Former colleague who knows basically nothing about finance and investments just joined, they asked me if they should get stock as they get it on discount. I said “depends on the discount”. They didn’t know yet and I have no feel for the discount rate. Looking at this graph I’m in mind to say “if you can get it below $150 go for it”, any views?

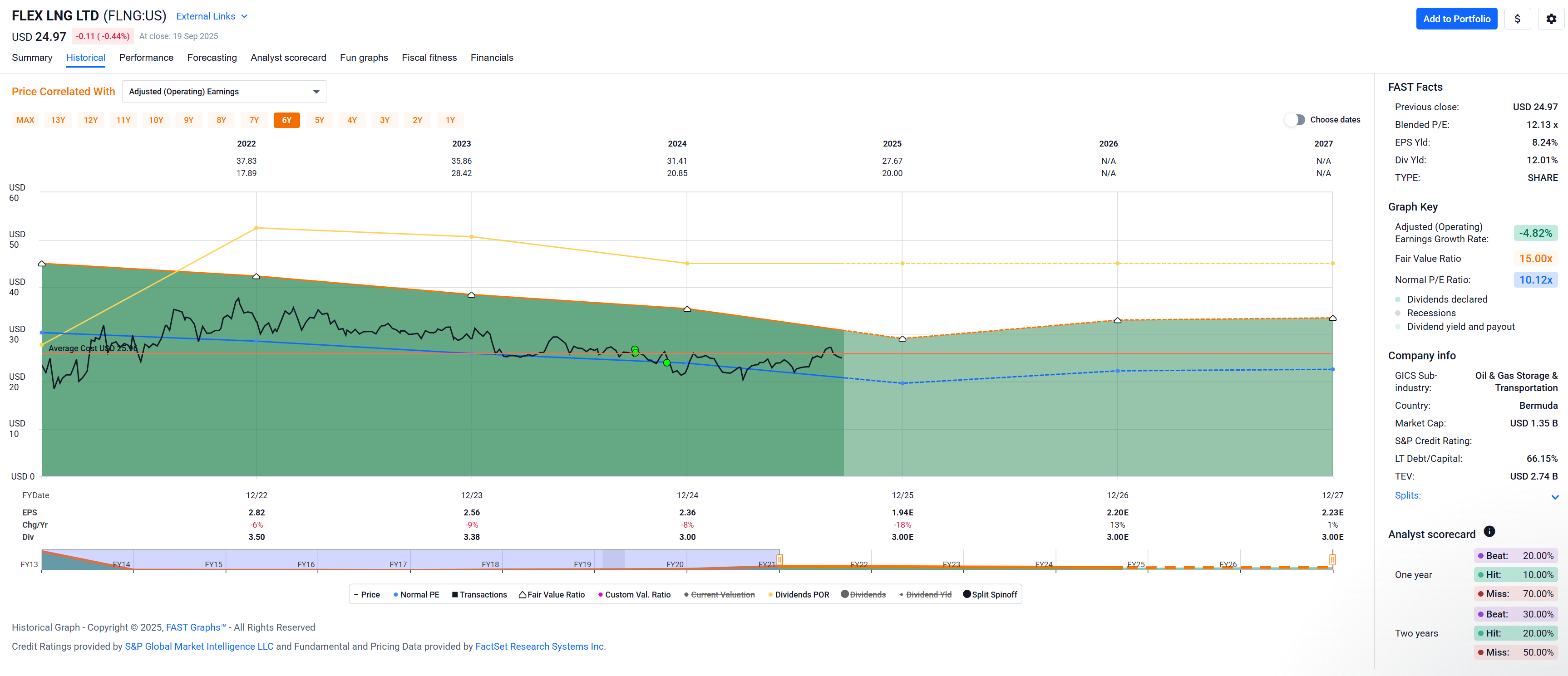

Another one that gives me pause is FLNG. It’s not your typical Goofy stock pick …

In fact, it looks like a sinking ship value trap with its 11.56% yield, 66% debt and sinking earnings since 2021.

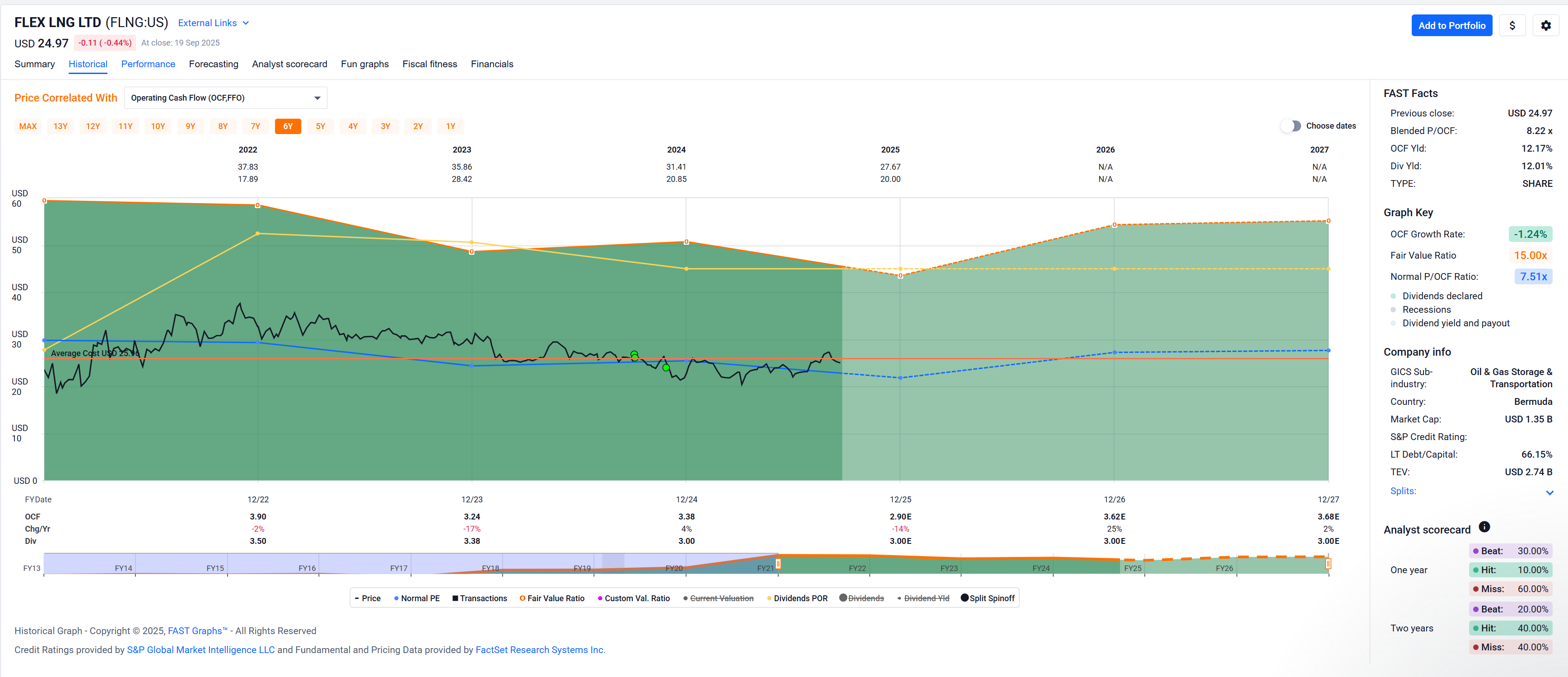

Since it’s a capital intensive business looking at Operating Cash Flow might be better to value the business, but the OCF FASTgraph doesn’t look much better.

