I might start trimming my gold/gold miner positions. So get ready for the next leg up! ![]()

They’ve grown now to take positions 5, 6 and in the Top 10 ![]()

BTI

AMLP

CAOS

WDS

NEM

GLDM

ELV

ARE

AEM

URNM

I might start trimming my gold/gold miner positions. So get ready for the next leg up! ![]()

They’ve grown now to take positions 5, 6 and in the Top 10 ![]()

BTI

AMLP

CAOS

WDS

NEM

GLDM

ELV

ARE

AEM

URNM

TL;DR: It’s a buying opportunity IMO

I’m biased as I am a shareholder and MRK is an almost full position in my portfolio (and I’m even short a 75P expiring in December …) so take my view with a grain of salt. ![]()

Merck seems like a fine business to me and I’d probably add at these levels if my position wasn’t already almost full. If you ignore the price line for a minute, then the earnings line looks fine except for that hiccup in 2023. According to Gemini, the earnings drop was not the result of a commercial slowdown or operational weakness[1] which is also how I remember it. The company even guided for it which is why the price held up until just about around the time that … Trump won the election!

Pretty much the entire healthcare sector has been under pressure since then as Trump ran on the promise to bring healthcare costs down.

Maybe he will. In the meantime, earnings expectations for most of these healthcare companies still look fine and Trump will be gone again in a couple of years.

Executive Summary: The Paradox of Growth and Decline

An in-depth analysis of Merck’s (MRK) 2023 financial performance reveals a significant dichotomy between its top-line revenue growth and a dramatic decline in reported earnings. The precipitous drop in both Generally Accepted Accounting Principles (GAAP) and non-GAAP earnings was not the result of a commercial slowdown or operational weakness. Instead, it was a direct consequence of substantial, non-recurring, and one-time charges related to strategic business development transactions. These charges were the primary financial mechanism by which the company executed a proactive, long-term strategy to diversify its product pipeline and mitigate the future risk posed by the impending patent expiration of its blockbuster oncology drug, KEYTRUDA.

Merck’s underlying commercial performance remained robust, driven by the sustained strength of its oncology and vaccines franchises. The company’s calculated decision to heavily invest in its future, rather than to maximize short-term profitability, positions it for a return to strong earnings growth in the years to come, as evidenced by its positive forward guidance. Therefore, 2023 should be viewed not as a year of decline, but as a pivotal period of strategic transition and capital allocation designed to secure long-term value.

| Metric | Year Ended Dec. 31, 2023 | Year Ended Dec. 31, 2022 | Percentage Change |

|---|---|---|---|

| Total Sales | $60,115 million | $59,283 million | +1% |

| GAAP Net Income | $365 million | $14,519 million | -97% |

| Non-GAAP Net Income | $3,837 million | $19,005 million | -80% |

| GAAP EPS | $0.14 | $5.71 | -98% |

| Non-GAAP EPS | $1.51 | $7.48 | -80% |

| Strategic Investment | Financial Impact on 2023 |

|---|---|

| Total Business Development Charges | $6.21 per share |

| Daiichi Sankyo Collaboration | A significant portion of the total charge, including a $4.0 billion upfront payment and a $1.69 per share charge in Q4 |

| Prometheus Biosciences Acquisition | A significant portion of the total charge, stemming from the $10.8 billion acquisition |

| Other Transactions | Remaining charges from other acquisitions and agreements, such as Imago BioSciences and Caraway Therapeutics |

The timing of these monumental investments is not coincidental. The impending patent expiration of the company’s leading drug, KEYTRUDA, in 2028 is a known and significant future risk. A pharmaceutical company’s viability is fundamentally tied to its ability to continuously innovate and replace the revenue from aging assets. The 2023 earnings drop is a direct financial manifestation of Merck’s proactive strategy to address this patent cliff years in advance. The company is leveraging its current profitability to acquire and develop the drugs that will power its growth for the next decade. This is a crucial distinction that redefines 2023’s performance as a strategic reinvestment rather than a financial setback.

| Product Franchise | 2023 Sales (in millions) | 2022 Sales (in millions) | Percentage Change |

|---|---|---|---|

| KEYTRUDA | $25,011 | $20,937 | +19% |

| GARDASIL/GARDASIL 9 | $8,886 | $6,897 | +29% |

| JANUVIA/JANUMET | $3,366 | $4,513 | -25% |

| LAGEVRIO | $1,400 | $5,700 | -75% |

This data visually demonstrates that the company’s core growth drivers were exceptionally strong, and the overall sales increase was achieved despite significant declines in other product categories. This substantiates the argument that the earnings drop was not due to a commercial failure, but rather a deliberate, strategic action.

