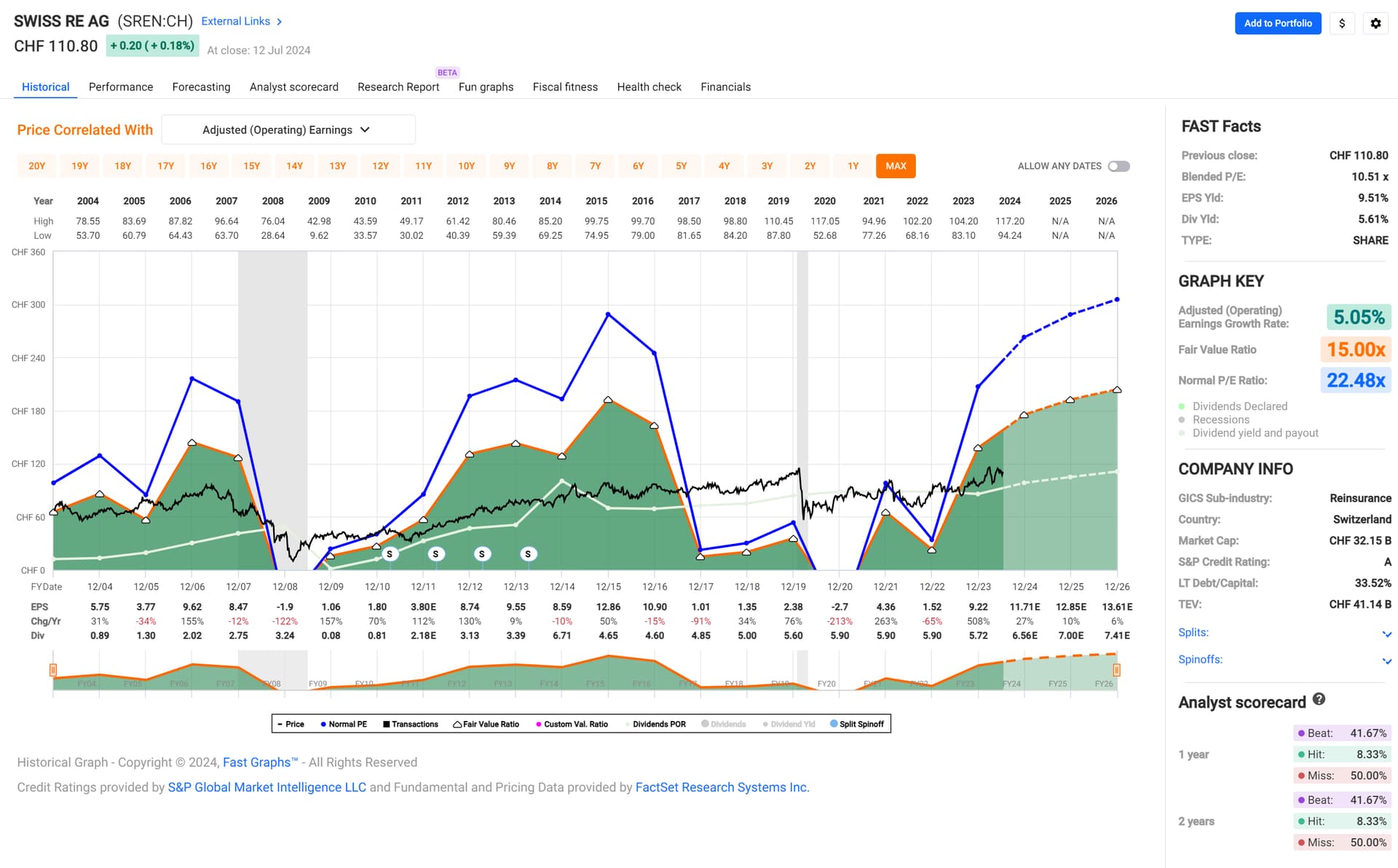

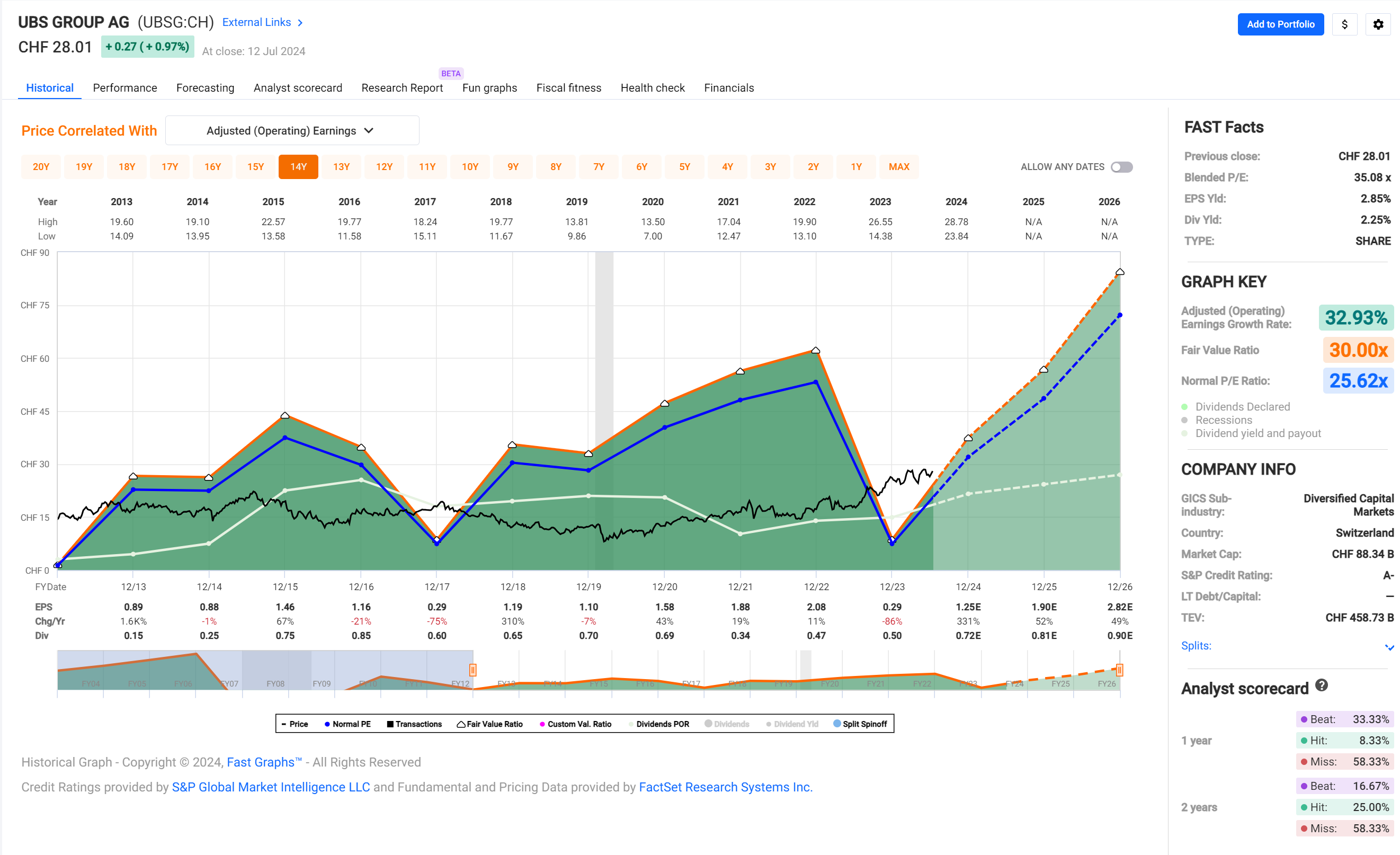

