In your case, if buying in USD is not to expensive, it could be a great solution. The fact that it is also a capitalisation one offer you peace of mind about dividend conversion.

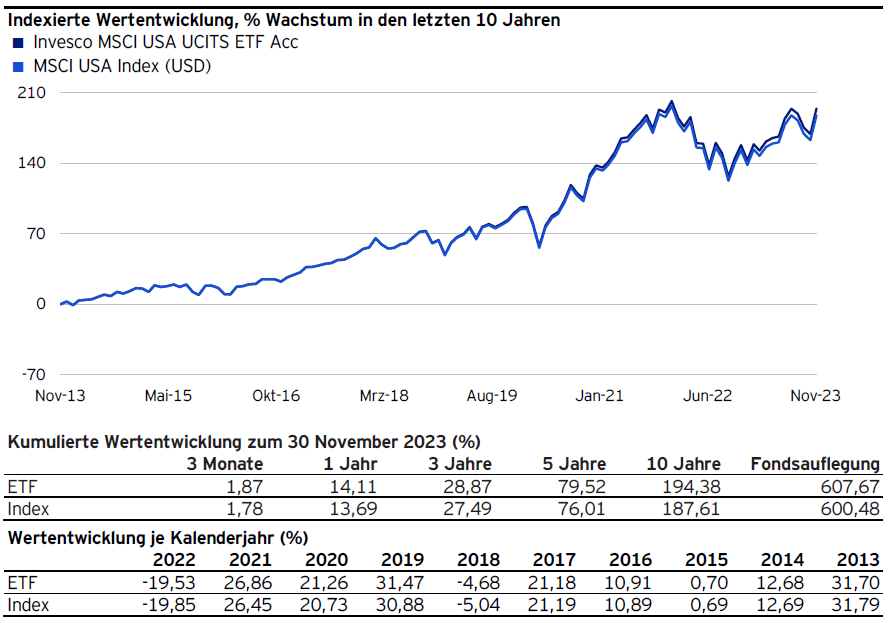

I just wonder what happened after 2017 when this ETF started outperforming its underlying index. Total outperformance is 7% if looking at the last 10 years. Maybe as @nabalzbhf pointed out it’s due to the performance drag of withholding taxes which don’t apply for this fund.

With this, you unconditionally get 15% back via R-US and you get an additional tax credit of up to 15% via DA-1 (it depends on your relevant Swiss tax rate, likely the full amount in your case). That’s assuming your declaration is accurate, i.e., your bank is an IRS qualified intermediary and deducted 15% US WHT and 15% extra Swiss withholding, not 30% US WHT.

If you sign the W8-BEN for treaty benefits, you will get taxed 15% (double tax treaty reduced rate) + 15% (Swiss supplement as per DTT).

The Swiss supplement is always recoverable in Switzerland if your dividends are declared. The other 15% is claimable using the DA-1 (reimbursed totally or partially depending of your personal situation. It has been discussed in this forum already)

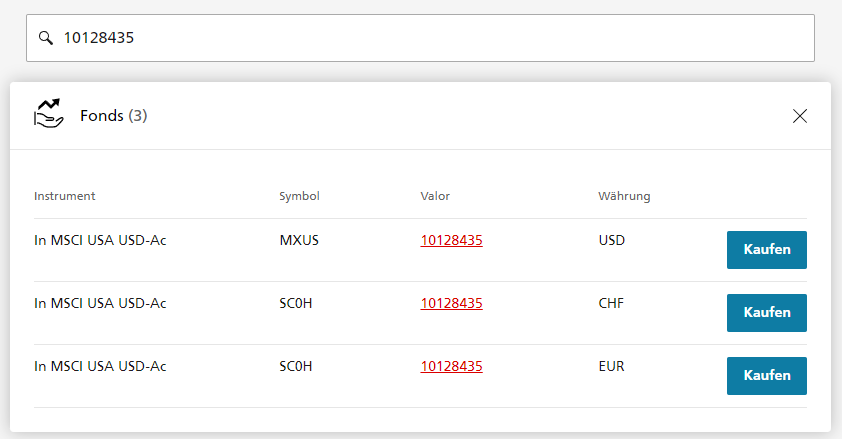

Are you sure about the CHF version? I think that justETF convert it automatically in the currency exchange website version if you are a swiss investor because it said that you can buy this ETF in USD on the SIX Swiss Exchange.