Strategic Context and Forward-Looking Outlook

Merck’s 2023 performance must be understood within the broader context of its long-term strategy and the evolving pharmaceutical landscape. The substantial, multi-billion-dollar investments in mergers, acquisitions, and collaborations are a direct, proactive strategy to diversify the company’s pipeline ahead of KEYTRUDA’s looming patent expiration in 2028. The company is actively building a portfolio to secure a sustainable long-term revenue stream to counter the inevitable decline in KEYTRUDA sales that will follow its loss of exclusivity.

By acquiring novel assets, such as Prometheus Biosciences and Caraway Therapeutics, and forging key partnerships for next-generation therapies, such as the Daiichi Sankyo ADC collaboration, Merck is laying the groundwork for future growth. These strategic moves position the company to maintain its leadership in oncology while also expanding into new therapeutic areas like autoimmune and neurodegenerative diseases.

The company’s positive guidance for 2024 underscores its confidence that the 2023 earnings drop was a one-time, non-recurring event tied to these strategic investments, and not a sign of long-term weakness. Merck anticipates worldwide sales to be between $62.7 billion and $64.2 billion and projects Non-GAAP EPS to be between $8.44 and $8.59. This guidance signals a significant rebound and a return to strong performance, which aligns with the company’s view of a fundamentally healthy business.

Merck’s position as a top-tier pharmaceutical company by 2023 revenue ($60.1 billion) provides a clear benchmark, ranking it among the industry’s leaders. Furthermore, the challenges faced by its older products, like the decline in COVID-related LAGEVRIO sales, are mirrored by similar experiences at Pfizer and AbbVie , indicating a common industry trend rather than an isolated corporate issue. The company’s strategic investment in new technologies, such as AI and next-gen therapies, is also a major trend across the entire pharmaceutical sector, which is increasingly focused on innovation to address rising R&D costs and supply chain disruptions.

Conclusion: A Year of Strategic Transition, Not Decline

The sharp decline in Merck’s reported earnings for 2023, while visually jarring on a financial statement, was a direct consequence of a deliberate and strategic pivot. The company leveraged its robust financial position to execute major acquisitions and collaborations, incurring significant one-time charges that were accounted for in the fiscal year. These investments were a proactive and calculated measure to address future challenges, most notably the impending patent expiration of its blockbuster drug KEYTRUDA, and to secure long-term growth.

The underlying commercial performance, driven by core growth assets like KEYTRUDA and GARDASIL, was exceptionally robust. The earnings drop was a temporary and calculated trade-off, a financial manifestation of the company’s strategy to secure its future. Therefore, 2023 should not be viewed as a year of decline for Merck, but rather as a pivotal year of strategic transition and portfolio reinforcement that has positioned the company for sustained success in the years to come.

The under-valuation deceives a bit - Just off your Merck graph to the right, in 2028, Keytruda patents start expiring. Keytruda is the best selling drug in the world today, a mega-giga-blockbuster-drug with annual revenues of about $30B, over 50% of Merck’s total revenue. Keytruda revenues will probably drop 30-40% annually. Very difficult (to predict whether) such a patent cliff of one drug can be navigaetd without significant drop in EPS. I would say no. New drugs have a revenue ramp-up time, as new indications get added over the years. No way to replace 30B by 2030. The “undervaluation” may be gone very quickly. Still an OK holding for the dividend and maybe a “normal” valuation by 2030.

I remember when ABBV was hit hard due to anticipated Humira expiry. They completely overreacted. I remember buying some in the $60s - then I thought, hey, even at $80, this is a bargain and bought more. I sold once it hit $160-$170, but it is now $218 today.

I own Merck and it is actually on “hold” state because of the last quarterly cash flow statement. I bought Merck from 2020 until February this year with an average price of $81.81, almost no gain or loss, but nice dividends.

On first sight the reason for the “hold” state is a FCF dividend payout ratio of over 100% in the last quarter. I hope that gets better soon, until then I just wait and get paid nicely for that.

In other healthcare news MRNA slumps 7% as FDA plans to link child deaths to the vaccine. Fun times to be a healthcare shareholder.