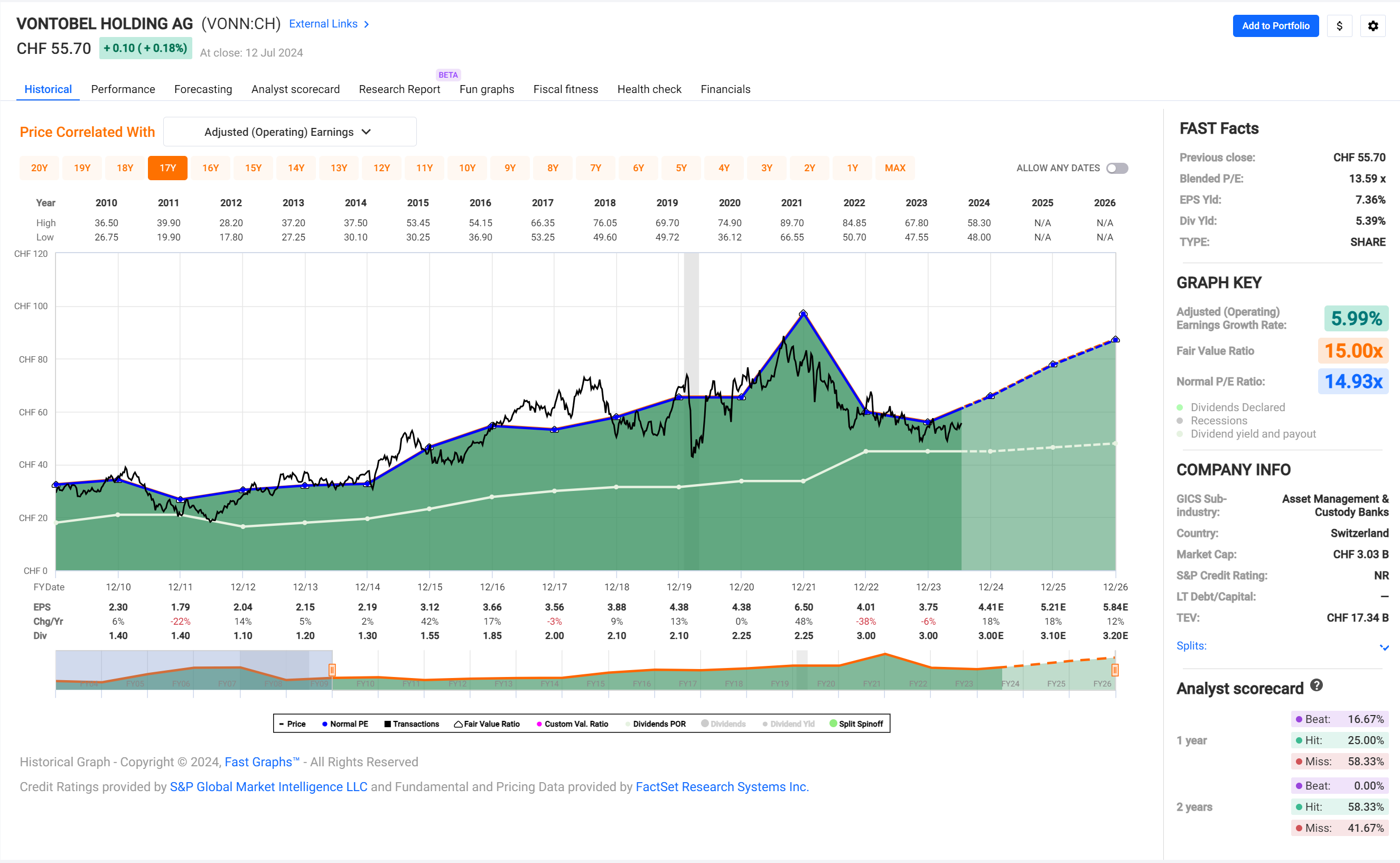

The short list(s):

Buy Candidates: Worth a deeper look, above the first cut.