Why am I invested and still interested?

- well, there’s that juicy yield … they could lower their dividend 10% or 20% or 30% – heck! 50% – and it would still be an attractive yield.[$]

This is really only an income vehicle, not a dividend growth stock that I usually prefer. - they have a modern fleet of 13 Liquefied Natural Gas Carriers (LNGCs) and my

macro theorybest guess is that Natural Gas consumption will increase with e.g. Europe buying from the US or so. - they have 55 years of minimum charter backlog (84 years with charterer’s options)

- no debt maturities prior 2029 and capex liabilities are limited to drydock of the fleet

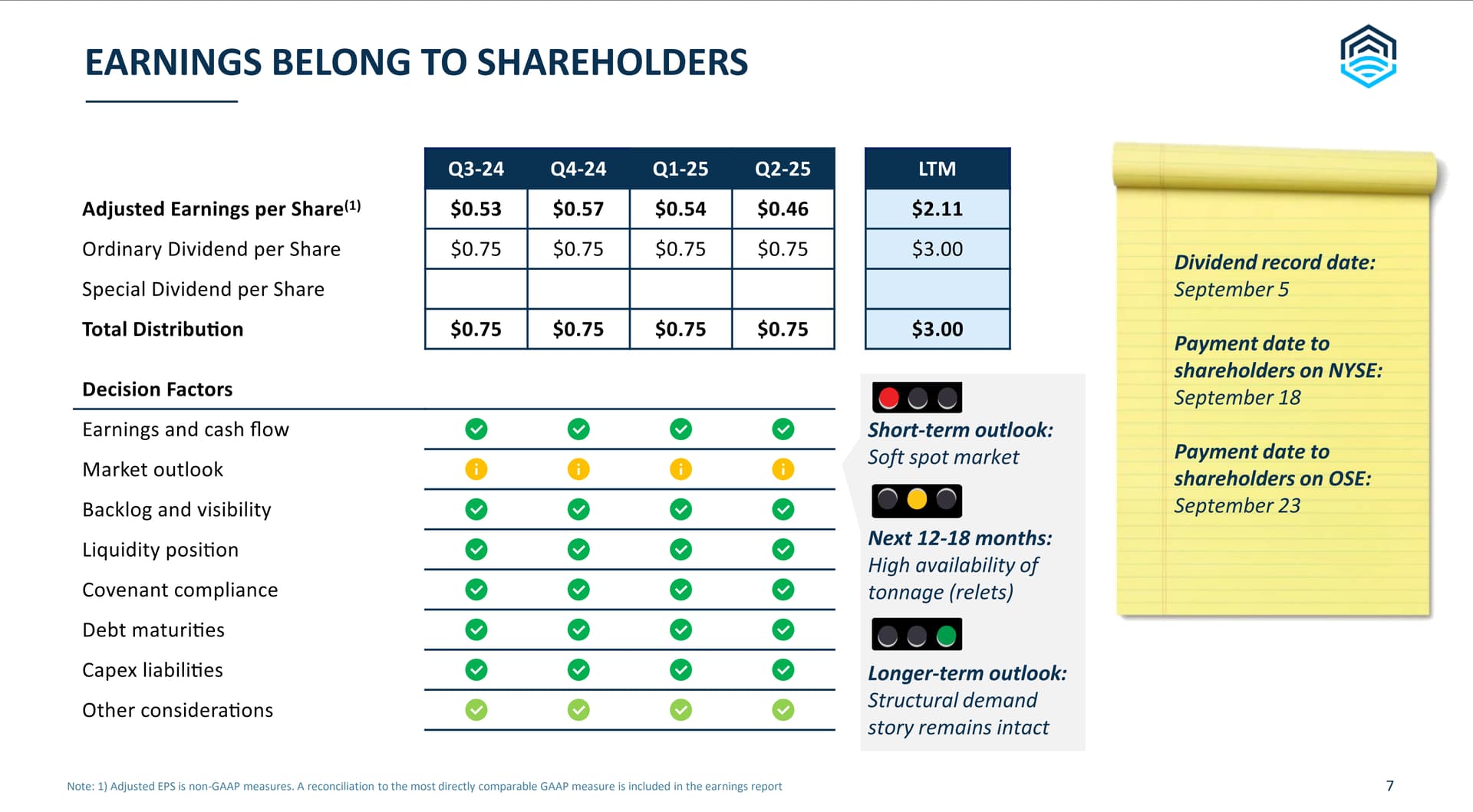

- they state that their earnings belong to the shareholder (how quaint a thought in today’s markets …)

- they’re small cap and afaik only in the Russell 2000 (hence I’m not competing with the big boys on Wall Street in trading this issue)

$ Of course they claim that their strong financial position and the contract backlog supports the dividend.