I held on to it.

Might sell some if it continues to be overvalued and goes up a bit more.

ABBV’s Humira patents expired in 2016 in the US and 2018 in the EU. Biosimilars didn’t hit the market until 2023 which is nicely visible in the earnings line.

As you say it’s hard to predict when this will actually hit their earnings. In ABBV’s case it took another five years or so until biosimilars came to market and started to eat into ABBV’s Humira revenue (which is still selling quite fine as some doctors/patients won’t switch brands).

Perhaps a Keytruda generic drug is easier/faster to bring to market. Surely, @Mirager can speak to the complexity of these drugs and let us know of the date (just the month/year, not down to the day) when Keytruda competitors will enter the market after the patents start to expire.

Is MRK the one with management morale issues? I remember researching a pharma company, it could have been MRK but maybe another and there were huge complaints from within the organisation about bad management, loss of staff and general dis-array in the organisation. It was enough of a red flag not to buy.

I thought you’d know better: that’s 99% of all companies …

obviously, I meant beyond that average 99% baseline ![]()

I hold ABBV too, bought since 2020, last buy in January this year. Nice average gain of 155% plus the tasty dividends.

It is on “hold” too because it is slightly overpriced according to my cash flow parameters. But then overvaluation is almost never a trigger for me to sell, unless the stock is in the lower half of momentum of all my dividend stocks.

I don’t actually know, there are other drugs of the same class, borderline interchangeable, there are also Chinese versions that the FDA hammered, possibly slightly protectionist.

Um, so … about your preference for looking at quarterly financial statements …

Hey, don’t shoot the messenger, please, but I hate to break this to you. Fresh from the Wall Street Journal:

Trump Calls for Ending Quarterly Earnings Reports

I had nothing to do with this, honest to God!

Isn’t Drumpf just an exceptional talent at letting wither everything he touches … ?

Image generated by ChatGPT in the style of Bram Stoker's Dracula -- directed by the great Francis Ford Coppola -- where there indeed is this scene where Dracula, played by Gary Oldman, has just returned from a night out, and he is a monstrous, bat-like creature. He approaches a vase of roses, a symbol of love and beauty, and his clawed hand gently touches the petals. As his hand glides over them, the vibrant, crimson roses instantly shrivel and die, turning black and brittle. Exceptional movie, BTW, if you're too young to have seen it when it came out.

A kitten died in the process of creating the image above due to the power consumption of NVDA’s GPUs involved.

Edit: Sacrificed another kitten to the AI gods, but I think it was worth it:

Fun fact: after getting the above image with Drumpf, I asked both ChatGPT and Gemini to generate a version with smaller hands for the Donald. Their answer: “This image generation request did not follow our content policy.”

…

There are way more companies now into Biosimilars than there where back in 2019. Also the requirements have been (or will be) lowered from a Clinical trial perspective with the biosimilar red tape elimination act. As Keytruda is by far the most important oncology drug (the most lucrative niche of pharma) right now I would be very surprised if there is no biosimilar out the minute Keytruda loses patent. In any case, I’m invested in Merck as well.

Eh, they (Merck) will and does everything to drag out the protection as much as possible, like AbbVie does. That said biosims are a tad harder to get right than generics (=of small molecules) and pts/drs often have preferences. In any case generics/biosimilars are a GOOD thing - they increase equality. Dunno, don’t have a view into pembro generics. I was once paid to write an article FOR generics, and some months later an article AGAINST. Consultants are…concubines at times…though I’d stand by either article as well-researched and supported by evidence-based medicine, it’s just how you spin it.

Out of curiosity, any insights on Chinese pharma / biotech companies? The country does have the brainpower for R&D, manufacturing capacity and government sponsorship (which may or may not be helpful, but that’s another topic). Anything investible? Or already hyped and over-farmed?

I don’t know about investable, BeiGene (now BeiOne) is one I know being the most western, but there are many local pharmas. I think that soon we will be seeing quality innovative drugs out of China.

Looking at that chart, I don’t feel my decision to sell was a bad one. It went maybe a little out of value but as always, stocks can keep on going up for a lot longer than you expect. A continued decline in earnings in 2025 would make things look very different.

Wasn’t quite sure where to post this, but since it’s about active investors, I’ve settled for posting in this topic.

If our beloved mods know of a better place, please move it accordingly.

