I have the same. Are you checking for something else then?

The general calculation (afaik) it’s CHF 1800.

It doesn’t matter the supplementary, you can keep them.

The difference it’s not huge comparing the min and the max if you go over 2500.

I calculated around CHF 500. So at the end it’s a matter of probabilities.

1 Like

I would recommend to take average of last 3 years as expected expense (unless you already know if you will have higher income spend)

Once you have the number, do the math. I don’t think basic insurance is linked to supplement in terms of deductible

1 Like

Already looking at it on Priminfo ![]()

1 Like

Anyone knows a site (or what to do a gralhp) that show the difference in costs between the various deductibles vs expenses?

It used to be that only 300 and 2500 mattered and the one you should pick changes at around 1700 chf/year.

Is it still valid?

1 Like

Still valid.

4 Likes

Here you can put in your estimated medical expenses to find the best franchiese:

4 Likes

And what’s the best franchise for children? 0, right? I have been using 600 for all these years (8) and I think it was the wrong choice.

I don’t have kids but I think they are going to the doctor way more than adults?

Oh yes, 600 chf threshold regularly surpassed

1 Like

correct, 0 franchise is best.

1 Like

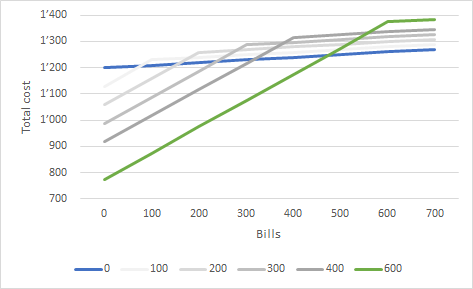

Here’s my overview, normalized to 100 / month for 0 Franchise. Here, below some 475 of bills, 600 Franchise cost least (max saving of 426 p.a.vs. 0), above its 0 Franchise (max benefit of 114 p.a. vs 600).

For younger kids with regular check-ups, vaccines and occassional other visits, 0 is the best option. For older ones, I can’t say. 600 might make sense if there are less frequent checkups and no other issues?

100 to 500 Franchise are just noise, 0 or 600 it is.

4 Likes

Slightly offtopic I found this article interesting. The guy writes about why costs rise vs. what we are told why they rise.

1 Like

I switched to 600 after they became older than 5y and there is no regular checkups/vaccinations anymore, so far so good

but of course if the kid gets sick something like twice per year (which is quite common) or you have other reasons to see a doctor more than twice per year then 600 will be spent and it is a sign to move to smaller franchise

what I am interested now is dental insurance for kids and what is included and what’s not in the basic one

I have this for kids: Zahnversicherung in der Schweiz | Vergleich – KPT, Leistungsklasse 4.

never used but it seemed pretty good and it is 9.40 CHF / month (until now…)

Here is the interactive map for the cheapest premiums in 2025. At the top right you can navigate between age groups (young/adult), inclusion/exclusion of accident cover and deductible. For each combination of those parameters, the map has 3 layers:

- “Recommendation” which gives you an advice for the cheapest premium for the next year (assuming you had already the cheapest premium in 2024). The color code works as follows:

-

Red: another insurer will offer the cheapest premium;

-

Yellow: another model (within the same insurer) will be the new cheapest option;

-

Green: the current cheapest insurer/model is the same for next year.

-

“Change of cheapest premium (YoY)” which shows how the cheapest premiums changed across the KVG-regions.

-

“Cheapest premium” which shows the cheapest premiums (absolute) across the KVG-regions.

Hovering your pointer over the municipalities displays more information in each of those maps.

Feel free to share any suggestions you may have or any mistakes you spotted.

The interactive map is available here.

13 Likes

Anyone heard of Agrisano? They are 20-30 CHF cheaper than the rest.

Has anyone tried the health insurance switcher service from AXA?

Supposedly each autumn, you can switch to the cheapest basic insurance provider with a few clicks.

Seems I get different numbers there vs. priminfo? ![]()

Never heard about it, but my best guess is that they then reach out to you to review your supplemental health insurance coverage.

Also brokers get commissions when you sign for a basic health insurance (they get even more for supplemental health insurance). This contributes to increasing the premiums, so just don’t.

3 Likes