Iirc this was discussed before, IRS rules allowed to remove some tax drag for those ETFs. I don’t remember the detail and whether there is now no tax drag at all.

Broker domicile usually shouldn’t matter regarding taxation (though there are some exceptions - and often the practical question if and how you can recover tax withheld in practice, i.e. what documents need to be provided to whom).

As @nabalzbhf said, I would assume 15% U.S. tax (non-refundable from the U.S. but probably eligible to be offset against your Swiss tax through DA-1) and an additional 15% withholding in Switzerland, refundable from the Swiss tax authority.

Did you look at the actual dividend statements how much was deducted?

I have 3 fund options. The CHF-version is traded on XBRN, the USD-version on XLON and the EUR-version on XETR.

@San_Francisco

Yes, the last dividend in September got paid out with a 30% deduction. But as you and 2 others here are suggesting: 15% is offset through DA-1 and 15% is recovered through RUS.

So maybe I should just try it out with my next tax declaration early next year and see how it goes. If I get the full 30% back, I’m going to stick with VTI. Otherwise I might use the Invesco MSCI USA ETF with 100% dividend payout.

I may be a bit pedantic, but it‘s not really a different „version“ (share class) of the fund - it‘s just different exchanges allowing trading in different currencies (if you bought a distributing fund in CHF, you will still get receive dividends in the fund‘s currency, e.g. USD).

it says that L1TW is 0% for US ETFs with US stocks and L2TW is 15% that is recoverable via W8-BEN and DA-1. There is no mention of an “additional 15% withholding in Switzerland, refundable from the Swiss tax authority”.

There is - but the information provided in that link (at least for „Scenario 4: a Swiss buys the VT ETF (Vanguard Total World Stock ETF) domiciled in the US“ and particularly with regard to the DA-1 and R-US 164 forms) is inaccurate anyway.

Keep in mind that I was replying to @Cortana, who is using a Swiss broker/bank. He receives 70% of U.S. dividends paid out, as also confirmed by @Guillaume_GVA, who is using a Swiss broker too, AFAIK.

W8-BEN through a qualified intermediary will reduce U.S. withholding tax on U.S. dividends from 30% to 15%. For the remaining non-refundable 15% of U.S. WHT, you can usually (but not always) receive a corresponding tax credit on your Swiss income tax through by filing DA-1.

Irrespective of that, Swiss intermediaries (banks/brokers) have to withhold an additional (Swiss withholding tax) 15% on U.S. dividends, which, I think, you could call L3TW - which is refundable through filing R-US 164.

Just replying to this to confirm and maybe help others.

I did indeed open an IBKR account in January 2024 and by now have received the first dividends (on a US share, on a US ETF will come next week).

I can see that I clearly received 85% of the gross amount, so yes, for IBKR one does not pay 30% but only 15% withholding tax (when receiving dividends on a US share).

I will update in one year’s time how it goes with claiming this 15% back via DA-1, if I don’t forget.

Though I realised IBKR also pays broker interest (while Saxo my cash keeps decreasing for their fees, even after they lowered them, and given they are Swiss broker which has all these drawbacks, I can’t recommend IBKR over them enough, the stamp duty alone for someone who trades a lot is massive in the long run) so I’ll have to figure out how to declare these, even though the amounts are tiny, I feel like taxes should also apply the principle of proportionality.

Well they didn’t for me, and the fact IBKR made it easy (I believe it comes from the lending of shares) and Saxo don’t (of course they did pay when I had a lot of cash with them) is just another plus, and contributes to the feeling - Saxo my cash just goes down, IBKR it goes up. Of course amounts are insignificant, but it’s about the optics.

I think it’s clear IBKR rocks when the question is “who Is best broker for Swiss investor to buy stocks/etfs” . There wouldn’t be any criteria where IBKR won’t win. Except they are not Swiss.

The discussion about Saxo, SQ, Corner etc is mainly focussed on who is best Swiss broker. The choice is complicated

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.