For those with time on their hands (55 pages often dense!) and interest in how professional active investors deal with managing Other People’s Money, this is a fascinating paper to read:

Exploiting Myopia: The Returns to Long-Term Investing by Kalash Jain, Dian Jiao :: SSRN

It dives into the reality of active institutional investors and how they deal with redemption pressure where many fund/ETF managers let go of weakly performing companies, resulting in relatively short holding periods. They hypothize that this results in systematic underinvestment in firms that require longer holding periods to realize value. They then construct a factor – Horizon – that is a proxy for the holding period of individual stocks and derive that funds/ETFs with larger Horizon (holding periods for individual stock) tend to have significantly better returns.

It’s at first almost obvious that – big if: for fundamentally sound companies – the longer you hold the company the more you benefit from the compounding, but it was new to me that you can systematically and rigorously show that even active institutional managers suffer from selling too early the fundamentally strong but recently weakly performing companies because the investors in their fund want out because of recent weak performance of the fund and then the fund managers sell the wrong companies too early for a bunch of reasons that are rational from the portfolio manager’s perspective, but that hurt the performance of the portfolio.

This is an edge we have as retail / individual active investors. I won’t sell a company I have conviction in, even if it performs poorly for many years.

It thus lines up with my own experience where some of my positions need 3 to 5 years to realize their value even if it seems obvious to me at accumulation time that the company is mispriced.