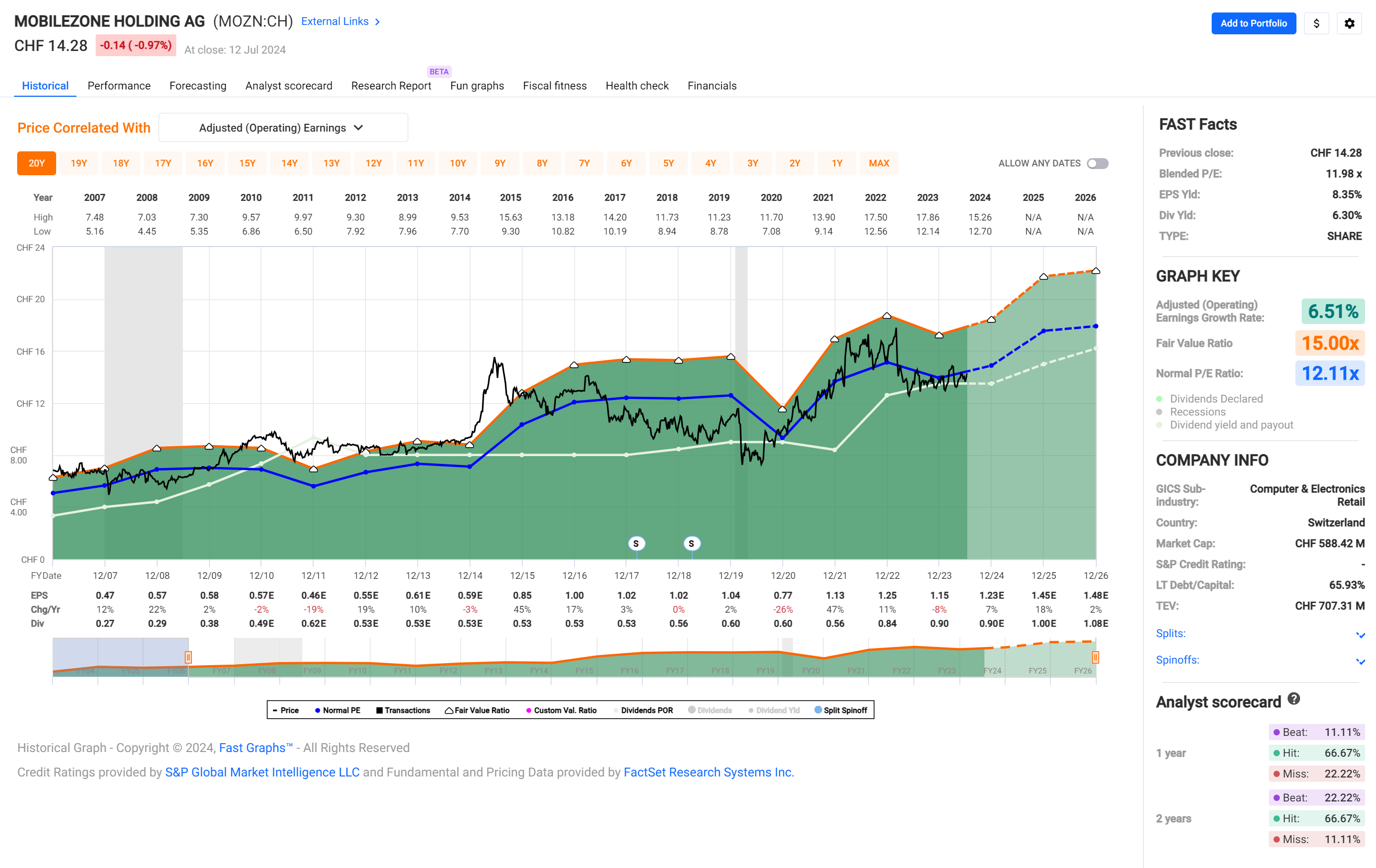

Mobilezone

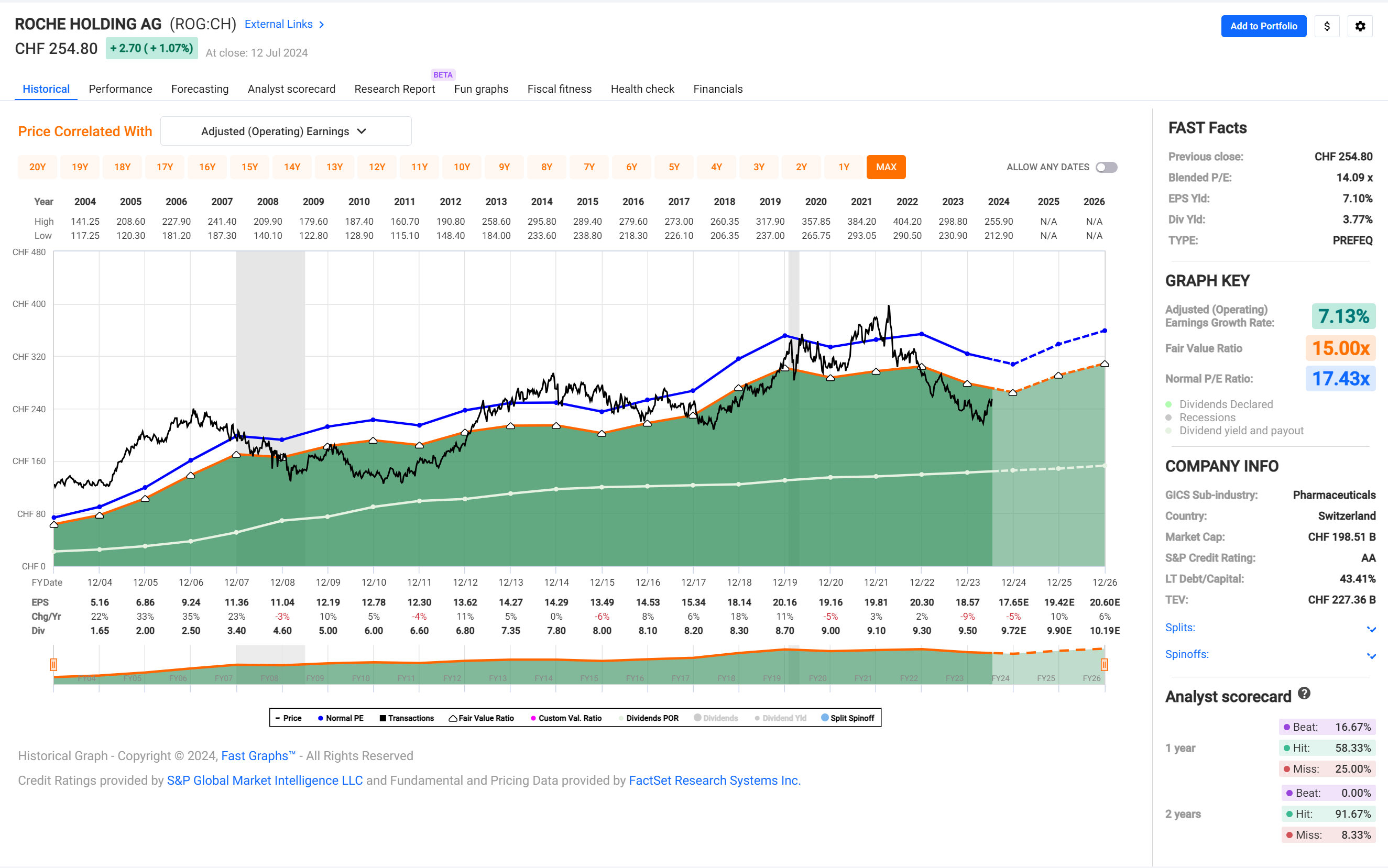