1 Like

Always hard to advise other people on investing, at least for me, as their goals, risk tolerance, time horizon, etc differ from mine. With that out of the way:

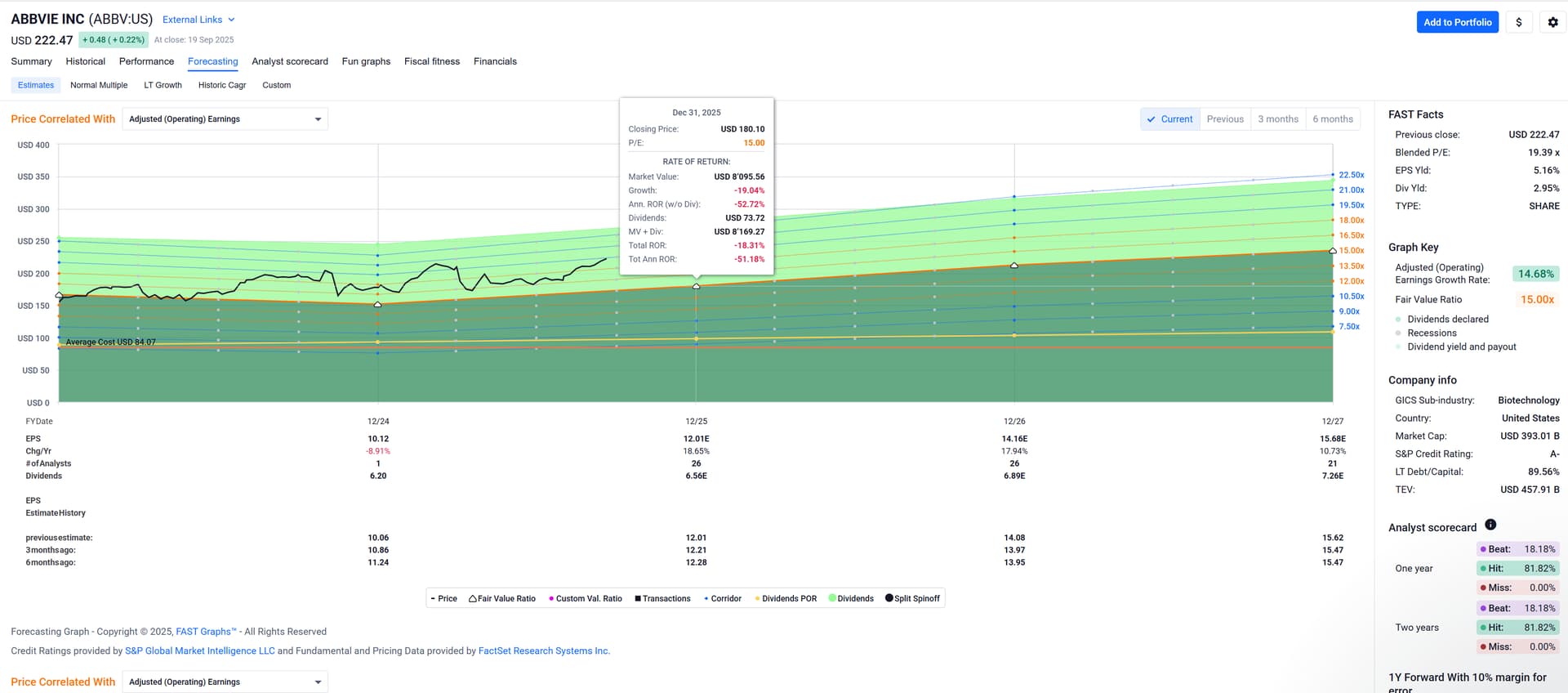

ABBV

- fair value is about $173 at the moment ($180 at year end) with regard to “fair” being a 15 multiple given the company’s earnings growth

I’d prefer to buy with a margin of safety, so below the fair multiple of 15, but then again Goofy’s a chicken.

If you’re going to hold for, say, 10 years, buying at the fair multiple now (without a margin of safey) won’t matter that much in 10 years. - the normal multiple for this company has historically been lower than the fair multiple for this company (the blue line in your graph) and only in the last couple of years has the stock price been above the fair multiple.

I believe that’s heavily influenced by that Humira patent cliff we discussed last week or so, so maybe that’s a one-off that dominated the normal multiple but it’s not the normal normal multiple.

Nobody knows with these biotech companies …

Certainly “if you can get it below $150 go for it” makes sense. I would add at $150 if I didn’t have a full position already. It’s even below the normal multiple of $160 that would apply at the end of 2025 based on current earnings estimates.

1 Like

Thank you, I thought my eyeballing of the chart wouldn’t be far off.

Overall they came to me for general investment advice because they don’t know anyone else “investing”, to which I said “we need to book some proper time, stay the hell away from banks and insurance companies until we talk” - I know insurance and banks are like vultures and will spot someone joining a big multinational firm, after which they’ll start circling them with “offers”. I’ll give the overall spiel of “low cost, broadly diversified index funds”, “time in the market beating timing the market” etc and they can take it from there.

1 Like

Isn’t it Signa Holding that you’re mixing this up with , solid RE sector investment?

![]() Mechanise your strategy before it’s too late!!

Mechanise your strategy before it’s too late!!

1 Like

Sorry, that’s private equity. We don’t mark that to the market until we have to.

Oh, wait …

It’s softly mechanised, rubber band and duct tape holding together a Tinguely-like machine, occasionally emitting a white puff as a buy signal and occasionally some grease burning with black smoke as a sell signal.

![]()

4 Likes

Position trimming continues as I try to convert stocks to cash for my pension purchase.

Today, I sold just under half of my BTU position. Funny how this ‘obsolete’ industry doubled my money in less than a year.

3 Likes

I remember posting about it on here when the price was $10 and wondering “why am I not buying this hand over fist?”

Although it is where it was a year ago, the big money was to be made pre- and post- covid. it is a 10x from 2020/2021.

Dear Stockpickers out there!

Let’s suppose I’m tired of my gambling with options and I want to put the corresponding $60,000 in one large US stock that pays little to no dividends and will hold relatively well when the tech/AI bubble finally pops. A stock I don’t have to monitor constantly because I intend to hold it forever and that is not crazily overvalued today.

Which stock would you buy right now?

