Thanks for sharing your method and portfolio holdings.

I see that you have several holdings with a >50% loss after 2-4 years. Any reason you want do keep them ? believe in a rebound ?

Thanks for sharing your method and portfolio holdings.

I see that you have several holdings with a >50% loss after 2-4 years. Any reason you want do keep them ? believe in a rebound ?

Nostalgia?

Plus I enjoy other forum members sticking their well salted fingers into my bleeding wounds …

![]()

Slightly more seriously, thanks for setting the 50% threshold so I don’t have to explain some of my other positions deep in the red … ![]()

CMP (-55.1%): rationally, I should have sold it.

It remains there like a sore black eye in portfolio as a personal reminder to myself that Basic Materials is mostly not a sector for simple minded Goofy.

Luckily, it’s a tiny position.

PETS (-53.6%): rationally, I should have sold it.

Another sore black eye in portfolio as a personal reminder to myself that I should never blindly “copy buy”: one of my mentors – who I still consider an inspiration – bought this in the COVID recovery, I just did the same at the time without having built my own conviction.*

Luckily, it’s a tiny position.

VFC (-56.5%): I should have sold. I think they’ll recover; I should still exchange them for a more profitable company. I have no real excuse here.**

They’re just about fairly valued right now, but even with the expected returns going forward, it’ll take a few years … maybe I’ll sell on more “Fed rate cut” news bounces like last week.

Unfortunately, this one is an expensive lesson.

WBA (-57%): I probably should have sold at the time of the dividend cut, but I believe they’ll recover.

They’re IMO currently severly undervalued. Since I am somewhat cash flow oriented I’d also have a hard time replacing their current earnings yield of 26% and dividend yield of 8.7% with something comparable. Maybe I should part with those goals …

Expensive lesson as well. ![]()

* Of course said mentor sold the position when PETS cut their dividend and perhaps I should have just “copy sold”.

I’ve since however successfully eliminated “copy buying” and PETS reminds of this whenever I’m tempted.

** I enjoy seeing people almost every day wearing/owning expensive NorthFace stuff and I am almost sure my wife owns their entire icebreaker line garment, but VFC’s Supreme acquisition was plain stupid expensive. And I fell for it as my teenager at the time loved the Supreme brand (of course before it was acquired by VFC …).

- 3 times for tax reasons: the company is a limited partnership and a change in US taxation at the end of 2022 would have made it prohibitive to own these companies (BIP, EPD, MMP)

There are typically wrappers or alternative containers available e.g. BIPC, AMLP. I also liked a lot of the midstream partnerships and there are not so great options for holding indirectly and avoiding the partnership structures I found they were either not what I wanted or expensive or both. I settled on AMLP (expensive) and bought ones that were structured as companies.

