I am new to EFTs and I am about to open an account with IB to invest my capital(cash) that sits in Europe (in Euro).

I have already spent -hours- looking at the documents/guides . Despite that I would appreciate your help regarding the following points because the information are a lot and I am getting a bit confused:

does it make sense to buy European domiciled ETFs (note that the ETFs would invest globally)?

Notes: the reason why I choose to buy European ETF and subscribe to IB is due to my mobility. I am trying to build a portfolio where I don’t want to be forced to sell my assets in case I have to move to another country (most likely in Europe).

Just for information, this is where I plan to invest:

(30%) Lyxor Core MSCI World (DR) UCITS ETF

ISIN LU1781541179 (or something equivalent)

and

(70%)Xtrackers Global Sovereign UCITS ETF 1C EUR hedged

ISIN LU0378818131

Is there a way to predict the fees before purchasing assets with IB? Some kind of calculator?

Notes: I will choose a tiered pricing model. I tried to use the IB demo version and I could see a cost estimation but it is not clear what is the pricing model configured (IB support did not help). Based on the document I expect to pay between 50Fr and 100 Fr when I buy/sell ETFs. Is that a good assumption?

I asked the same question to IB but they did not answer.

Option “eligibility for a U.S. benefit tax treaty” : does it make sense to answer “yes” when my plan is to invest in European ETFs and I am not a US citizen ( I am European)?

This is recommended here (section 13), I suppose that probably that aspect can be used for tax/commission deduction. The reference document does not explain why it is recommneded.

Ref. IB subscription guide: How to open an Interactive Brokers account? - Mustachian Post?

ETF :. accumulating vs. distributing

I would prefer to use accumulating ETFs but ,according to the link below, accumulating ETFs are more complicated in terms tax declaration . Should I really care about that aspect in case I use an accountant for my tax declaration??

“If the swiss tax authorities cannot figure out what is dividends and what is course gains, simply everything is taxed, including the usually not taxed course gains.”

reinvesting dividends: does IB offer some kind of reinvestment advantages/bonus for reinvesting dividends ? I read on Investopedia that some brokers offer this kind of feature.

If you’re moving to other European countries, probably.

Fees are on their web site. I think they also show commissions when ordering in client portal.

50 to 100 CHF per trade sounds like a lot in fees - what amount / numbers volume are we talking?

Side note: IBKR has a bit of a reputation of holding your hand in customer support.

It doesn’t change anything (on EU income) but it can’t hurt either (if you answer truthfully), can it?

They aren’t anywhere more complicated than distributing ETFs as long as they are listed on the ICTax web site (for Swiss tax purposes, that is). Now if you’re thinking of moving to another country, it could get hairy, if the fund (or the tax authority) aren’t delivering you the figures for accumulated dividends for tax purposes. On the other hand, some countries might only tax realised income and gains. A distributing fund might be less advantageous than an accumulating in this case.

If you’re moving to other European countries, probably.

Fees are on their web site. I think they also show commissions when ordering in client portal.

50 to 100 CHF per trade sounds like a lot in fees - what amount / numbers volume are we talking?

Side note: IBKR has a bit of a reputation of holding your hand in customer support.

It doesn’t change anything (on EU income) but it can’t hurt either (if you answer truthfully), can it?

Thanks for your feedback

I was just looking for a reference number for an investment of 100K. Regarding IB support, I find the communication a bit slow using the email. Perhaps I should open the account with some funding to get some attention?

There are no explanations on the guide about why I should answer yes (to the “eligibility for a U.S. benefit tax treaty”). I suppose there is some agreement between the US and CH…but the criteria are not that clear to me and I am not sure about.

EDIT:

about point 3:

I believe I found some key info here:

" however, for foreign investors (swiss domiciled…), by default, US based funds & companies pay 30% (=L2WT) of withholding Tax from distributed dividends to the US tax authorities. BUT ,it takes some effort to get there: you need to file a [W8-BEN ] form for this. Your broker needs to be a “qualified intermediary” for this. From IB we know they directly do it when you sign up."