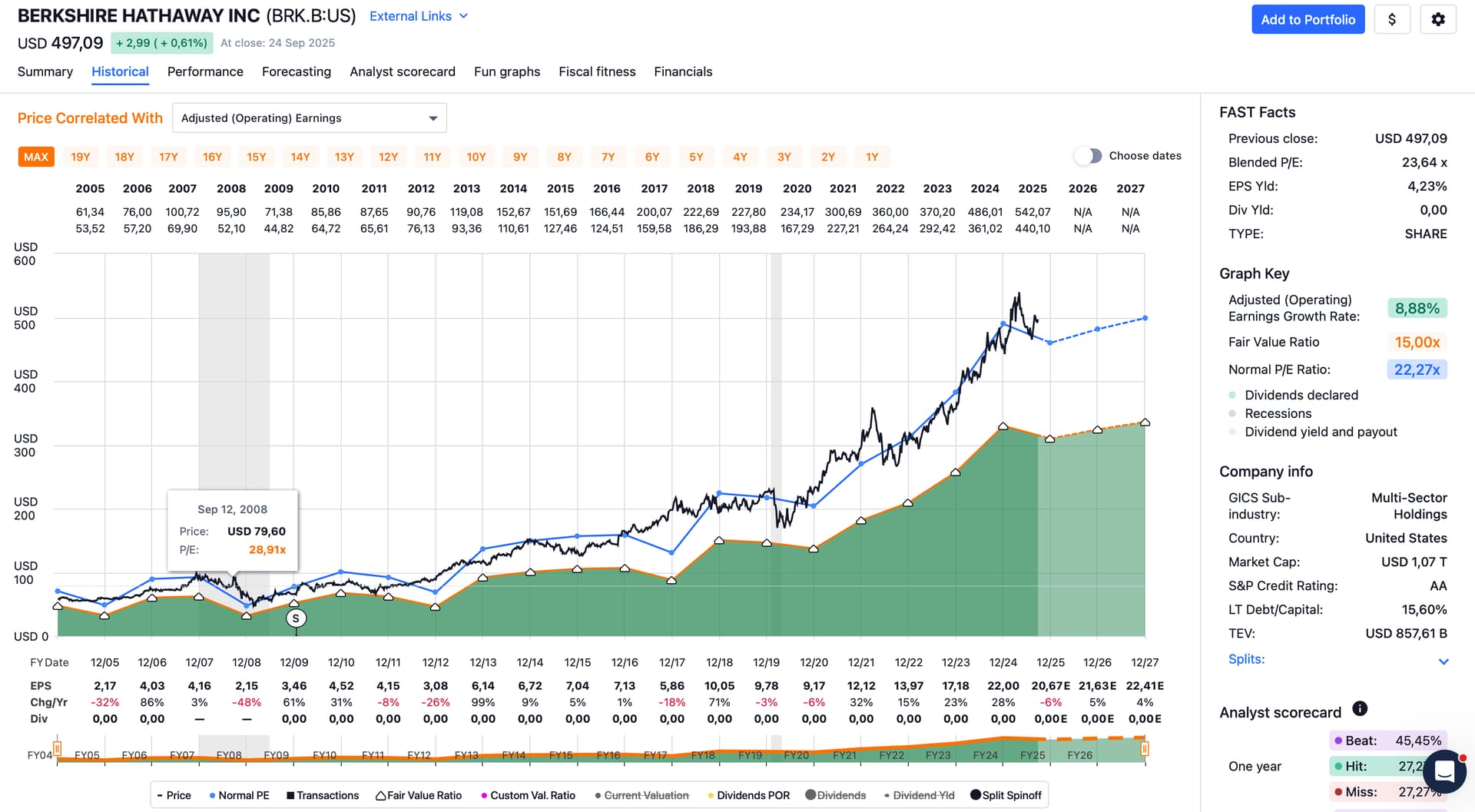

Spoiler: ChatGPT suggested GOOG or BRK.B

Thanks for your suggestions!

Larix

If there are any “lifetime” bets - mine is with BRK.B.

(But I’m definitely not worthy of a “stockpicker” moniker)

3 Likes

Depends on lifetime of who…

I would at least do minimal yearly checks. Even the oldest company (I think some construction company in Japan) went bankrupt after hundreds of years. Times-they-are-a-changing. Change is the only permanent thing!

I like to hold for very long periods, decades. But when the risks rise I sell, even if my heart bleeds. Motto: hold as long as possible… but not longer.

2 Likes

I’d go with BRK. Though when the AI bubble pops, I think everything will go down.

1 Like

BRK.B is my own lifetime pick, too. If I’d pick a handful of US stocks it’d be J&J + MSFT (both are the only US companies with AAA credit rating), and BRK.B, but you don’t want divvies so maybe BRK.B?

1 Like

I wouldn’t lump sum (but we’ve discussed this elsewhere on this forum) just for psychological reasons. Same for distributing $60k into several companies instead of just one.

Can’t really help with the “little to no dividends” requirement as I am on the opposite end of the spectrum, but gun to my head:

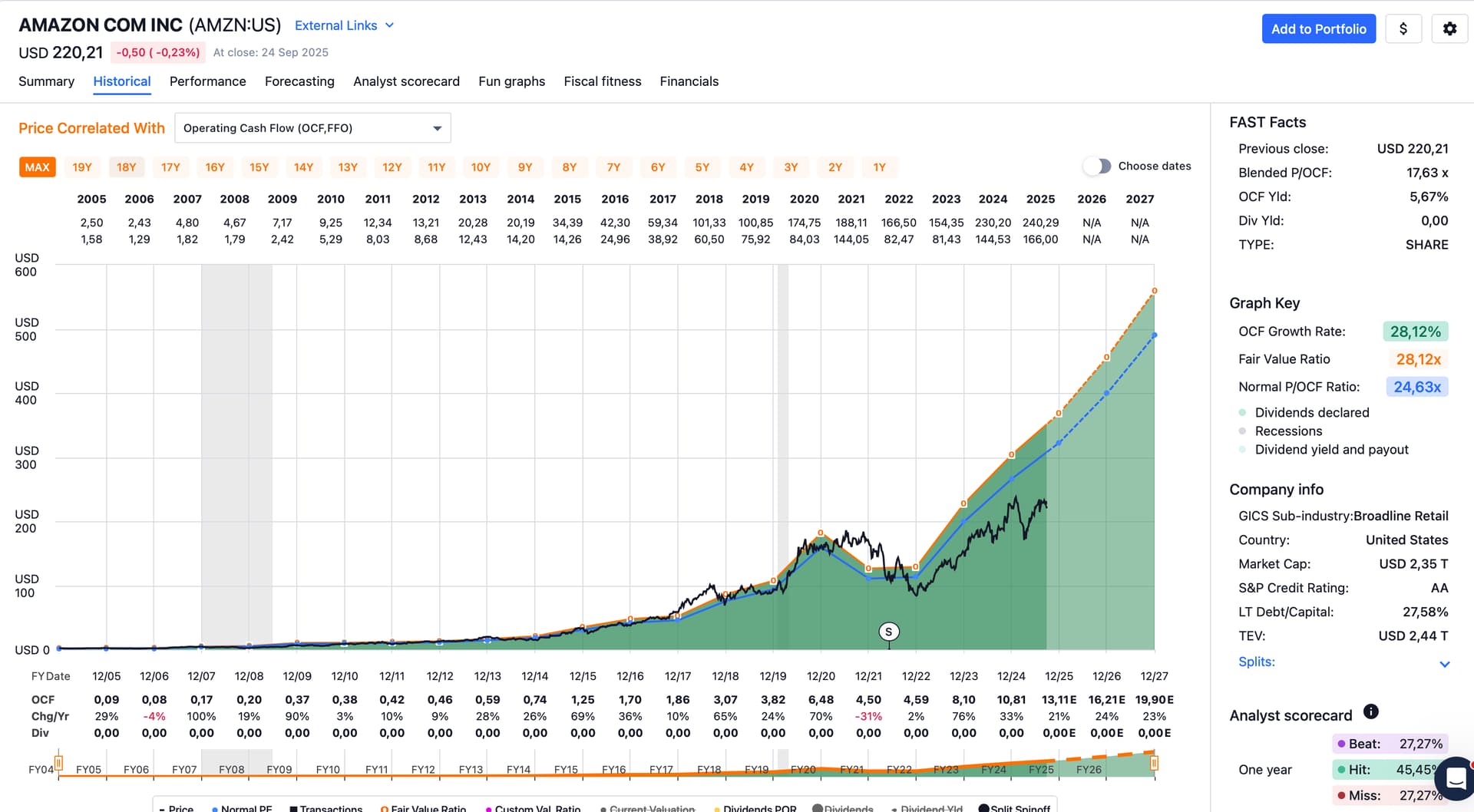

- AMZN: from my “junior portfolio” (which I manage for my son who is also not interested in dividends). Some correlation to AI through their cloud business where customers want Nvidia and its ecosystem (see also GOOG).[$]

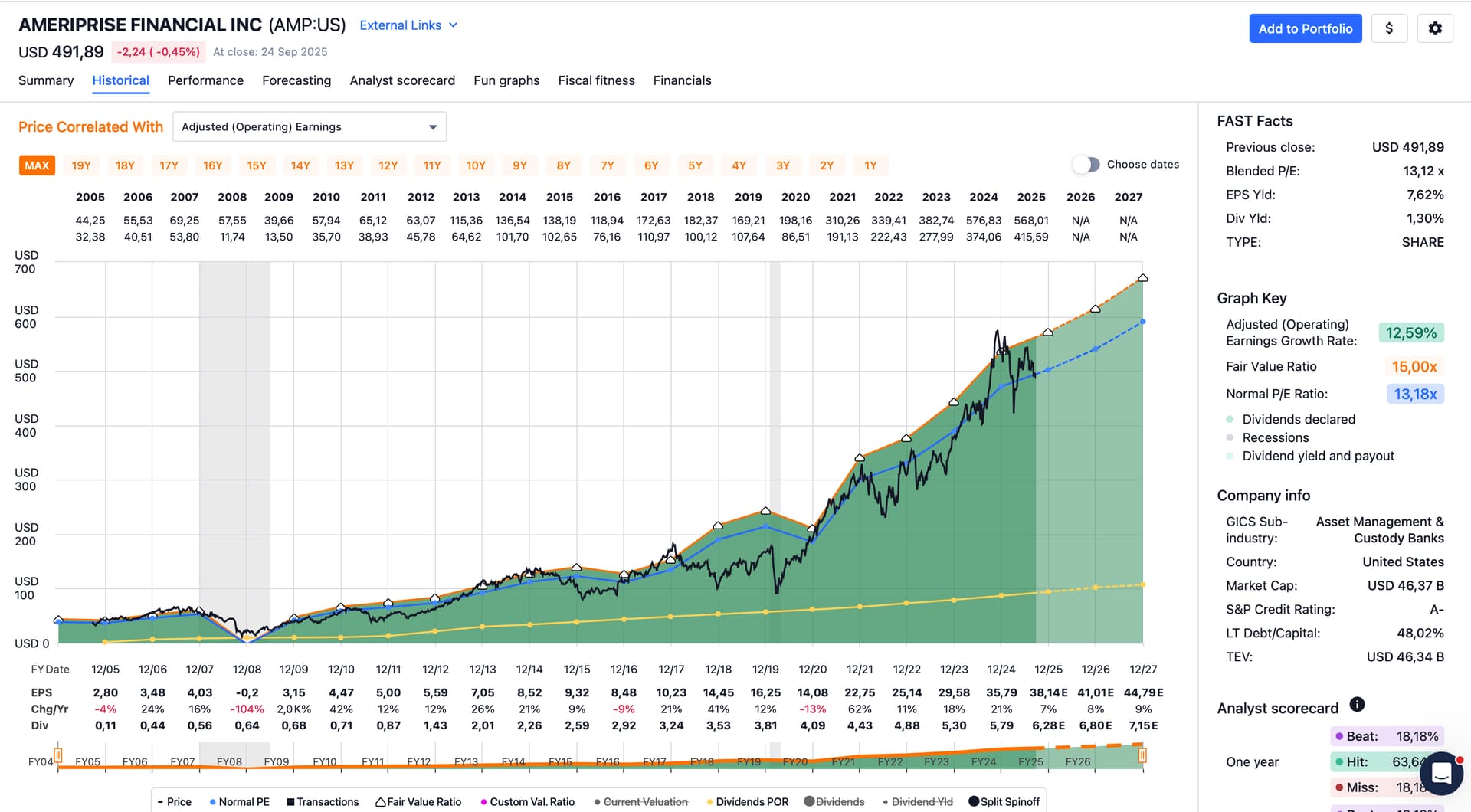

- AMP: from my “junior portfolio” (which I manage for my son). Probably almost no correlation to AI.[$$]

- BRK.B: probably fine, a tad overvalued even compared to its normal valuation (but isn’t it almost always?). Probably almost no correlation to AI.[$$$]

