I’ve posted before about taking a very active approach to this - i.e. I mainly invest in (high) dividend yield stocks and complement that with

Selling call options (which also ensures I don’t ‘fall in love’ with a stock and sell it at a price I am fine with + get the premiums on the options)

Selling put options (which allows me to buy stocks I want at a lower price than spot price + get the premiums on the options)

I try to balance above two out - i.e. 80% of options typically mature without being executed on anyway, but the part that does I aim to balance the cash inflows (from sold call options) out with cash outflows (from sold put options).

In addition, I’m now considering taking a Lomard loan on my stock portfolio, perhaps totalling 20% of the portfolio value, and then investing that in more high yield stocks. Interest rates are low (and tax deductable; and can presumably be fixed for 1-2 years?) and there’s plenty of stocks with fairly save dividends and relatively low share price volatility thus making it realistic to make money off the spread between interest and yield. Add on top writing call options on the shares.

Am curious if others here have experience with pursuing strategy 3 - advice? pitfalls?

Keep in mind, my objective here is not aggressive high risk growth investing, but rather driving enhanced dividend yield from my assets without much risk.

I thought about the same strategy however it highly depends on the stocks and also on the currency. For CHF the loan is cheap but there are not that many good stocks with high dividend yield. And for the USD the loan yield is relatively high and nobody know if these yields are coming down as Trumps wants them.

I’m still on the sidelines and wait for another dip to use margin (while still doing my monthly purchase via put options)

That’s a good point. Currently the Euro is relatively weak though so timing wise it may make a lot of sense to borrow in CHF now, invest in EUR high yield stocks and reinvest the dividend / option premium returns there while waiting for the EUR to recover.

Well that is true, however historically betting on a weaker CHF was not a good idea. Also the USD should get higher in theory but this way the bet is two ways; on the stock to perform well and the currency moving in the right direction. I guess I will try to go with a CHF loans on swiss stocks but will wait and try to time the market

The stock doesn’t need to perform well - as long as it remains stable that’s fine and it then keeps paying dividends and call options expire with an opportunity to rewrite.

But yeah, FX could be an issue. There’s always going to be some risk or there’ll be zero return.

I’ve looked around and there’s CHF ETF’s with low cost ratio and >4% div yield. Not really what I was having in mind (v.s. 6-7-8% div yield). Something requiring more thought.

I did pretty much this a couple years ago for a while. It worked, it did generate some extra return, but also never anything really substantial. I stopped because the few shares (CH listed & mainly CH exposure with high dividend yield) I was doing it with became too expensive, and I wasn’t happy anymore with the downside risk. Ultimately it’s a nice idea, but you really need to understand and be comfortable with you risk profile.

Edit: I did subsequently follow-up with various methods to improve my portfolio yield and/or enhance other elements like this, but recently ended up going back to good old buy and hold and nothing else.

Several years ago I had a modest Lombard loan with UBS (1 year) and it was with a fixed interest rate. I needed some cash to buy some physical assets, wasn’t used to buy stocks. Will be curious to see if this is still possible (fixed rate).

Read that interest rates may go down again tomorrow in Switzerland.

I assume Saron is also a key reference point for Lombard loans… so perhaps there is a unique ‘low interest’ opportunity coming to use leverage to enhance returns?

I do use lombard credit. There are a few pitfalls however.

You need a strong control of your money management; don’t wait for a margin call.

I found only one broker who offers fair rates which was Interactive Brokers.

I defined every detail of the strategies in advance. Your brain has more than a 100 bias that make investing a nightmare and the lombard (margin credit) makes them worse.

I live off my investments since 11 years and have a high cash flow strategy and a high risk momentum strategy in place. Both use margin. The high cash flow strategy uses margin only temporary, in bear markets and when I need to take out money (needing money is no good reason to sell a stock). The high risk momentum strategy uses margin all the times, between 130 and 300%.

BTW: I don’t like the option strategies. After many many years of small gains you may hit a big missed gain or a big loss with that strategy that wipes out years or decades of making small amounts of money.