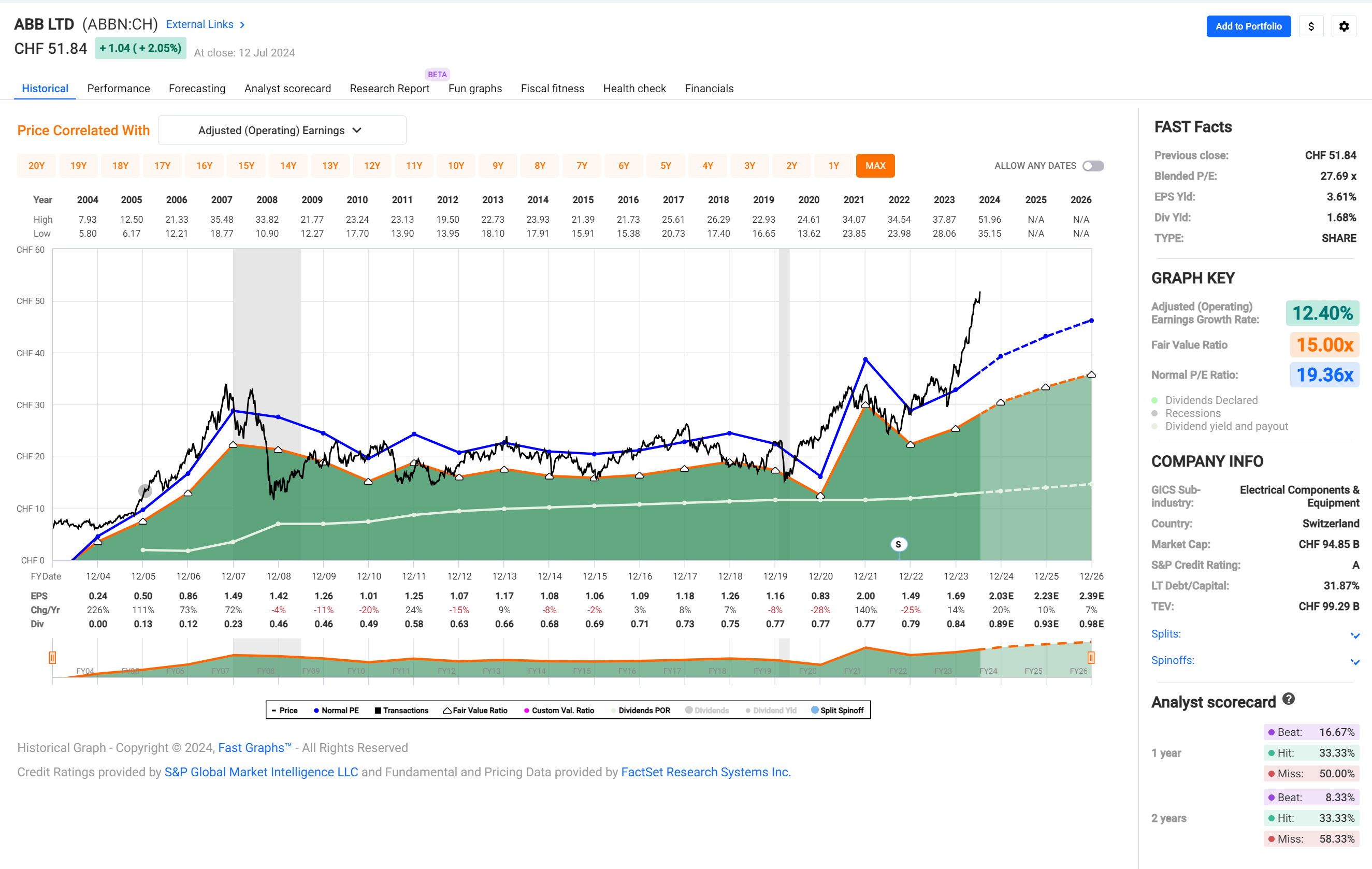

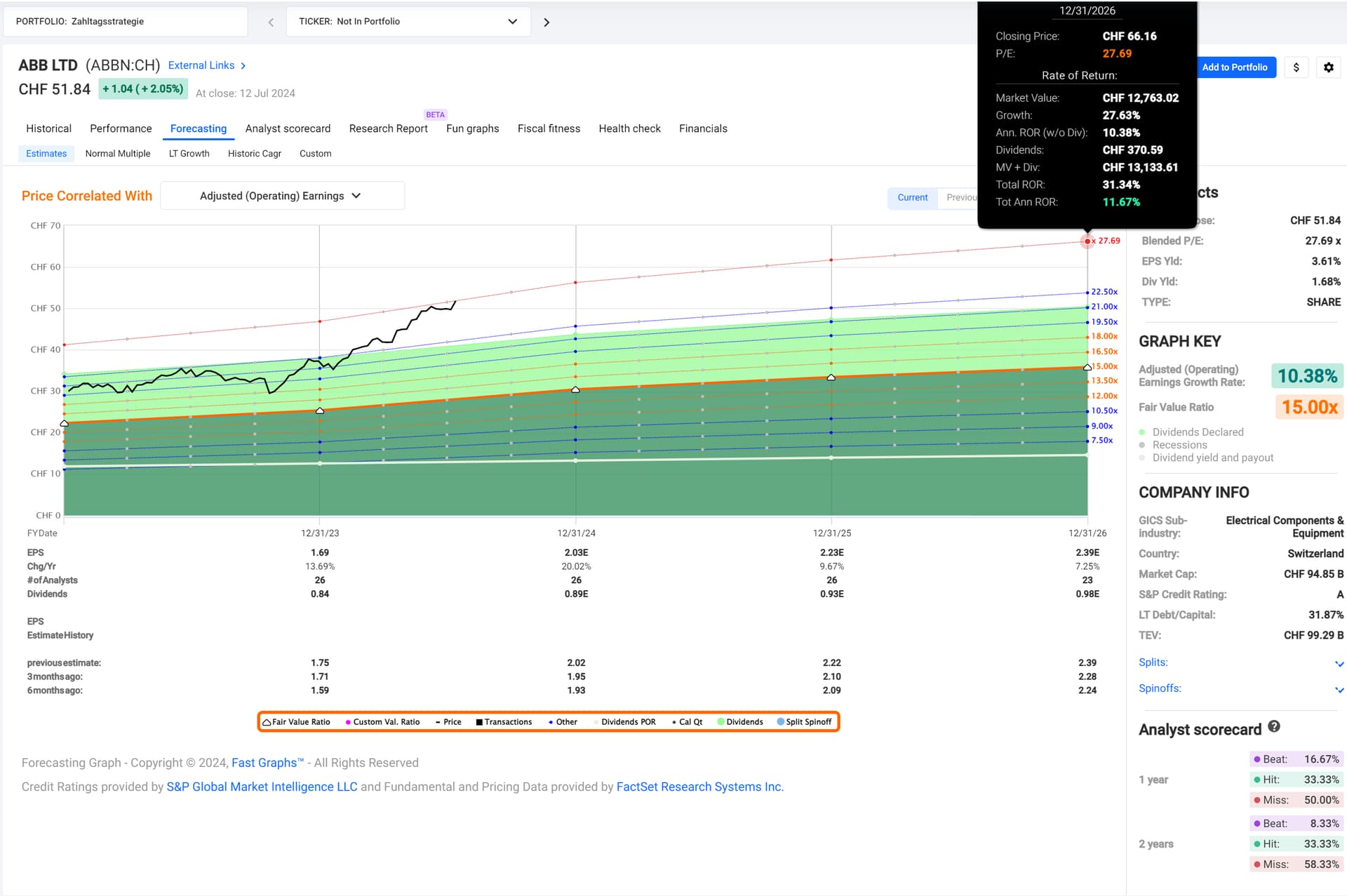