- CI: see my post above

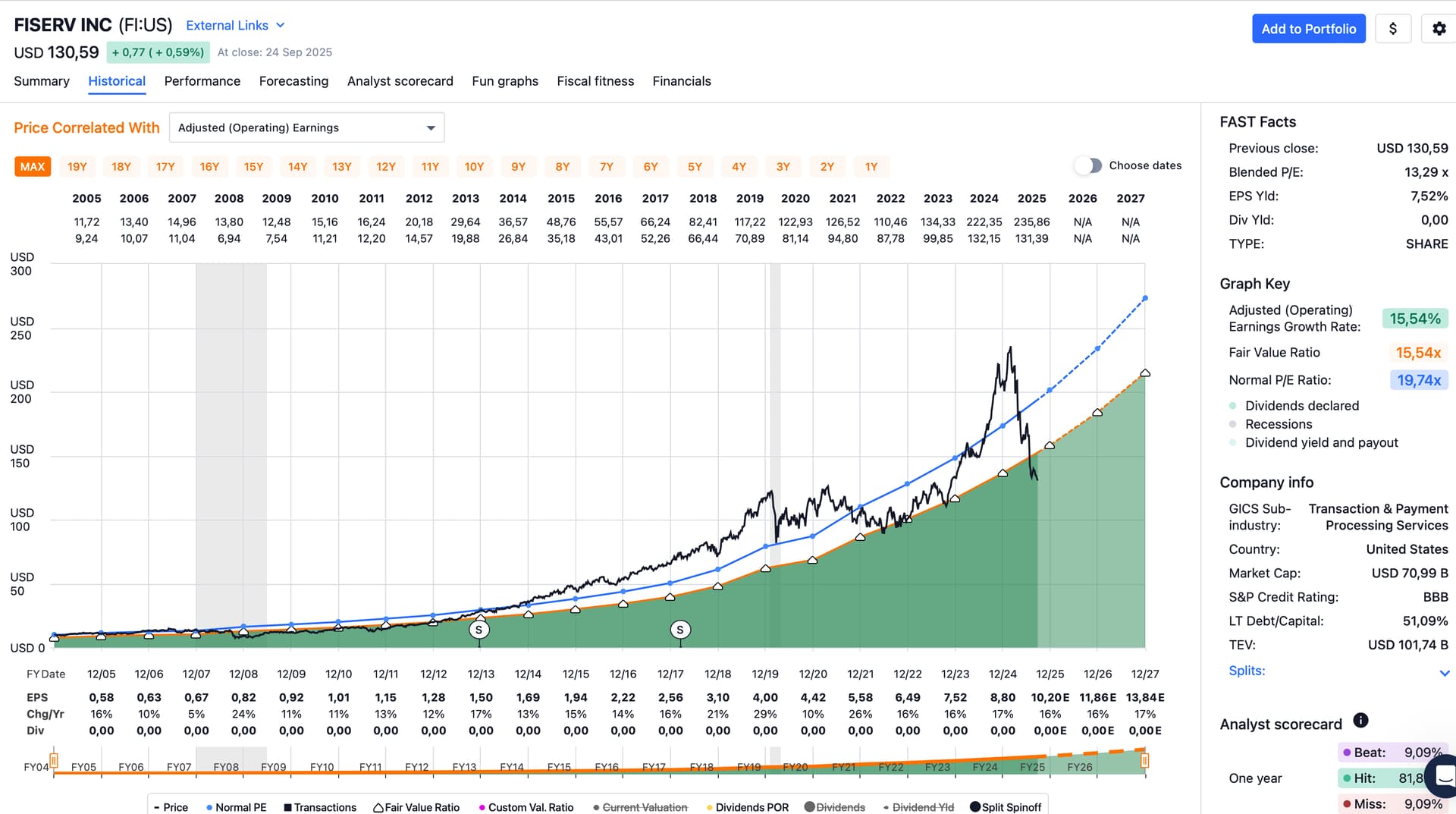

- FI: from my “junior portfolio” (which I manage for my son). Not sure about their correlation to AI.[$$$$]

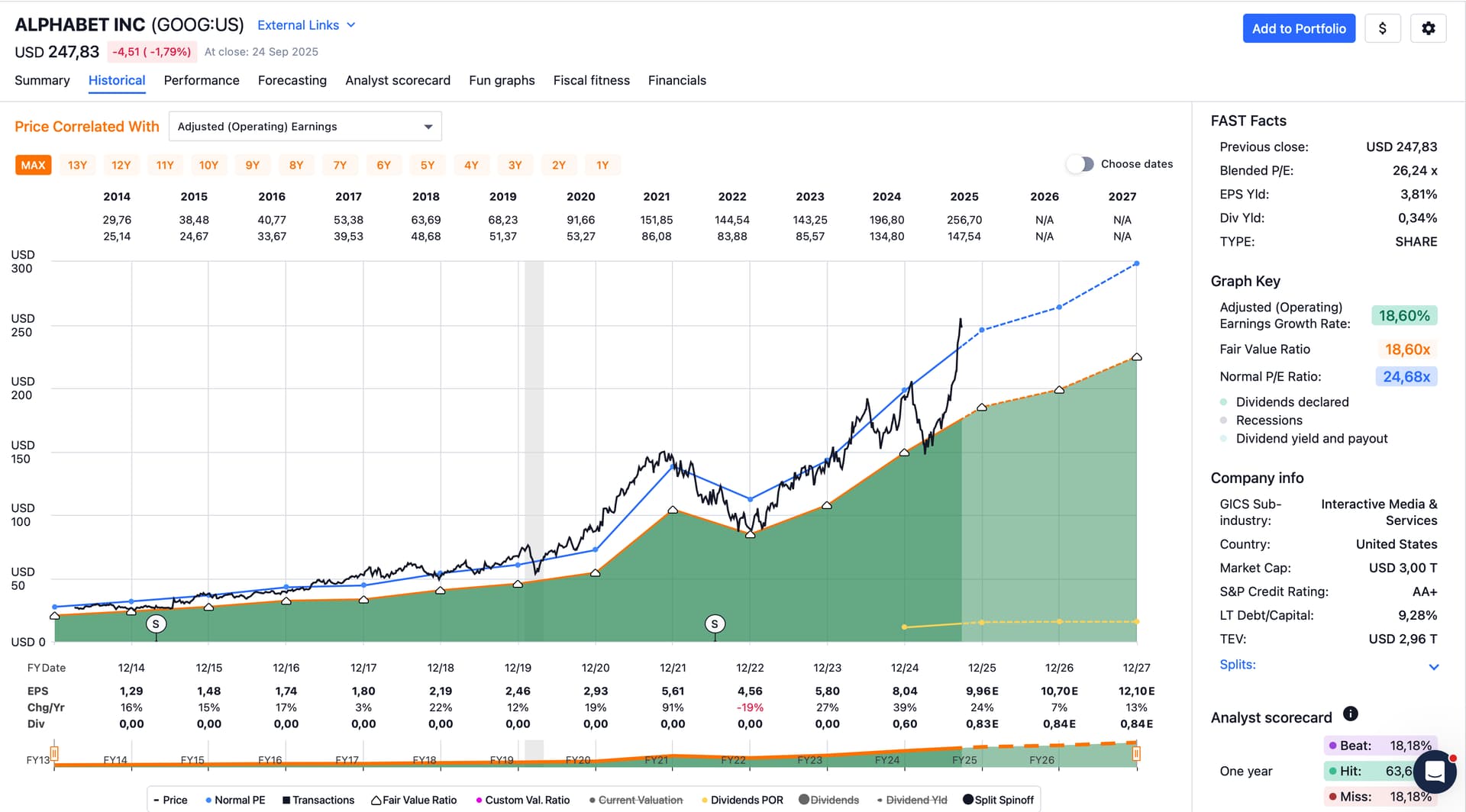

- GOOG: IMO fairly tied to AI: for their own offering (Gemini) they’re independent as they’ve developed their own custom silicon (TPUs), but for their cloud offering their customers want Nvidia and its ecosystem.[$$$$$]