Roche

Valiant

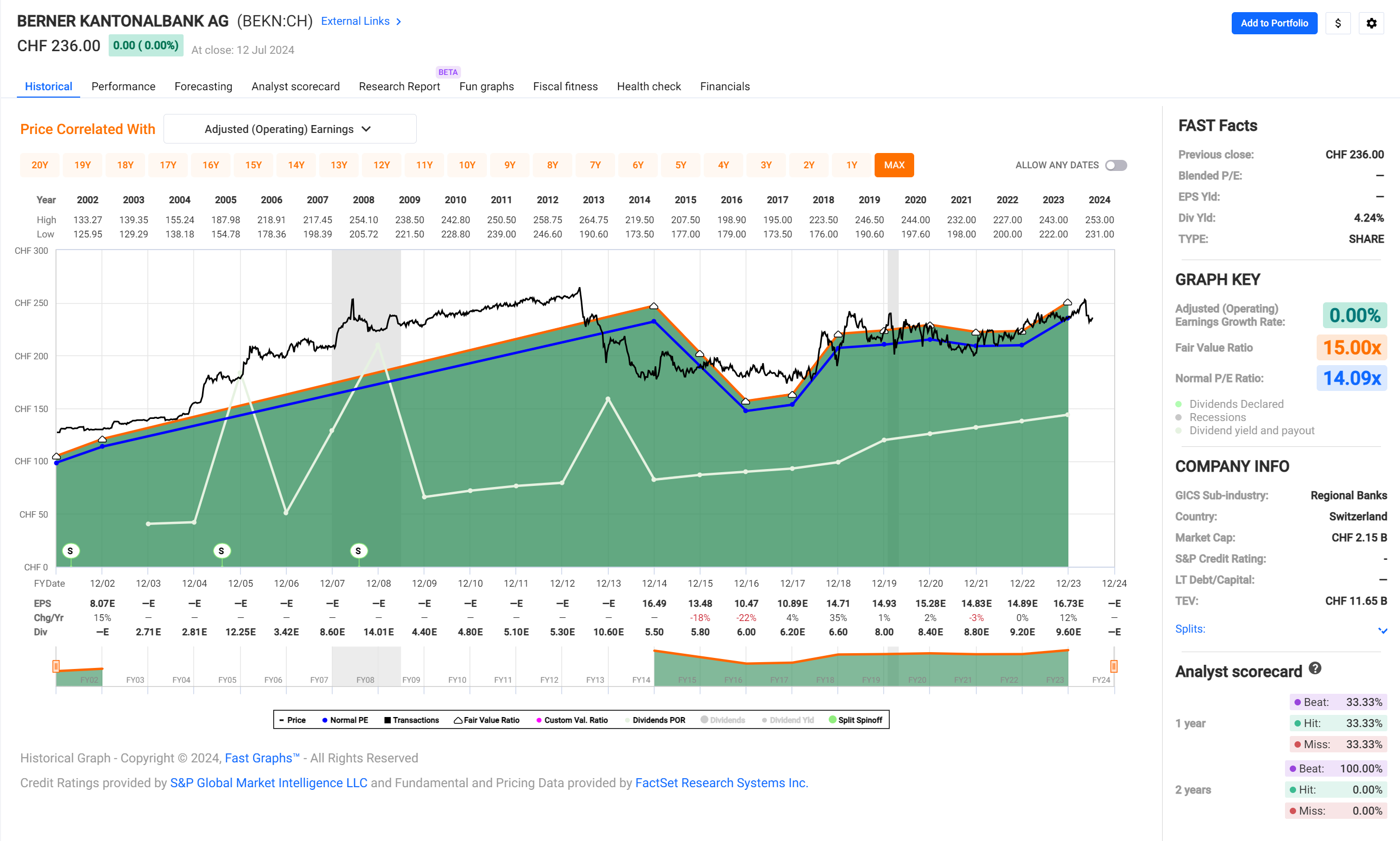

