I’ve successfully filed a DA-1 for the Vanguard VTI ETF (among other ETFs) for several years without problem but this year I got the DA-1 rejected with the (very short) motivation “Kein R-US, da ausländische Zahlstelle”.

Could someone elaborate on what that might mean? I guess “R-US” is just short for “Rückerstattung-US”.

If it matters the ETF is held in my Interactive Brokers account.

In this case the “correction” changed my refund to 0% (from 15%). Would you expect that to be in line with not correctly communicating the IB is UK domiciled?

R-US: additional tax withheld by Swiss paying agent on U.S. dividends (not applicable to IBKR accounts - hence no refund).

DA-1: non-refundable foreign withholding tax on dividends (withheld through basically all brokers, offset against Swiss income tax)

„Kein R-US, da ausländische Zahlstelle“ is correct (in itself). What you want to make sure is that you correctly requested and will receive DA-1 refund (as @Guillaume_GVA said: we haven’t seen the tax return you filed and can’t comment on that).

What you want to make sure is that you correctly requested and will receive DA-1 refund

(This was in response to my DA-1 filing. I’ve filed DA-1 for the last 10 or so years I believe, for the same ETFs.)

I contacted the authorities and got the following explanation:

Auf amerikanischen Titel können gemäss DBA maximal 15% Steueranrechnung gewährt werden. Der zusätzliche Steuerrückbehalt USA kann nur unter folgenden Voraussetzungen gewährt werden:

Es handelt sich um amerikanischen Dividenden

Aktien werden von inländischen Zahlstellen verwaltet (Beim “InteractiveBrokers” Depot handelt es sich um eine ausländische Zahlstelle)

Der zusätzliche Steuerrückbehalt USA (15%) wurde an der EStV in Bern abgeliefert

Der Vermerk: “Zusätzlicher Steuerrückbehalt USA 15%” ist auf der Abrechnung aufgeführt.

2-3 confuse me:

In (2) are they saying that getting a refund using the DA-1 isn’t possible when using IB because it’s not domiciled in Switzerland (I believe it’s domiciled in the UK)?

In (3) I don’t really understand what foreign withholding taxes have to do with Bern.

I also wonder if I incorrectly checked/didn’t check some box that was needed for (4).

No, they are saying that you can’t get a refund for the “zusätzliche Steuerrückbehalt USA” as a IBKR customer. They didn’t say anything about you not being able to get a tax credit for the 15% US withholding taxes, which is completely separate from the “zusätzliche Steuerrückbehalt USA”.

I’d suggest posting (part of) your DA-1 form here to figure out whether you may have made a mistake filling out the form (despite previous years being accepted). If you don’t want to reveal any real numbers, I suppose you can also provide a fake entry as long as it has exactly the same columns and filled out in an equivalent way.

In essence:

It’s not a foreign (U.S.) withholding tax - it‘s a Swiss one.

A Swiss withholding tax that only Swiss paying agents are subject to and that applies exclusively to dividends (…and interest?) originating from one specific country (the U.S. of A.).

It’s indeed a very unusual construct in international tax law. Not sure when and why it was introduced - but it probably had to do with Swiss banking secrecy and the U.S. (and their financial markets) being important enough to to strong-arm Switzerland into doing it.

Wouldn’t it be instead to the benefit of Switzerland so that it would match the regular withholding (35%) for domestic dividends? I don’t think the US cares, it has 15% dividend with a bunch of countries anyway.

They‘ve got a standard rate of 30%, so they seem to care (you’re eligible for the reduced rate only based on residency in certain countries. Were Swiss banks allowed to communicate information regarding eligibility for the reduced rate to the U.S. authorities?)

I also don’t see how the US benefits from Swiss brokers withholding the additional 15% R-US. There is no case where the US gets that money, as I understand it.

As I understand, additional tax withheld was in place at least before 2001 to ensure that only Swiss residents would benefit from tax relief according to the DTA. And - where, for instance, investment funds couldn’t or wouldn’t guarantee that - thus tax may have indeed bern transferred to the IRS (3.1.1.1.2.2.1.3) and possibly refunded from the latter.

