Now I have:

25% SPI extra

12% SMI

30% CSIF world ex CH (in USD)

rest is cash waiting for a dip like these days’ one

If I look for funds denominated in CH (no bonds), I see:

CSIF SMI (costs 0%)

CSIF SPI extra (0%)

UBF ETF SLI (0.2%) not sure how this one differs from the SMI above - need to check

CSIF CH real estate (0%)

Would it make sense to find a balance between only these funds to avoid the high fees on USD/CHF conversion?

The assumption is that I have the rest of the world covered in IB, in USD and EUR, and VIAC would only have enough funds to justify exposure to CH market.

I ran the numbers and by buying the max allowed of SPI, SMI and real estate with all my viac money I would achieve a 10% stock exposure to CH (also taking into account my other etfs which contain swiss stocks) and 1% of my NW in terms of Swiss REITs, which I find good.

Unfortunately, by maximizing all these funds I am still left with 15% cash, a bit too much for my taste. Maybe some corporate bonds? Will have to decide tonight, hoping the bottom is in.

That’s what I would ideally do, but without leaving the CHF I can only buy the UBS SLI fund which is exactly like the SMI and costs 0.2. Maybe I get some world ex CH and forget about some forex exchange fees…

As a short aside, I really wish the VIAC app showed the total combined balance of all opened 3a accounts on the very first screen, rather than making you swipe through and calculate it all manually…

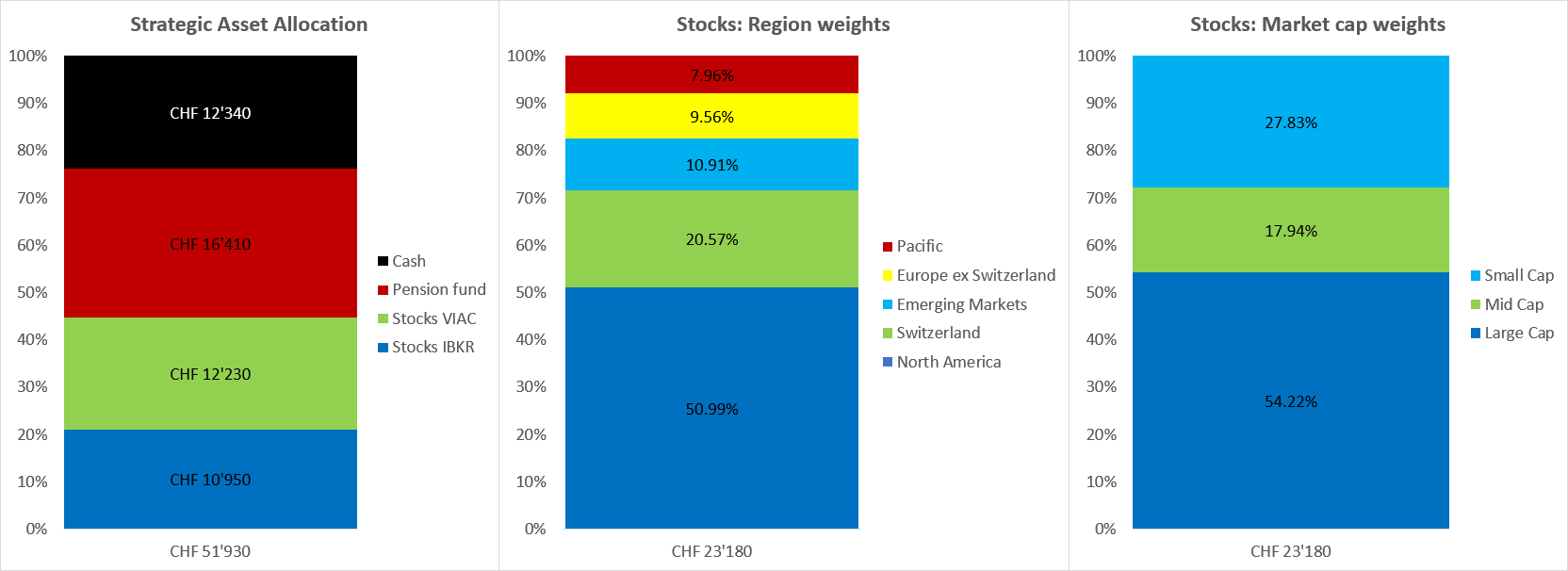

No, because I have VIOV (US small cap value) in IBKR and I always look at my total portfolio. In VIAC I use 7% SMI, 30% SPI Extra, 18% Europe ex CH, 10% Japan, 5% Pacific, 7% Canada and 20% Emerging Markets. In IBKR I use VTI and VIOV.

how could you lose 50% of the money “with the transfer”? must be a typo… next rebalancing should be beginning of April, not May 1st. anyway it’s hard to give you advice without knowing more of your situation.

@Neville: My time Horizon is more than 30 years… i’m 26.

@Giff: I paid the maximum during 41 months for my third pillar with Swiss Life (41x560CHF=22’960CHF-seller’s commission and penalty= 11’551CHF. That’s hard and it’s unfortunately not a typo…

Next rebalancig i’m talking about is 1.5, cause in April i will at least invest 50% in Global 100… just asking if i should go all in because of the situation now or give the market another month to invest the other 50%…?

investing in two tranches could be suboptimal in the long run, but might give you the impression of playing it safer. because you are so young it really won’t matter

Did you already pay in this year’s 6.8k into 3rd pillar?

If not - get done with it and go all in with this transferred amount from 1.4.

If yes - do the same.

You will most probably be investing much more than this amount in the coming years.

And no one knows which direction is this going now - neither till 1.4., nor 1.5 (nor 1.12., although very hopefully way upwards )

If nothing else, now is a much better time than if you had gotten in on 1.2., so you might make up at least part of those “lost” 6k sooner rather than later.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.