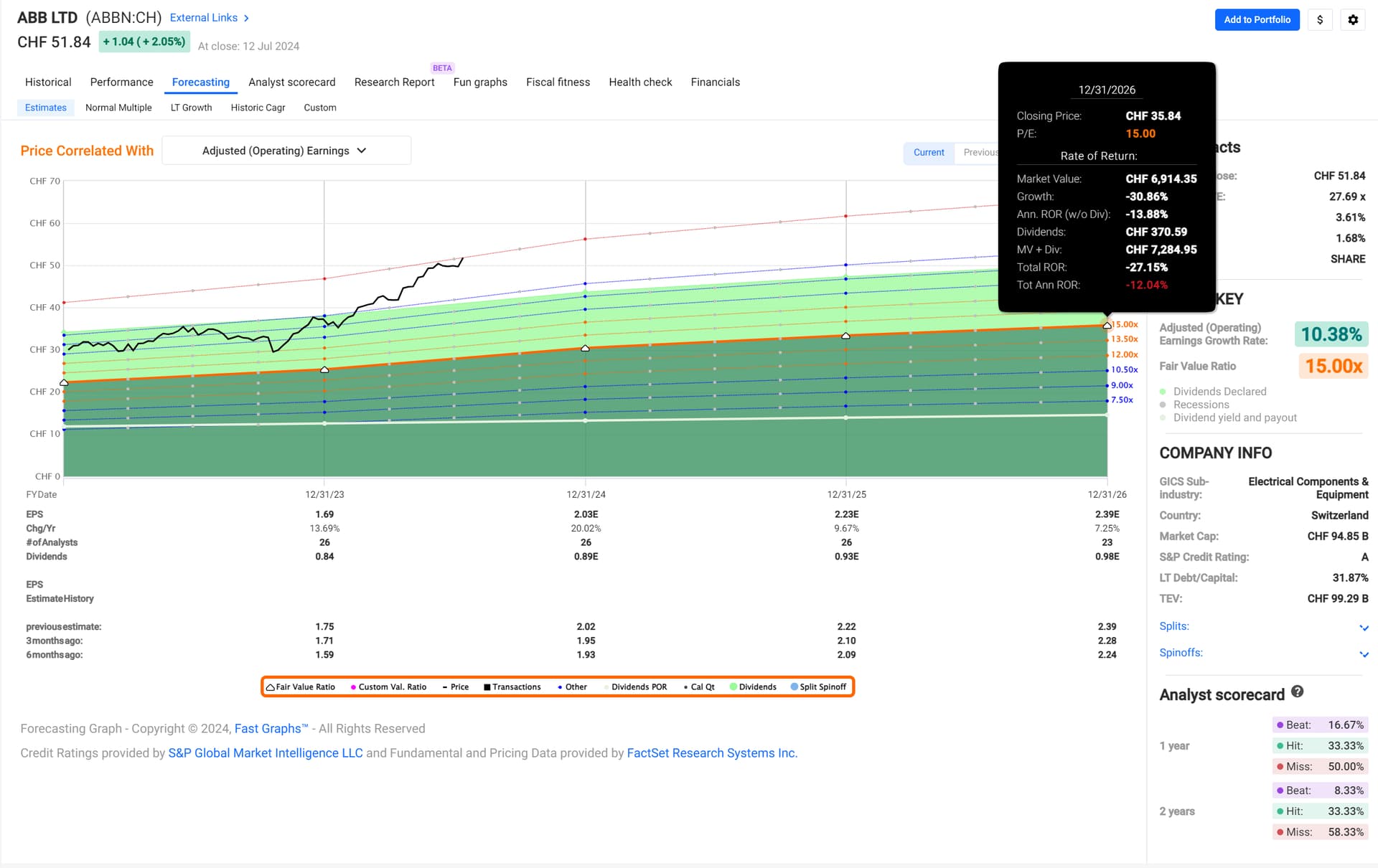

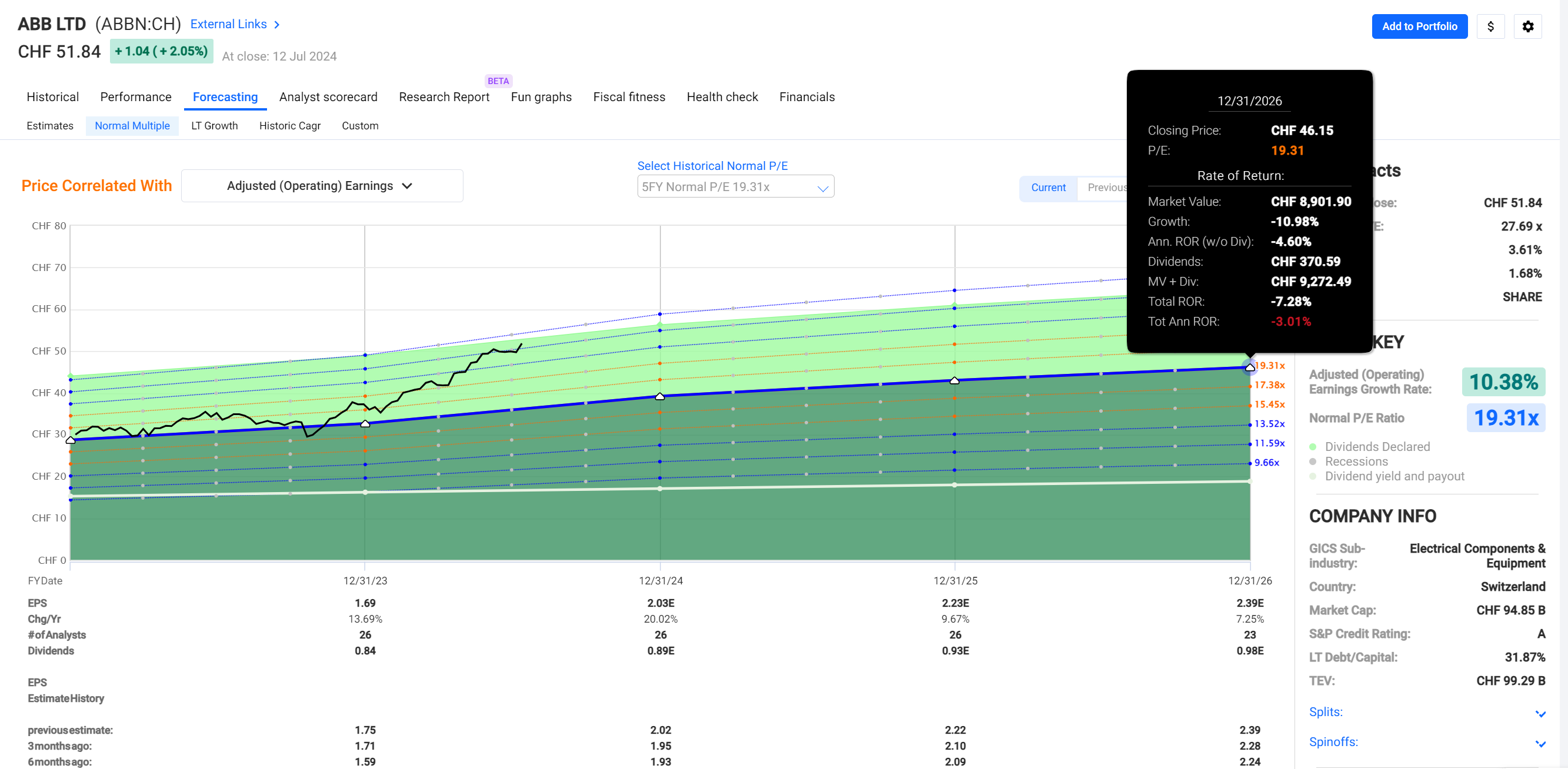