I suppose that being a Swiss citizen (B-permit) I can leverage on that treaty. That’s probably what the IB subscription guide, section 13, is referring to… Still, the ETFs I have chosen both have an ISIN starting with LU (Luxemburg) , so perhaps I am not eligible for this benefit . Actually I am not even sure whether that is a good way to find out where the ETF domicile is.

It depends. Most countries have a similar system like Switzerland, where you can get the 15% of withheld taxes back. It isn’t a huge issue if you can’t get it back because the US ETFs are also cheaper.

You won’t be able to buy new shares in Europe.

You need to be careful anyway, I’m not sure how the tax treatment of capital gains is, if you migrate.

I’m not sure about the tax treatment for US dividends to an etf in Luxenbourg. Note that this etf mearly has a bit over 100 holdings and holds Total return swap. You would probably be better of just buying a real swap etf like the one from invesco.

Swap etfs are more tax efficient, because they do not lose any withholding taxes.

You want to hold quite a lot of bonds. Do you need the money in the next 5 years? When do you want to move to Europe?

If you want to buy 100k-200k chf of ETFs on European exchanges, then that seems right.

The same is much cheaper if you buy US ETFs.

Buying 200k of VT will cost you less than 10 chf in fees. So going with VT and selling if you migrate is also a viable options as spreads are also quite low. If you plan to stay longer than 2-3 years, it is probably cheaper to just go VT. It might also be beneficial to sell anyway because of capital gain taxes in European countries.

for my usual investment cycle i change a few 1000’s CHF to USD for between 1-2 CHF in fees, and purchase up to 6 positions for typically 0.33CHF each. This totals in ~CHF 4 for a couple of thousand swiss fancs invested.

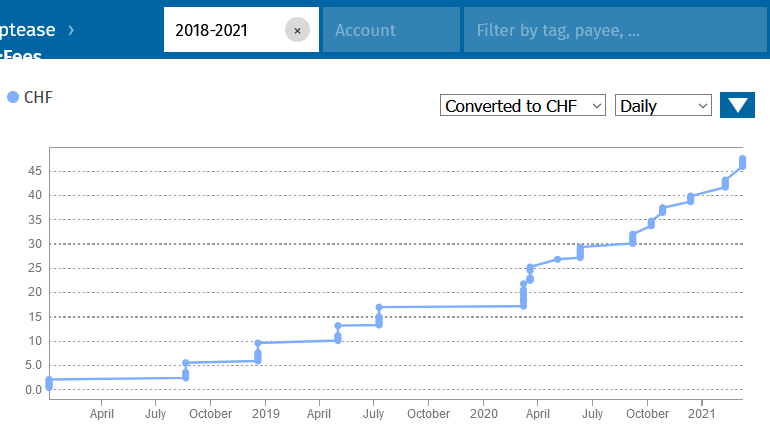

since 2018, i paid about CHF 47 total in fees with IB

Note that at the moment my capital is fully cash (EUR) since one year so any rational investments could be sufficient for me without the need to fine tune every possible cost . As a non expert I am just trying to avoid big mistakes with the taxation of other regulatory things.

Most countries have a similar system like Switzerland, where you can get the 15% of withheld taxes back. It isn’t a huge issue if you can’t get it back because the US ETFs are also cheaper.

You won’t be able to buy new shares in Europe.

Thanks, in case I am not forced to sell then I should probably consider to buy american ETFs since I planned to invest 70% of my capital and that could save me some commissions (expected 90/100Fr saving as per the reference cost you provided in your previous message)

Deciding the domicile of the ETF is quite complicated because I don’t really know what are all the pros and cons yet and considering the amount of money invested I am a bit concerned about taking the step or not.

I’m not sure about the tax treatment for US dividends to an etf in Luxenbourg. Note that this etf mearly has a bit over 100 holdings and holds Total return swap. You would probably be better of just buying a real swap etf like the one from invesco.