„Um eine (…) unberechtigte Inanspruchnahme der von den USA gestützt auf das Doppelbesteuerungsabkommen mit der Schweiz gewährten Entlastung von der US-Quellensteuer durch Personen zu vermeiden, die nicht in der Schweiz ansässig sind, verpflichtet Art. 11 in der bis zum 31.Dezember 2000 geltenden Fassung der Verordnung zum schweizerisch-amerikanischen Doppelbesteuerungsabkommen vom 2. Oktober 1996 die schweizerische Zwischenstelle generell, einen sog. zusätzlichen Steuerrückbehalt abzuführen.“

And the U.S. did care:

„Weil im Gegensatz zur Schweiz die meisten anderen Staaten keine mit dem zusätzlichen Steuerrückbehalt vergleichbaren Massnahmen zum Schutz vor unberechtigten Inanspruchnahmen ihres Doppelbesteuerungsabkommens mit den USA trafen, gingen dem IRS aufgrund des bis Ende 2000 geltenden US-Entlastungsverfahrens jährlich erhebliche Steuereinnahmen verloren. Dieser Umstand war einer der Hauptgründe für den Entscheid der USA, ihre Verfahrensvorschriften zu ändern.“

After the 2001 U.S. change of tax relief procedures, the „Zusätzlicher Steuerrückbehalt“ was just kept in place, but now mainly benefits the Swiss tax authorities:

„Die Verpflichtung schweizerischer Zwischenstellen zur Ablieferung eines zusätzlichen Steuerrückbehaltes wird indessen trotzdem nicht generell aufgehoben. Aufgrund des weiterhin bestehenden Bedürfnisses der schweizerischen Steuerbehörden nach Sicherung der ordnungsgemässen Versteuerung von US-Kapitalerträgen durch in der Schweiz ansässige Empfänger wird sie (…) weitergeführt (für in der Schweiz ansässige)“

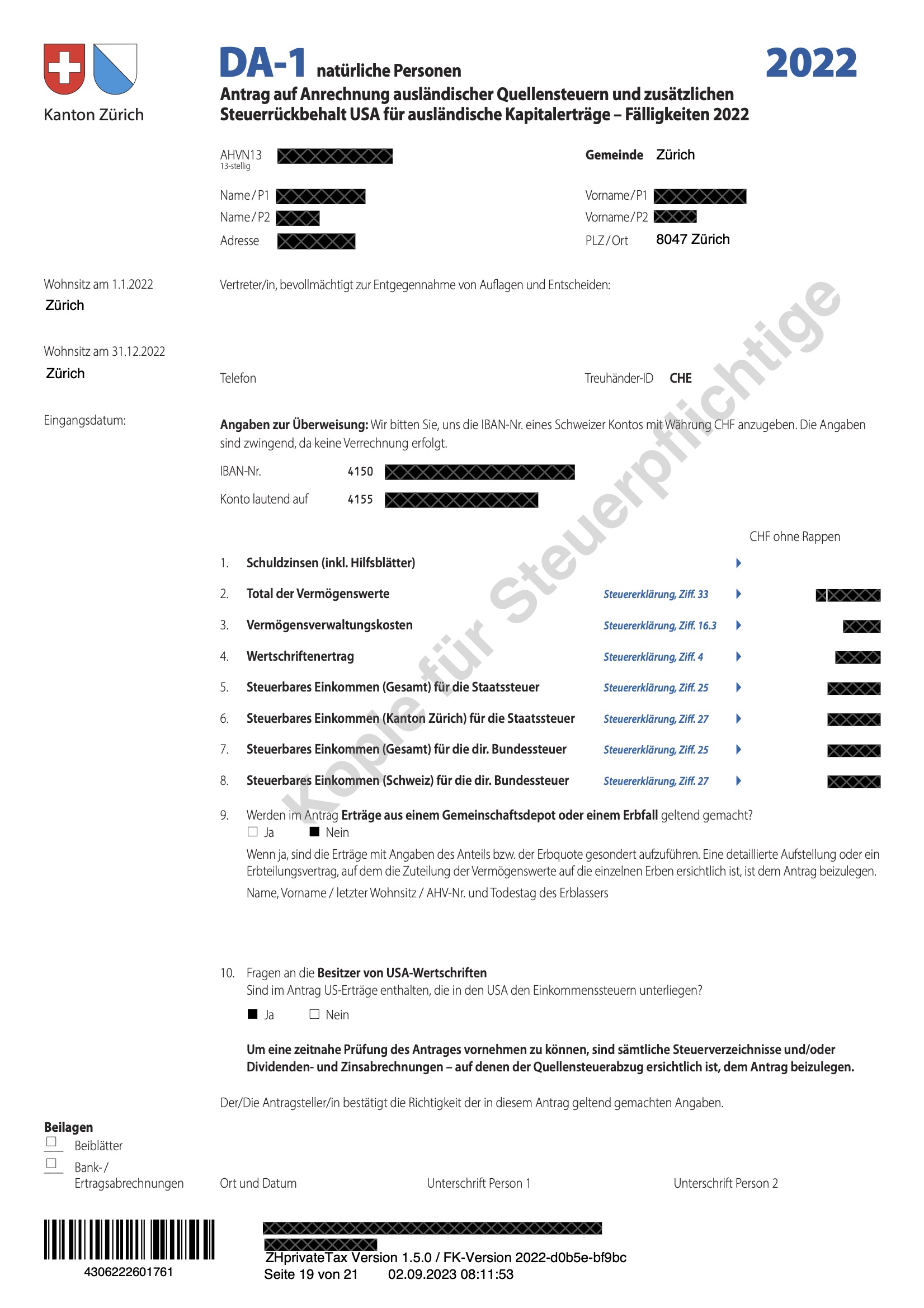

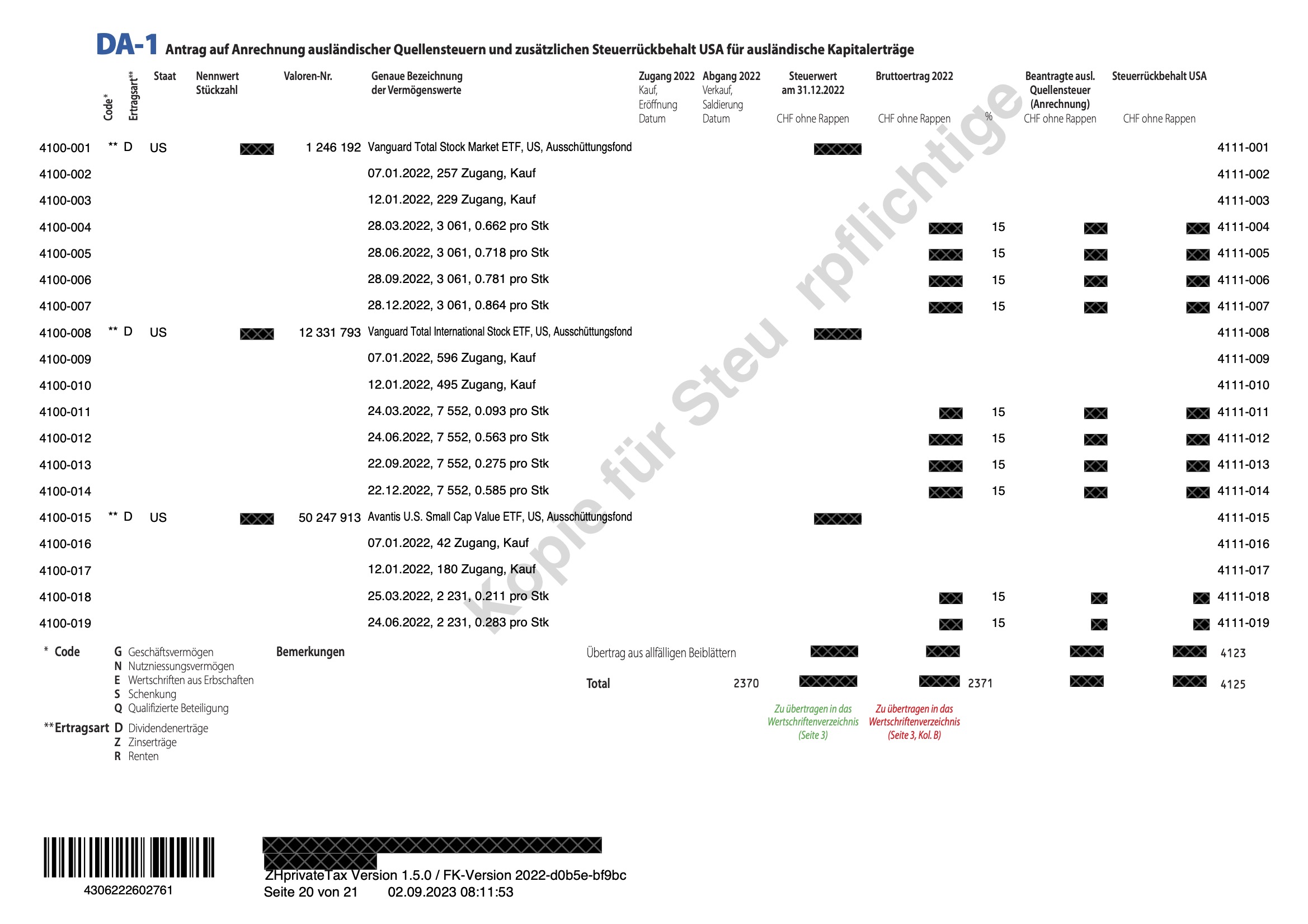

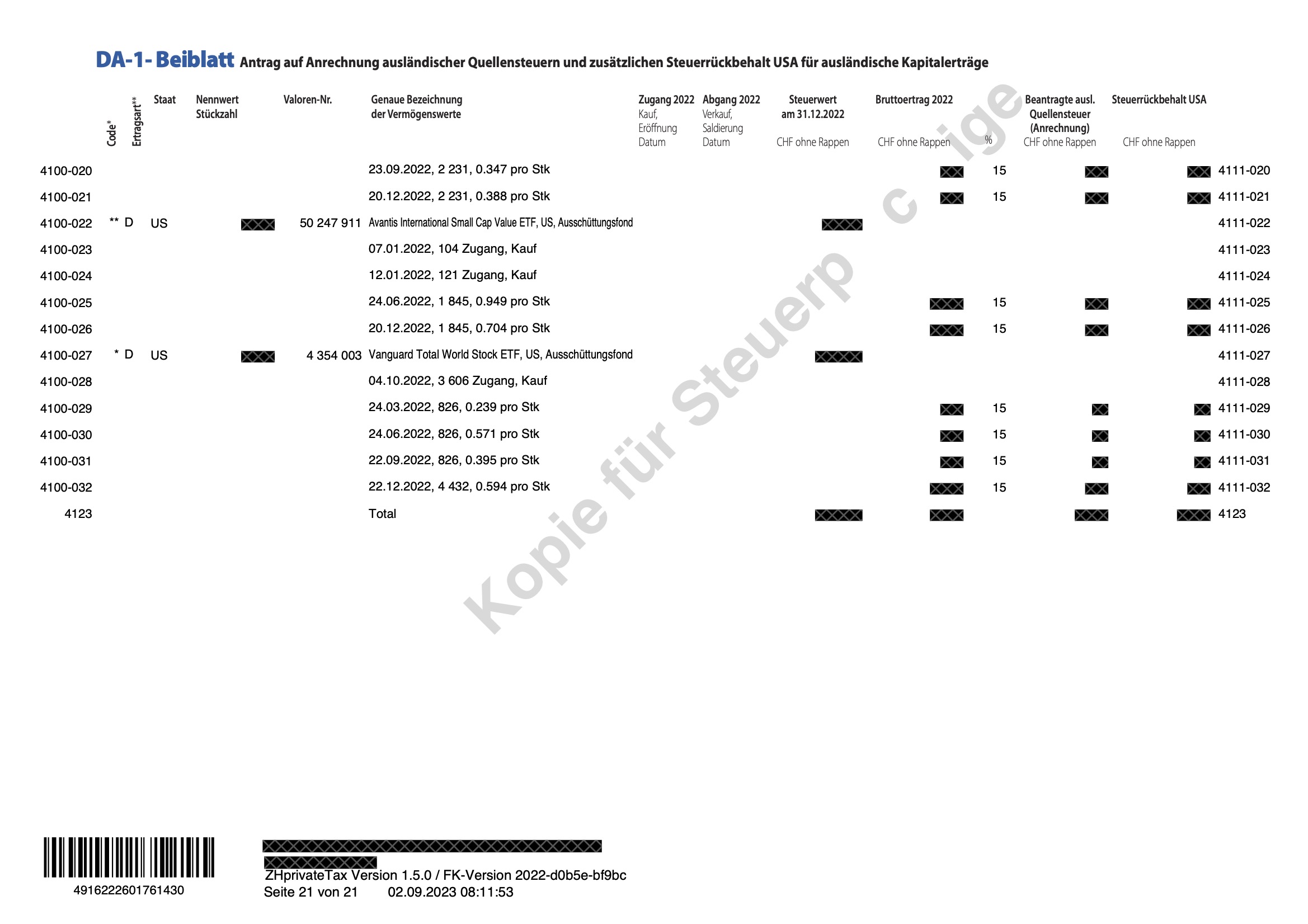

I’ve attached a redacted version of my DA-1. It looks very much like my 2021 DA-1 but of course that one could already have been wrong. Here are some of my ideas what I might have done wrong:

The first two questions:

“Werden im Antrag Erträge aus einem Gemeinschaftsdepot oder einem Erbfall geltend gemacht?” - I said “Nein”.

“Fragen an die Besitzer von USA-Wertschriften

Sind im Antrag US-Erträge enthalten, die in den USA den Einkommenssteuern unterliegen?” - I said “Ja”

I put the same amounts in both the “Beantragte ausl. Quellensteuer (Anrechnung)” and “Steuerrückbehalt USA” columns.

As I understand the question, this should be answered with ‘Nein’ unless you’re subject to US income taxes (e.g. because you’re a US person). Being subject to US WHT does not count as being subject to US income taxes. I don’t know whether/how that affects the Swiss tax return. Is it possible that US persons get the 15% US WHT back from the IRS and thus, do not get a tax credit in Switzerland?

That’s definitely wrong with a foreign broker as explained in earlier posts. You should have left the latter column empty/zero.

Based on this, it’s definitely correct that the tax authorities declined the R-US refund.

Regarding the tax credit for US WHT, I’m not sure which of these options apply:

You will get the tax credit for US WHT and the tax authorities simply didn’t make it clear that only the R-US part was declined

The tax authorities accidentally rejected the whole DA-1 instead of just the R-US part

You’re not eligible for a US WHT tax credit because you declared on the tax form that you’re subject to US income taxes

We may be able to provide further explanations if you also post the (redacted) initial rejection letter.

I think it all makes sense to me now, also the rejection letter. After reading the explanations above I re-read the rejection letter and I now believe it says that I will still get X’XXX.00 refunded in “Anrechnung ausl. Quellensteuern” but 0.00 refunded as “Steuerruckberhalt USA”.

Thanks for all the help.

Just in case I’ve followed up again with the tax authorities.

Did they „refund“ R-US (zusätzlichen Rückbehalt) without you actually being eligible for it?

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.