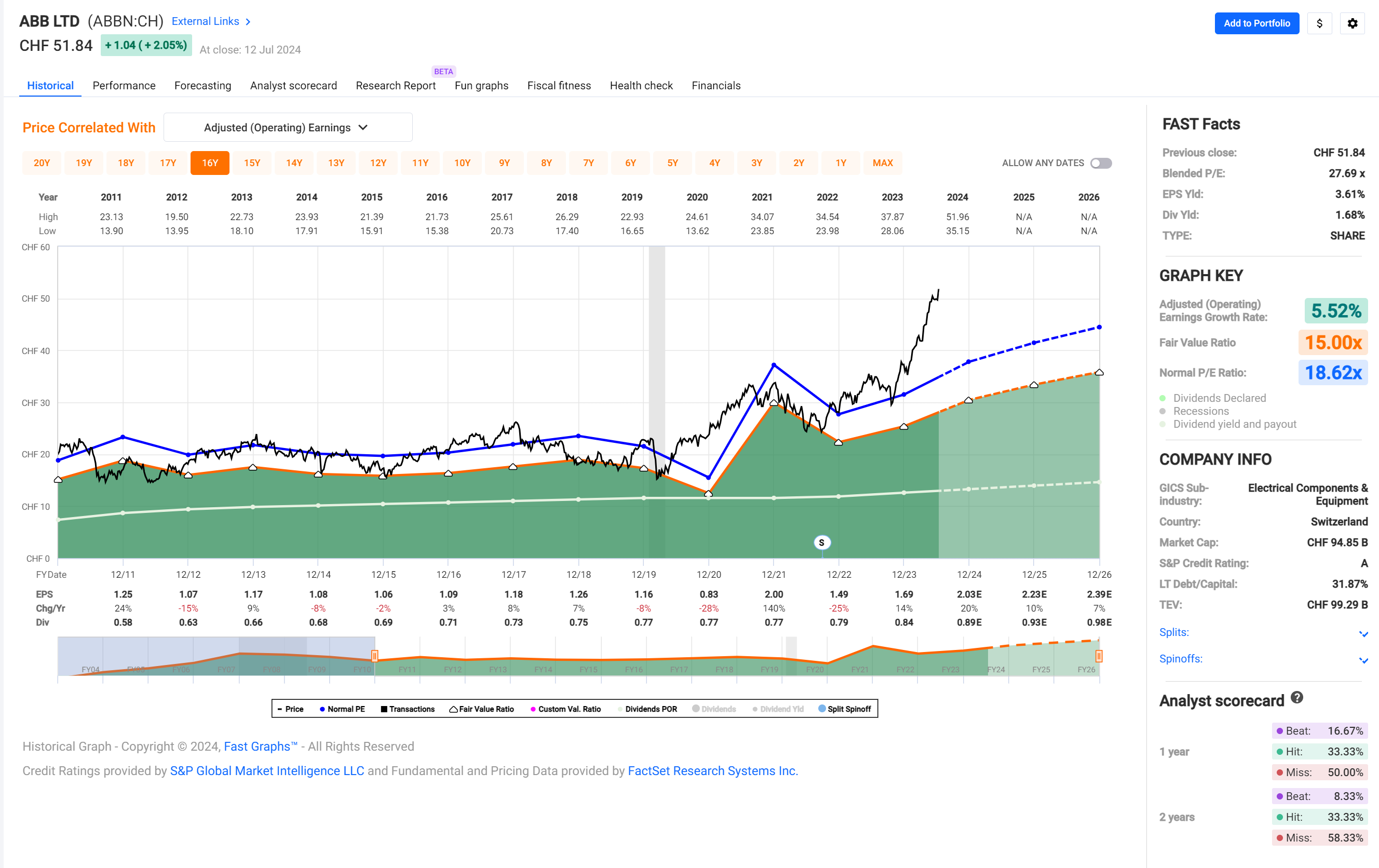

TL;DR: Goofy doesn’t like ABB’s current valuation

As they do it in school and in management, first some good things about ABB:

Now for some tougher discussions:

Valuation: “Price is what you pay. Value is what you get. – Warren Buffett”

Growth:

Final thoughts:

Can ABB go to the moon? Of course!

Can ABB return to their normal or even – given their growth – fair value? Absolutely.

The latter seems more probable to me, but in the end, only the future will determine the outcome.

Do I know anything about the future? No. That’s why it’s called the future. ![]()

* Only 5.5% if you go back to their last pre-Covid low in 2010:

Now I wish I’d held on to ABB!

So a question for the group

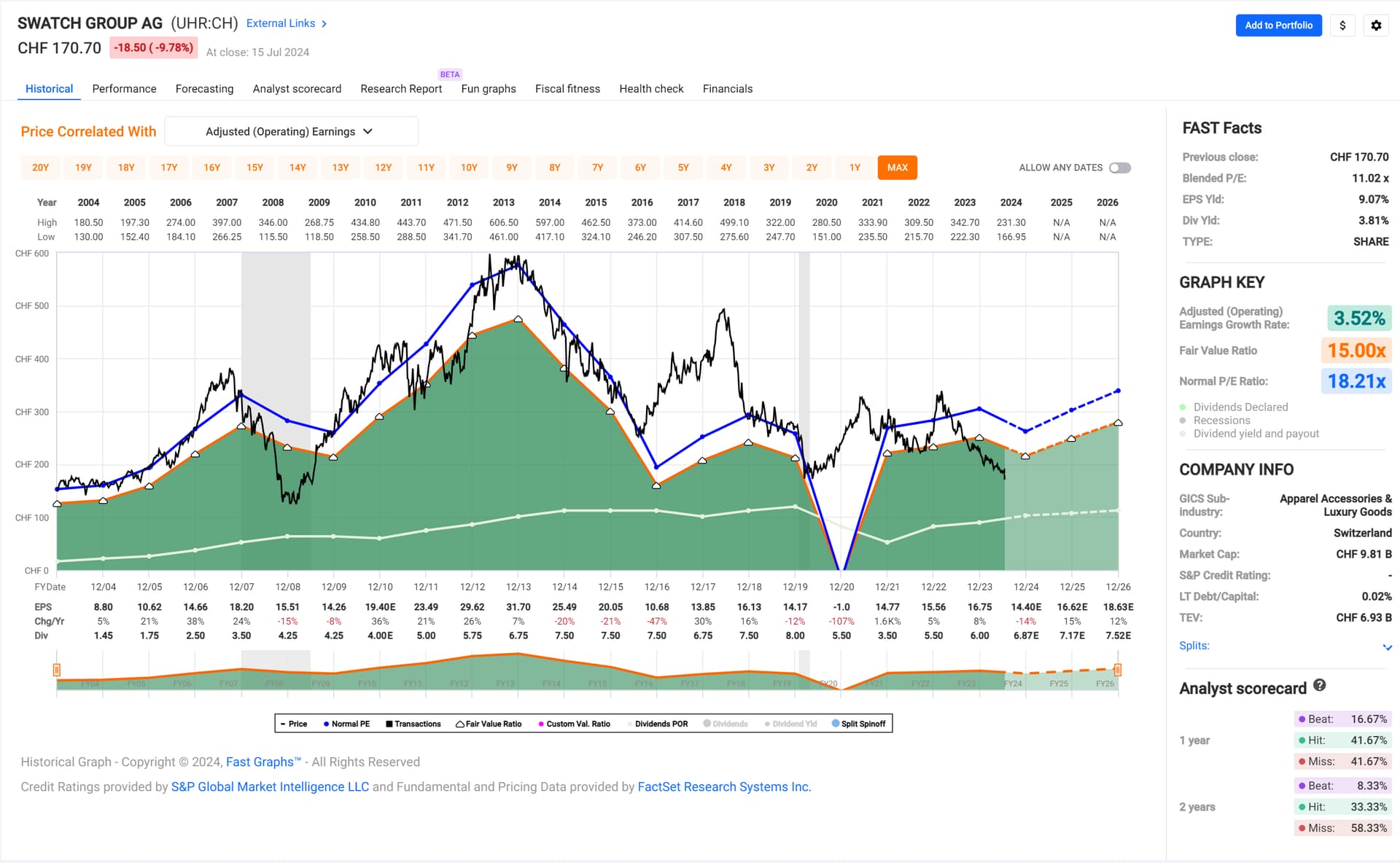

Swatch reported their earnings

Stock got hammered and now trading at market cap < 9 billion CHF

As per balance sheet , the assets are worth 14 billion. Retained earnings of 15 Billon, Equity 12 Billion. Even inventory itself is 7.7 Billion

How should I read this?

Market expect Swatch to sell products at discounts to be able to grow revenues ? Or they are grossly undervaluing this stock?Report

how much debt/liabilities do they have?

2 Billion liabilities

Maybe @Your_Full_Name has a FastGraphs on this. I have data only post-pandemic and would like to see pre-pandemic financials.

Indeed, Swatch has a book value of CHF 12.2b as of December 2023, and only a market capitalisation of 8.9 billion.

A market capitalisation lower than the book value of the business is usually a sign that the company is not earning its cost of capital. Here Swatch posted a CHF 147 million net income for H1, or roughly 294 million annualized. That’s a 2.4% return on equity, which is very insufficient for the risk taken.

Here shareholders are saying that they could get the same profits with less capital invested, and thus they value the capital of Swatch less than what is stated on the book.

Yeah, came across Swatch when skimming through the SPI …

I like that they have no debt, but even if they currently look undervalued, owning the company is not tempting to me. Too cyclical for Goofy.