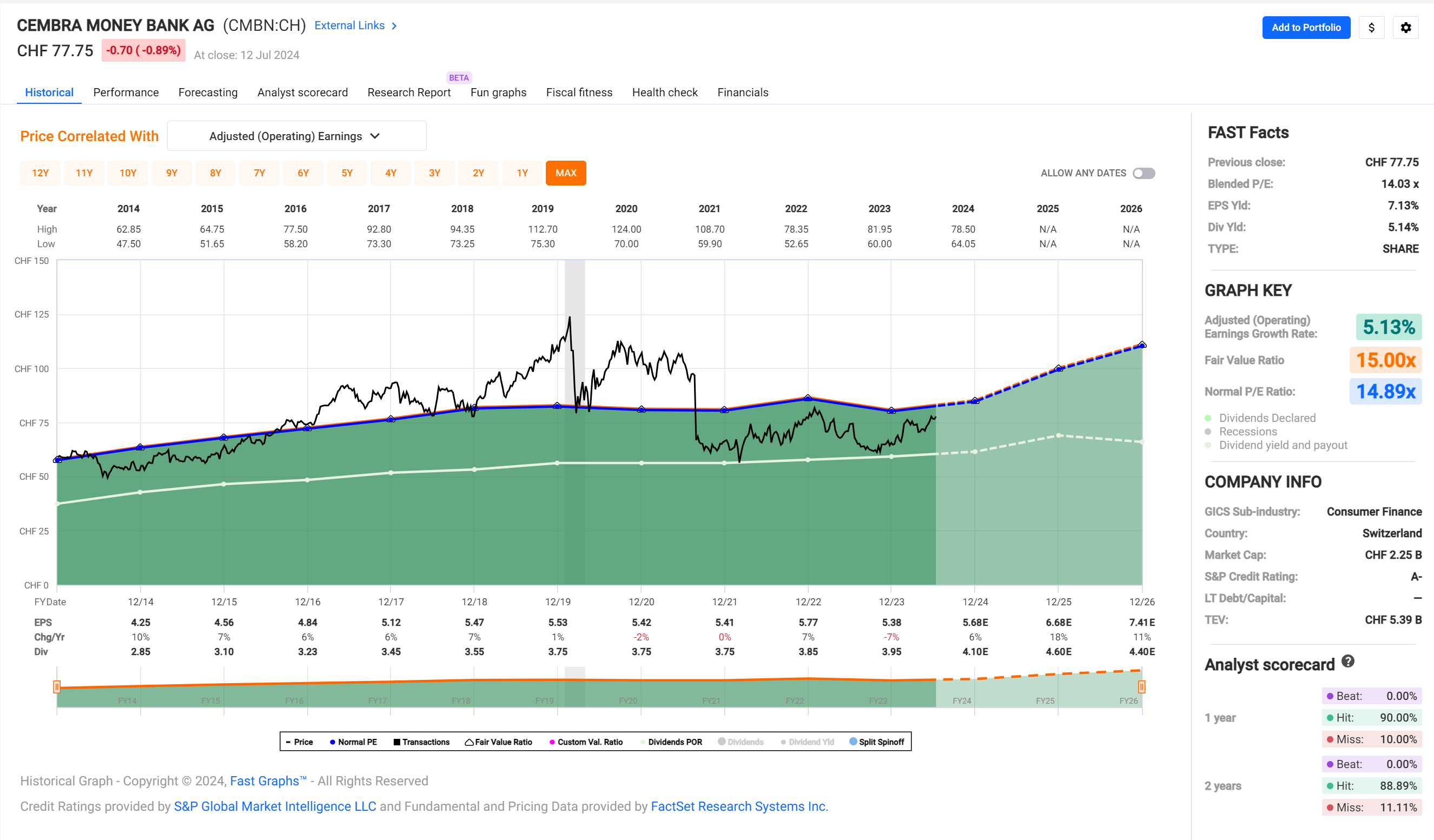

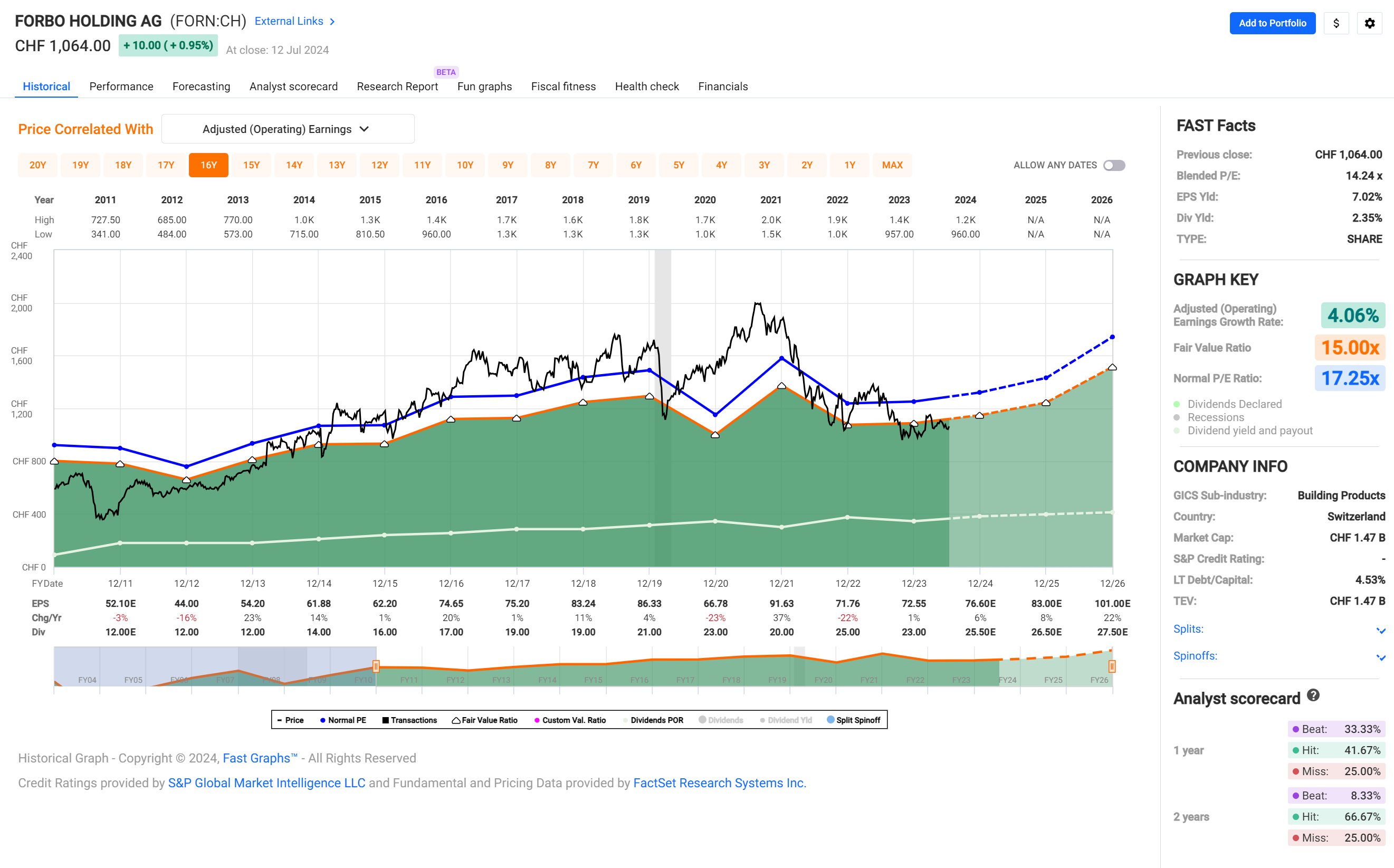