Swap etfs are more tax efficient, because they do not lose any withholding taxes.

To be honest I chose both the ETF without going to deep in technicalities (I checked the fund size, costs and compared the back-tests with few other combinations) . It is actually a combination copied by sample lazy portfolios using EU ETFs here

I suppose the Invesco ETF you are talking about is [IE00B60SX394] (Detailed Comparison for ETFs | justETF) . That’s IE domiciled . The TER is a bit higher though . Do you believe I should reconsider?. I suppose that the 15% of taxes I save investing in IE will probably reduce the TER by some decimal points.

Besides that , how did you check the number of holdings? I read the fact sheet and I could not find it.

You want to hold quite a lot of bonds. Do you need the money in the next 5 years? When do you want to move to Europe?

I don’t have plans to spend those money now but I am not sure. My primary intention was to avoid the negative interest on my bank account investing in ETF, create a conservative portfolio and try to speculate (rebalance/become more aggressive) when the markets fall.

Yes, the tax saving should be around 0.25% per year.

Note that the MSCI world only covers around 75% of the total world market. It is missing small caps and emerging markets (and frontier markets, but nobody cares about them)

I only found the holdings in the halve annual report.

Here is a portfolio, that covers a bit more and avoids small cap growth companies:

However it also misses Small caps from Japan, Australia, Canada and Israel.

Don’t time the market. It is not a sound strategy.

If your investable amount is a six-figure amount and you’ll be making a lump-sum investment, I’d rather worry about 90 CHF on the purchase of your next shoes than on broker commissions.

To be clear, there’s two or three good reasons to prefer U.S.-domiciled EFTs for many, probably most (though not necessarily all) people. Maybe not for you. It can also depend on your future jurisdiction.

Anyway, these one-time commissions should only be a very minor decision-making factors, if at all.

(Strictly speaking the aren’t one-time, since U.S. are distributing, and you’d pay commissions on reinvestments of distributions).

If your investable amount is a six-figure amount and you’ll be making a lump-sum investment, I’d rather worry about 90 CHF on the purchase of your next shoes than on broker commissions.

yes, that’s actually was my conclusion as well at the moment. I was only trying to better understand whether the impact of those “details”(optimised taxation/regulations) is negligible to some extent + getting some feedback in general.

Actually I was willing to ask for advise from an independent professionals as well but I really could not find one.

When this is going to happen? Any time or in few years?

There is no problem to sell and, as others pointed out, you better do it while you are Swiss tax resident and is not taxed on capital gains. Meanwhile keeping recurring fees (TER + withholding taxes) low is more important.

If you are not buying US ETFs, then I think you don’t necessary need IB. You can go for e.g. a German bank (flatex, DKB) broker or even Degiro in one of EU countries. This way you don’t even have to do a currency conversion. Worth comparing.

If you are not buying US ETFs, then I think you don’t really need IB. You can go for e.g. a German bank (flatex, DKB) broker or even Degiro in one of EU countries. This way you don’t even have to do a currency conversion.

I have some kind of gipsy life. IB supports more countries, and that would save me from changing broker or creating complications (hopefully). It has probably more securities available . Fees are probably lower (perhaps not that much for non US securities?). Another interesting comparison for European investors.

That’s why I thought it is better to use it.

Rather than investing 70% of your money in bonds I’d consider changing bank and keeping those in cash; most banks don’t charge (yet) negative interests, unless it’s a very large sum.

Rather than investing 70% of your money in bonds I’d consider changing bank and keeping those in cash; most banks don’t charge (yet) negative interests, unless it’s a very large sum.

I thought about that, I thought to wait for the market to drop as it is growing a bit too fast but based on the backtests of the combined ETFs, I can tolerate the market fluctuations and I prefer to have the money on the market instead of wasting time looking for bank accounts.

For your information my bank in the NL, lowered the negative threshold for negative interests from 2.5M to 150K in 12 months.

Postfinance has already several thresholds set to 100K 250K 500K depending on your situation.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.