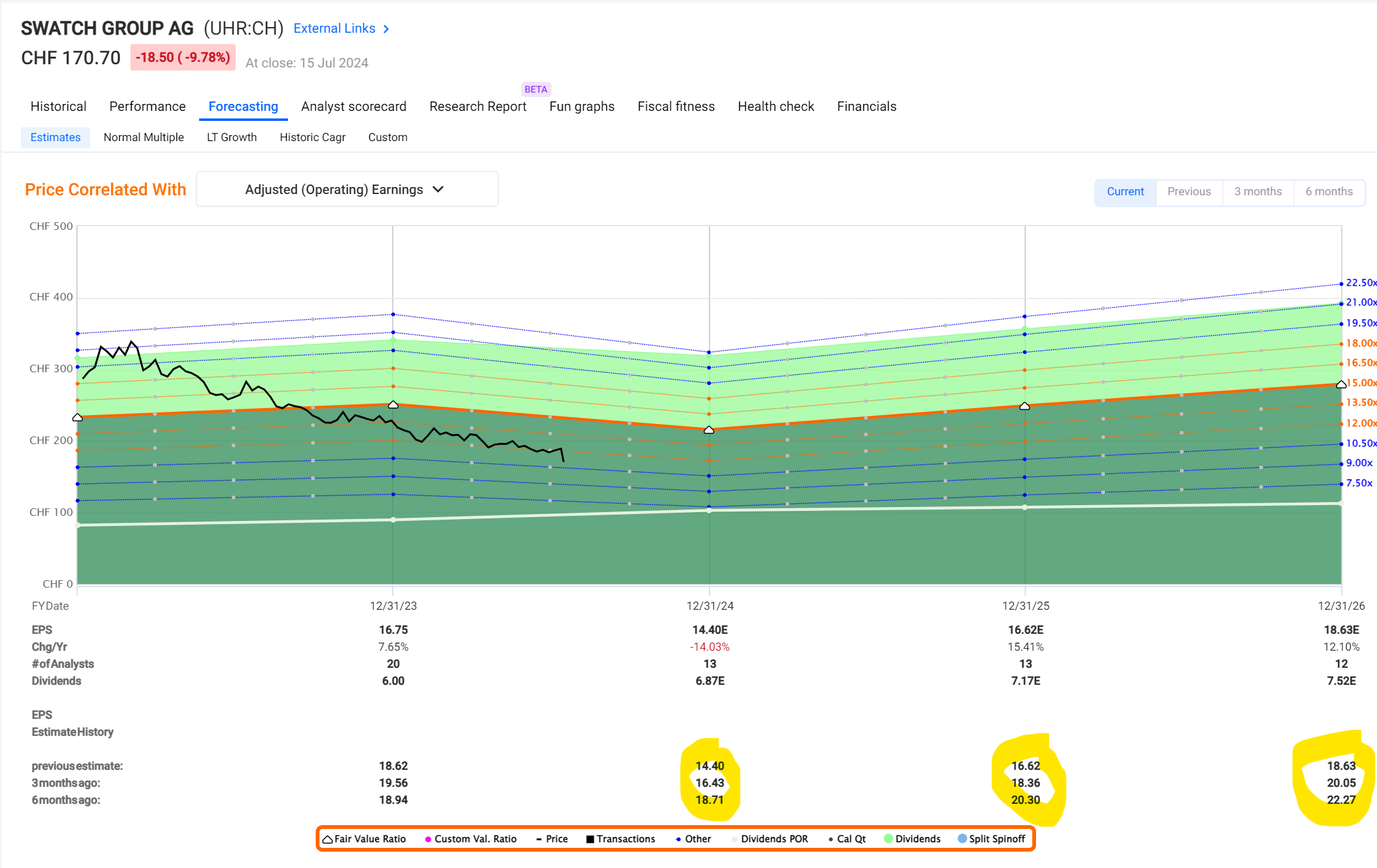

Looking into the future, their earnings estimates for this year, 2025 and 2026 have been steadily going down

and the analysts in the past still often overestimated Swatch’s earnings:

I also don’t really like their CEO Nick Hayek – whenever he appears in the press, he behaves like a patron and seems to forget that that Swatch is a public company, not his own.

And Swatch’s 6 member board of directors has three Hayek family members …

| Previous | Nov.01.2023 | Feb 2024 | Jul 2024 |

|---|---|---|---|

| Bonds | Bonds | BTI | BOXX |

| BTI | Short SPY | Bonds | BTI |

| VIRT | BTI | AWE.L | Bonds |

| MMM | VIRT | MPW | MPW |

| MPW | MMM | MMM | GLD |

| KAP.IL | KAP.IL | VDY.TO | AWE.L |

| AWE.L | O | ENB | VDY.TO |

| LNC | MPW | URNM | AMLP |

| VDY.TO | MO | AMLP | URNM |

| AMLP | AWE.L | WDS.L | VICI |

Sold some more today. Now up to 70/30 stocks/bonds.

Remind us again how we need to play this table … 4 in a row by first letter, horizontally, vertically or diagonally is a win? Shorter continuous streaks reward fewer points?

More seriously: Assuming it’s top positions by column?

Sorry, mate, I am really a little confused. ![]()

(and anticipatory apologies if you’ve explained this before ![]() )

)

It’s the top 10 holdings.

who’s buying CRWD today? ![]()

Anyone who has first really checked that CRWD’s insurance coverage will really cover today’s SNAFU. Frankly with all the liabilities and legal costs incoming I would not rush into this…

Today may potentially not only kill that player but as well a bunch of cloud / IT Services players. To be honest - I would not trade tech shares for at least a month, until the dust has settled. No need to sell, but clearly don‘t buy. This, in combination with the big rotation, may be the top of the ‚24 tech bubbley not worried about non-tech shares, but Nasdaq is probably a tough hold these days.

The more i think about it, the most obvious it is that the number of failures that needed ot happen for such a bug to be released in public is astonishing:

If you’re a software developer, that’s kind of a “The king is naked” moment. For a company with such a mission critical task that is cybersecurity, this betrays a lack of elementary development best practices that makes the stock absolutely uninvestable for me.

It’s way worse than what happened at Boeing : that would be as if Boeing delivered an airplane without even checking that the plane is able to fly…

The fish stinks from the head as the saying in German goes (not that this is the sole explanation).

CrowdStrike’s CEO had a similar shining moment at McAfee in 2010 when a security update there took down tens of thousands of machines across the Internet. One would think there was a lesson learnt then, but … well.

And of course all your points finding this astonishing are valid, but they all pile up on the cost side of things, don’t they?

Especially without those costs, the heavy currents of profit and stock price windfall are very powerful, statistically speaking. “Mostly, things turn out fine and my compensation covers some shortcuts here and there.”

I like your analogy to Boeing. Fewer people die right away because of mistakes made, but holistically, a lot more people seem to be put at risk because of CrowdStrike’s practices.

For those of you looking for an entry point: Goofy would advise to, ahem, be patient.

Be well and invest well!