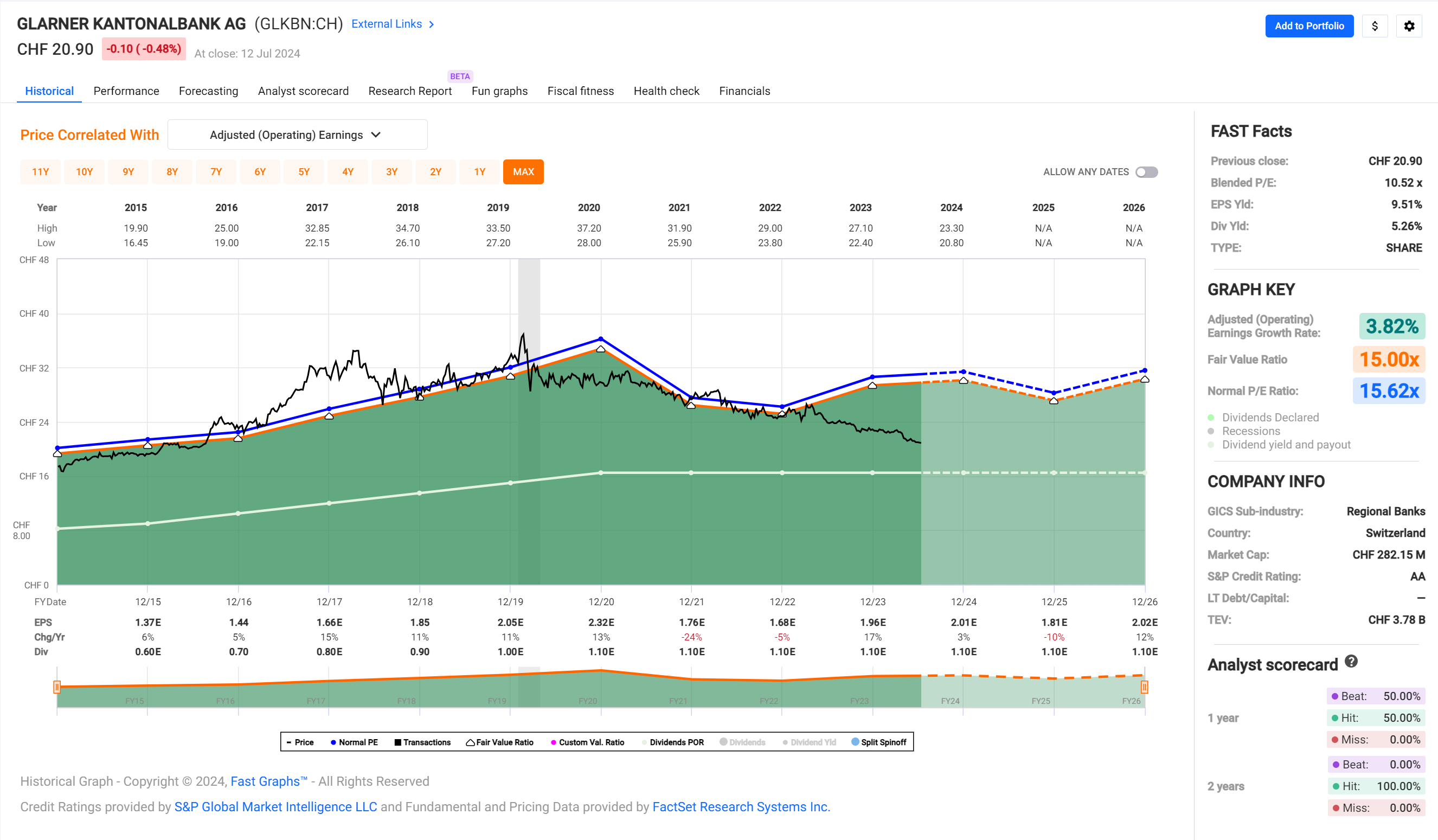

Contenders: Didn’t make the cut for various reasons.