I understand your point re Options although I take a different view.

E.g. you said elsewhere “As I said in the dividend strategy I have options because there are always enough companies to buy, companies that fulfill my criteria.”

This is one good reason why I use options - because in the div yield space there are many alternative stocks to own and writing calls helps me to not ‘fall in love’ or become complacent with a stock. It hits the target: I’m out. If I still so more growth potential, I may even immediately write a put option below the $ amount which I had to deliver for the written call. On the other side, I rarely buy stocks nowadays as I’d rather have a range of written puts out there (again, div yield strategy). By balancing those two I make sure that

a) majority of options never wind up getting executed

b) inflow from written calls (i.e. when I need to delivery the stocks) is always adequate to cover outflow from written puts

The point about “yeah, but on stock x you missed a bigger gain” is a theoretical truth because it assumes you would have held on to that stock to see that gain (which is not a given) AND it assumes if you held on to it that the gain did not evaporate afterwards.

The best thing I’ve down in a long time is work much more with writing options and use that to cycle my div yield stocks and enhance the yield.

Instead of just buy and hold and wait for dividends.

I wait for dividends AND get premiums on written calls/puts AND get more frequent ‘cash out’ premiums from executing written calls where the stocks reached my target price.

Most gains in the stock market come from more or less 5% of the companies. The chance you miss one with an option strategy is very high. But it gives you a smoother experience, probably less volatility and less performance over the long term. You can use options for the reverse of course…

You reverse your chances, instead of 5% it is 95%. And that is very good for your mind, hurts less but performs worse.

An example: I have normally 30-50 stocks in my mechanical momentum strategy. About one per year makes more than 500%. Two made more than 2000% in the 5.5 years I trade this strategy. Those single stocks are responsible for my internal interest rate (XIRR) of actually 27.4% per year since 2020 when I started the strategy.

This stocks are always complete surprises. Mostly stocks my “captain” orders me to buy against my gut instinct.

Thing is, I don’t want to rely on ‘luck’ with such multi-baggers. Sure, I’ve also been lucky on occasion and also have some money invested in potential home runs (on that note, I wish my bank allowed me to allocate individual positions to seperate portfolios - i.e. income generation vs. growth - for better tracking). My main focus now is reliable income generation used to fund my (unemployed) life so slow and smooth works just fine there.

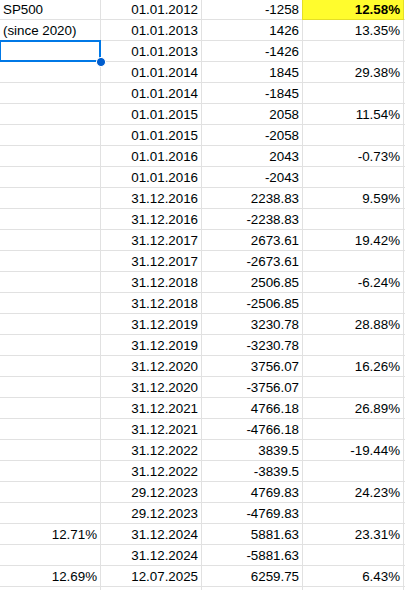

Having said that, unless I’m mistaken here, the S&P500 performance from crash in 2020 to the peak in 2025 is +180% which is roughly 35% annualized… thus beating your returns and obviously beating the long run 10% avg. Food for thought.

I’m not paying anything for writing options. I agree there is a case to be made about getting less than full potential.

Disagree with volatility and performance diminishing strategies. It may diminish performance vs. theoretical maximum but my returns are better than market average.

My bad on the S&P - should have made the effort to actually look it up rather than ask ChatGPT to do it for me!

If you really think AI can help you investing probably you should use it.

In theory option writing strategies perform better in flat markets. And you are right, you pay for what you get and you pay less than with holding stocks… at least in the currency volatility.