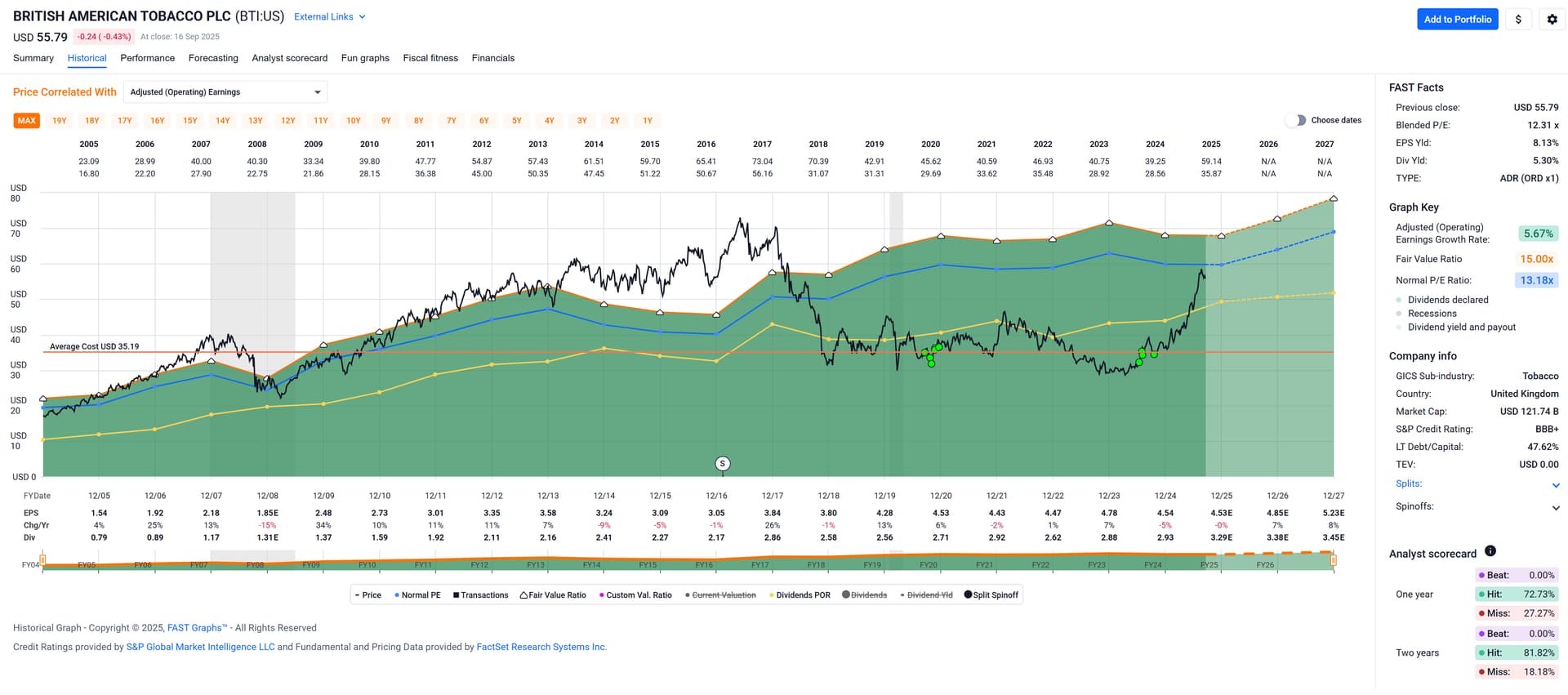

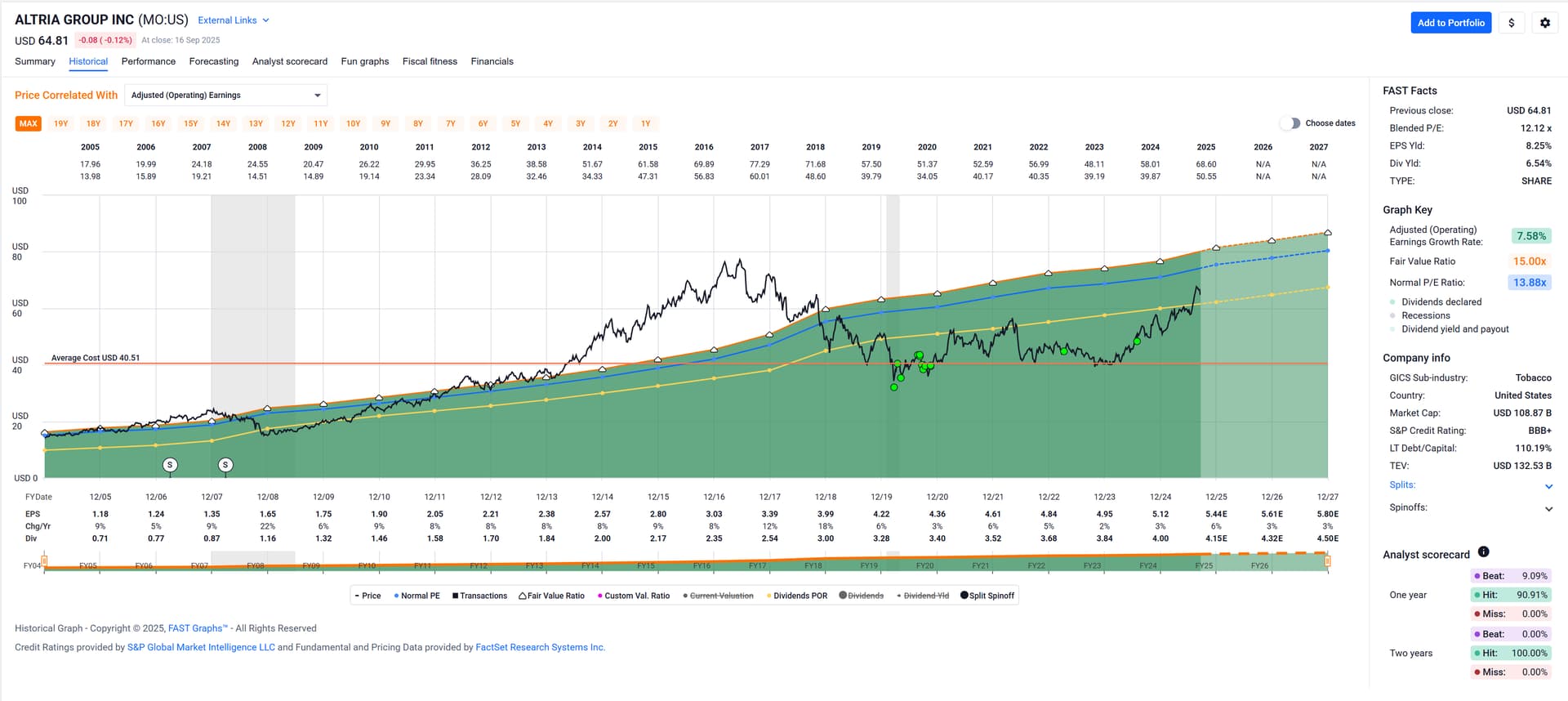

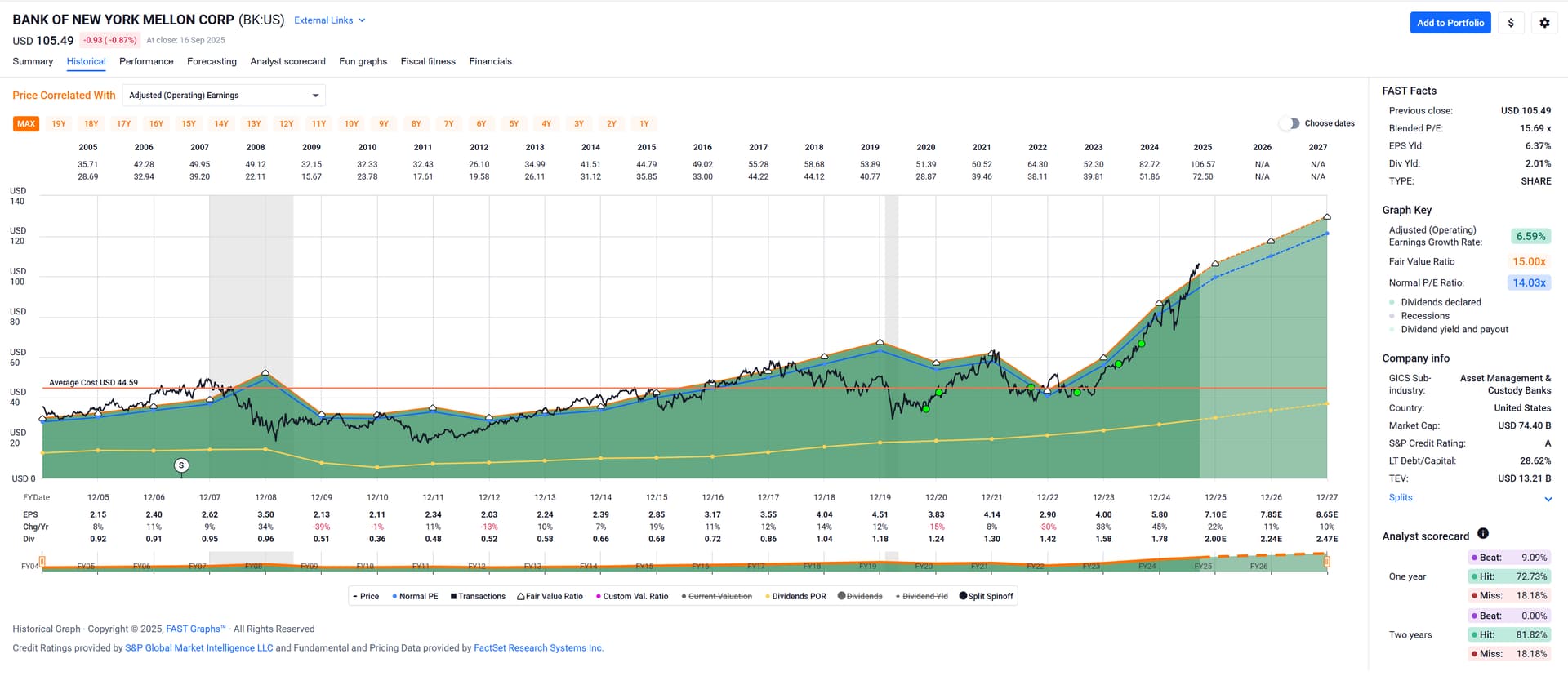

E.g. most tobacco companies (Imperial Brands,[1] British Americal Tobacco,[2], Altria[3]), but also financials (Bank of New York Mellon[4]) and many many others.

Anyway, if you’ve built the conviction that you’re buying a good or great company, the market will sometimes test your conviction for more than just a couple of months, maybe even more than a couple of years, but 3 or even 5 years until your returns will realize.

It helps if that waiting period is cushioned with dividends, at least in my case.

1 Imperial Brands

2 British American Tobacco

3 Altria

4 Bank of New York Mellon

Edit: Looks like I edited an earlier reply instead of creating a new post. Don’t quite know how to untangle this, but the earlier reply wasn’t that important anyhow, so I’ll leave this as it is.

Beside BeiGene which is definitely the most known for Europeans, I have worked with Zai Labs (ZLAB) but looking on their share price performance it’s not ideal. I was also thinking several times now to buy the KURE ETF but my buy order have never been filled. Looking at the performance now that is to bad. All in all a quiet challenging market as it’s unknown what the goal of these companies is (China forces only or globally, independence, etc)