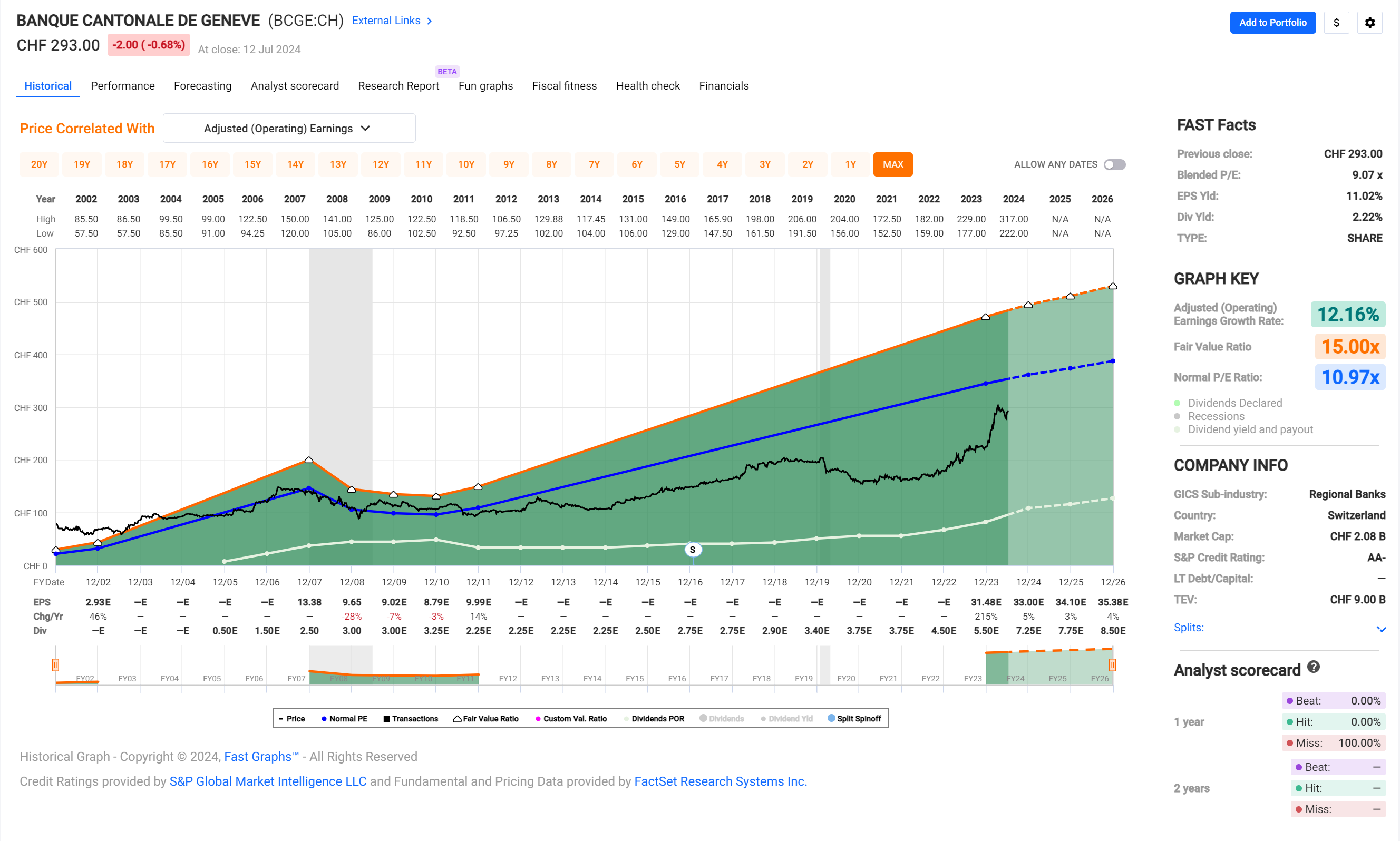

Banque Cantonale de Genève

Berner Kantonalbank

BKW

Cembra Money Bank

Forbo Holding

Glarner Kantonalbank

Holcim

Julius Baer

Meier Tobler

Mikron

Swiss RE

UBS

Vontobel

Zurich

Some final thoughts:

Don’t get me wrong, there are a bunch of great businesses in the SPI (Nestlé, Novartis, some of the ones listed above, etc), it’s just that many of them are (IMHO) overvalued.