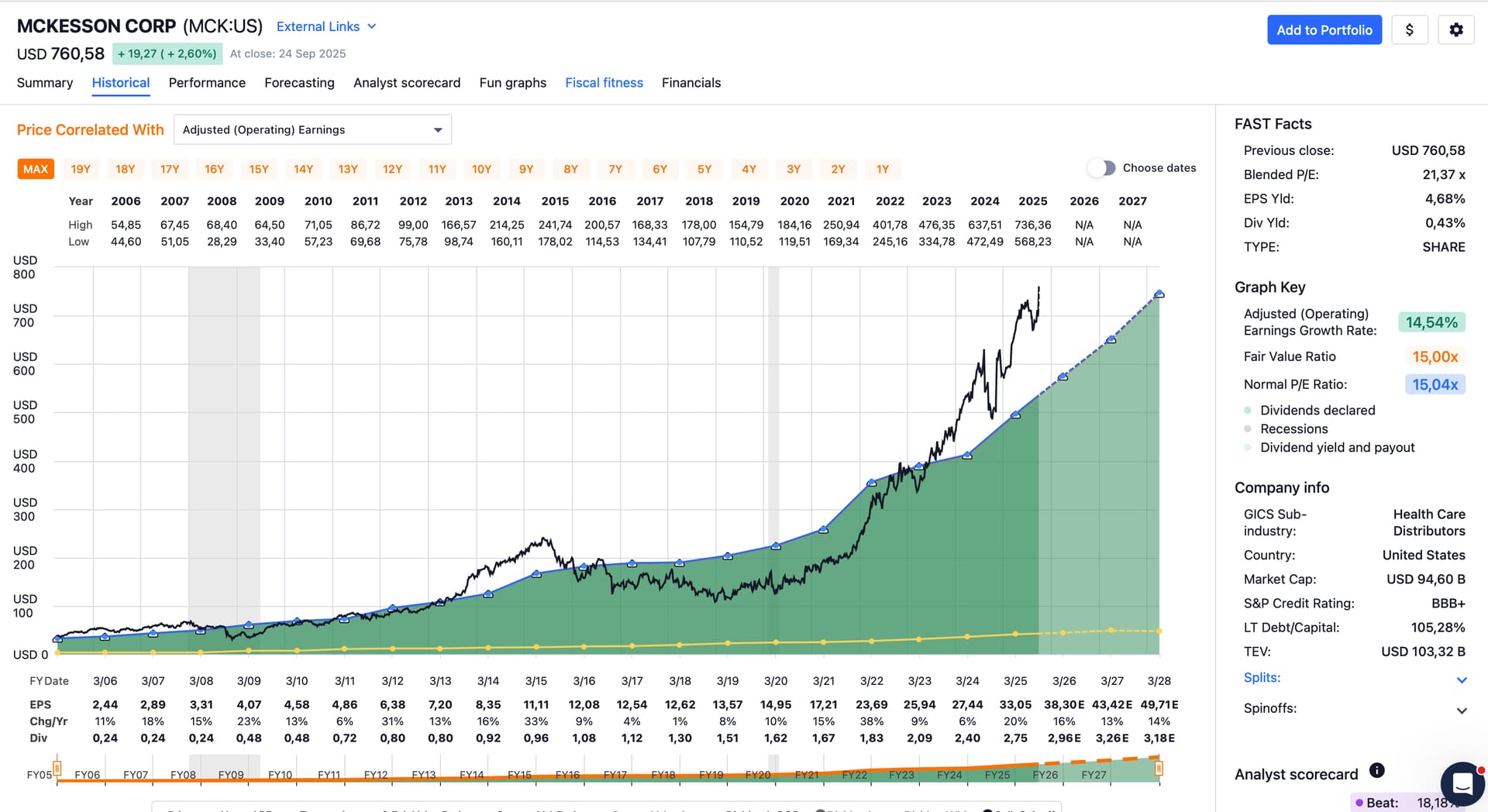

- MCK: from my “junior portfolio” (which I manage for my son). A little overvalued at the moment; probably only little correlation to AI.[$$$$$$]

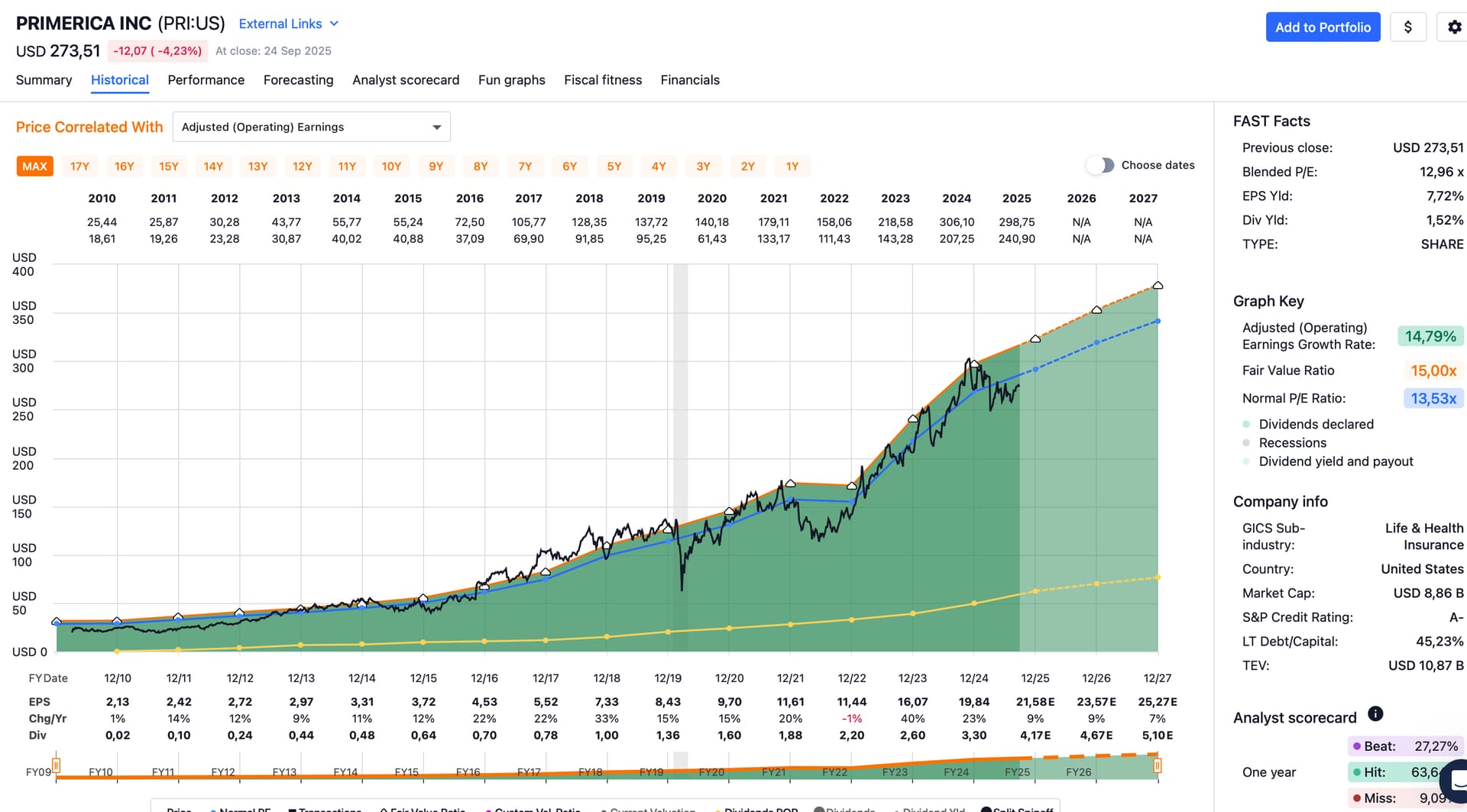

- PRI: from my “junior portfolio” (which I manage for my son). Fairly valued at the moment; probably only little correlation to AI.[$$$$$$$]

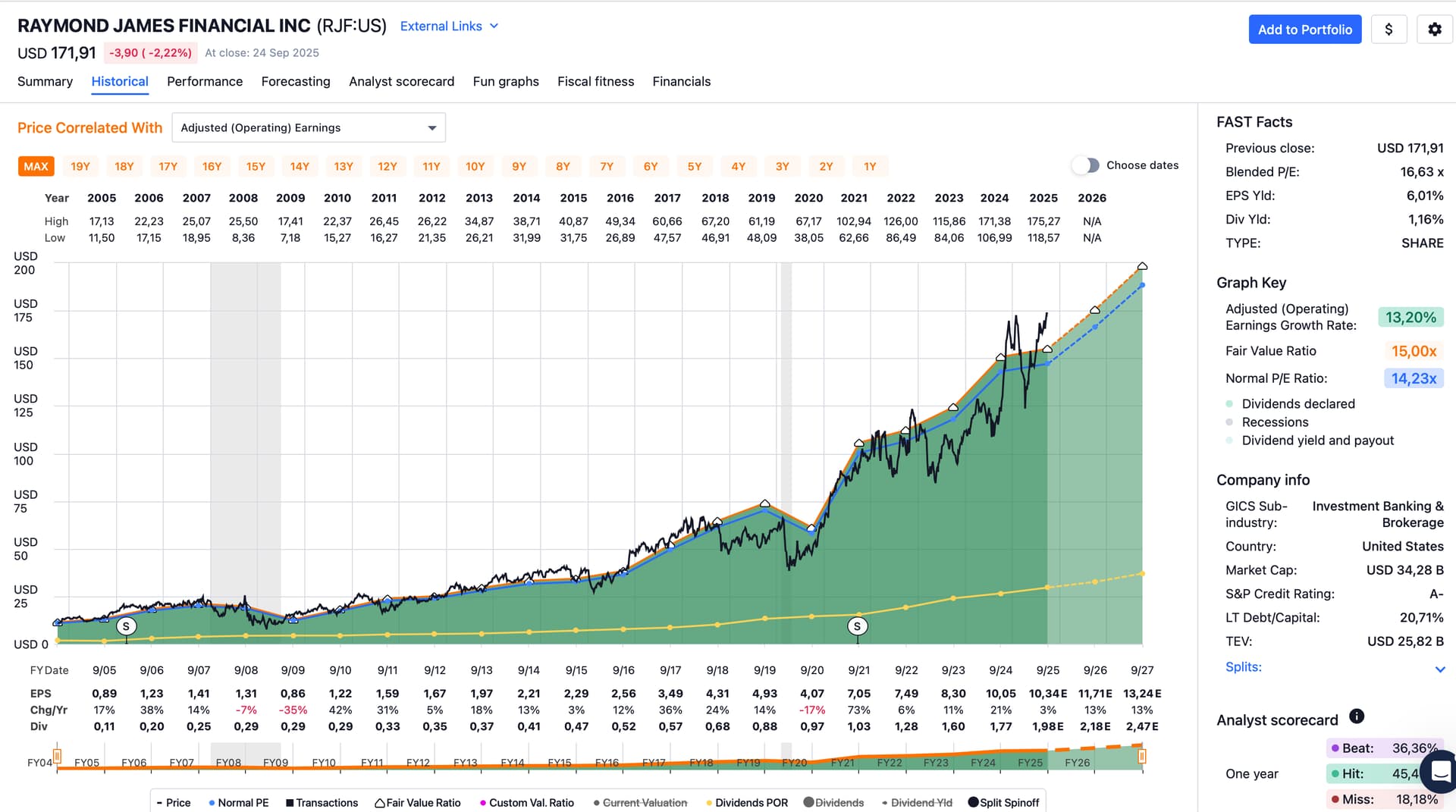

- RJF: from my “junior portfolio” (which I manage for my son). Tad overvalued at the moment; probably only little correlation to AI.[$$$$$$$$]

- SNA: from my “junior portfolio” (which I manage for my son). Tad overvalued at the moment; probably only little correlation to AI. Perhaps on the upper end of dividend payout for what you are looking for.[$$$$$$$$$]

Many financials …

This.

$ AMZN

$$ AMP

$$$ BRK.B

$$$$ FI

$$$$$ GOOG

$$$$$$ MCK

$$$$$$$ PRI

$$$$$$$$ RJF

$$$$$$$$$ SNA

1 Like

Hey, thanks so much for the detailed answer. Much appreciated!

Just got myself a bit of exercise: PTON

It’s much lower than before the COVID bull run started. Bombed out. Now there are more users than before, new products in the pipline and cost reduction done. No reason why it cannot rise a bit.

Sold off the rest of BTU today after it went up another 7% also sold off HCC. Kept AMR.

I like coal as an unloved sector, but find it hard to stomach these multiples.

There’s a coal story for you: GCM Resources PLC. Bangladesh is considering energy autarchy. Instead of buying coal from India, they could develop their own mine. Interim government with Nobel laureate Mohammed Yunnus can’t take decisions, hence everyone is waiting for elections in early 2026. Could become a 5-to-10-bagger.