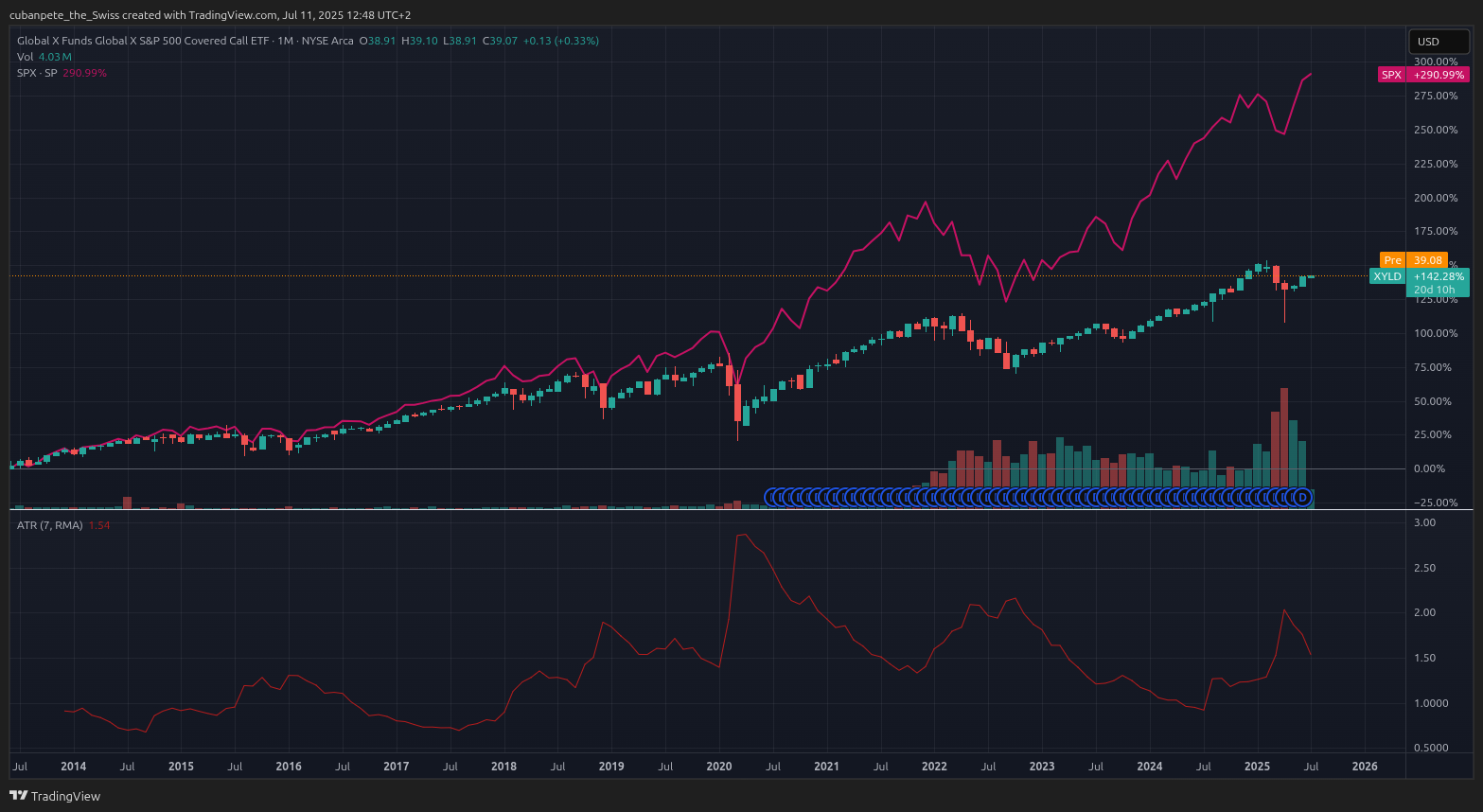

Now, you must have an edge way better than mean because you have to compare your strategy with ETF that do the same. Here is one, even including reinvested dividends it loses big against the SP500.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.