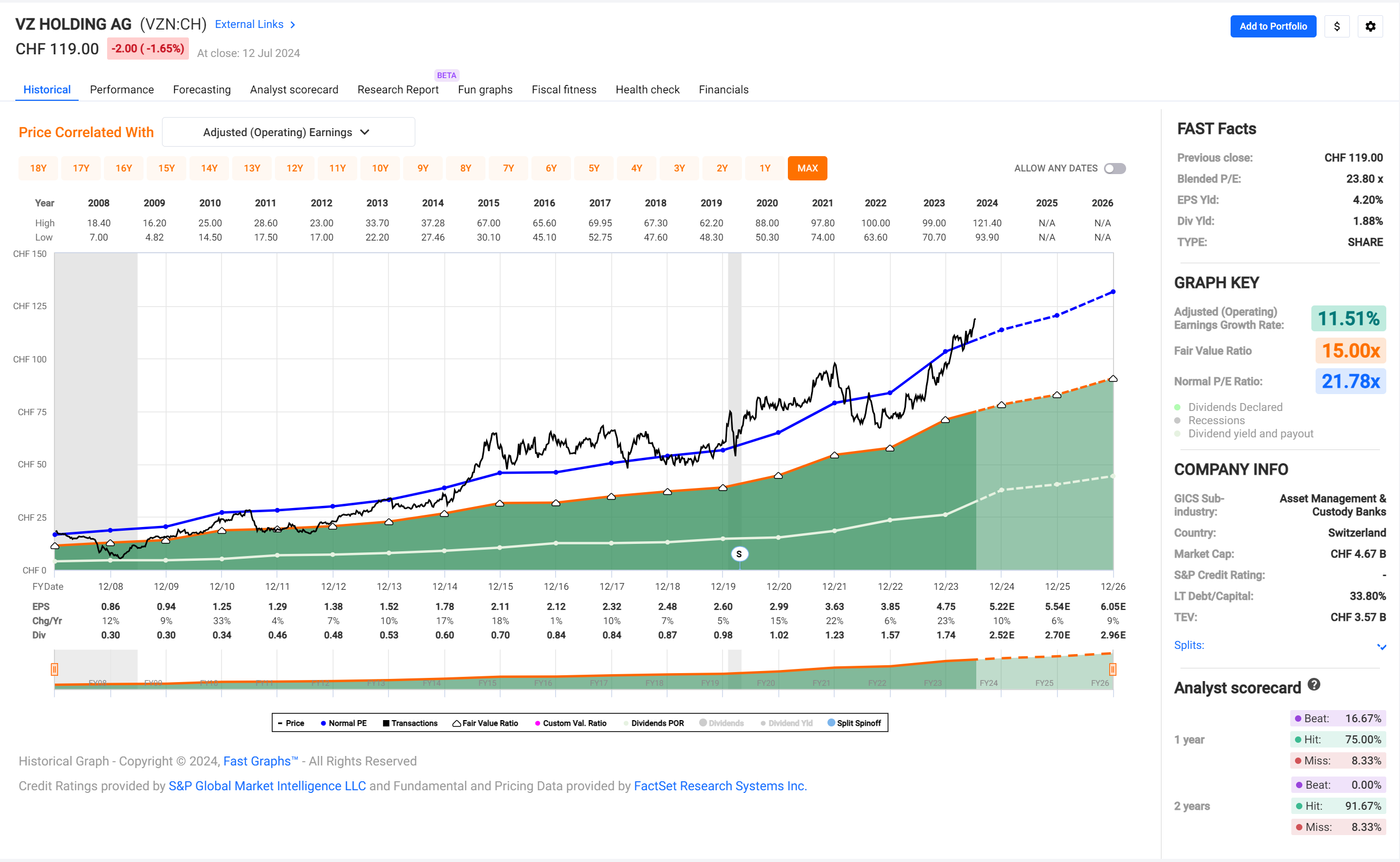

I’ll provide one perhaps less know example for a great company at the wrong price:

VZ Holding

* Earnings Yield: if you bought the entire company at its current price, your current yield in earnings would be 11% of the price paid.

** Analyst scorecard: lots of misses mean that analysts kept overestimating the company’s earnings.

Wow, your list of swiss companies is approximately the reverse of mine. The main reason is that I don’t buy banks or insurance companies

Not entirely sure which list you’re referring to?

My above-the-cut list (companies I would do further research on before buying) like Mobilezone, Roche, or Valiant?

Or my below-the-cut list (companies I would not buy but maybe keep on my watchlist)?

The entire SPI?

Sorry if I misunderstood.

Any reason for that choice?

Not questioning your choice, just trying to understand why you would shun these sectors/industries entirely.

Both your candidates and watchlist (except Roche) are not part of the 20 companies I find the best.

Banks can have big unexpected problems (look at Credit Suisse) that most other companies can’t have and that can litteraly kill the company. When for example Nestlé has some serious mortal bacteries in food on a large scale, even the specific brand doesn’t dissapear. Insurance is probably not as dangerous but can have similar problems too

I had Cembra and Holcim, but now sold.

I’m not making any recommendations, just sharing my observations.

You do with this whatever you like. Pick the top 20 you like best.

Be well and invest well!

@_MP : this looks like SPAM (or worse), I’m afraid, even if said member has been part of the forum for a while.

Reason: post is completely unrelated to forum topic and promotes stocks.

Please act as you see fit?

I retract, I still don’t get the RBKL reference, but maybe that’s just me.

Sorry about any noise?

How often do you reasses the stocks in the universe you monitor?

Basically you would need to check periodically all existing investments and the investable universe and adjust the portfolio. Isnt that a looooot of work?

What’s that anyway? Doesn’t exist as a stock ticker as far as I see.

I wonder where would ABB fit ![]()

Slightly tongue in cheek, and very much “I heard from a friend”, but last year I did hear from a friend who’s an engineer currently with Siemens and tried, unsuccessfully, to join ABB, that ABB is “going to the m00n”. It does seem to be going to the moon (language used is deliberate for effect!).

I’m pretty sure it wouldn’t make your cut @Your_Full_Name.

Well, Ok, seems Stockpickers with dyslexia should do extra due diligence!

Agree. The most recent post as well

Reassessing takes up relatively little time, at least the way I approach it.

In the first approximation* my universe is my existing stockpicking portfolio with about 100 companies.

(I only took a look at the SPI constituents as a fun exercise)

I tend to mostly buy and hold.

Reassessing is really only necessary when my basic assumptions about the company change.**

I hope to eventually reach zen status by looking at my holding only on a maybe quarterly basis or so?

Currently I typically review look at the holdings via FASTgraphs about every other week or so (mainly because I enjoy it). That takes maybe 10-15 minutes as you can see with a glance whether the main things I care about for the company are still intact.

* My tiny universe gets extended via suggestions I pick up from various places, but they rarely exceed one or two new companies a month (unless we have a crash or so).

** I’ve sold a little over 20 times in the past about 5 years for the following reasons: