I recently read the very much praised book by Gerd Kommer called “Souverän investieren mit Indexfonds und ETFs: Wie Privatanleger das Spiel gegen die Finanzbranche gewinnen”. For me as a beginner in investing it all seems very convincing.

Can any of you experienced investors please comment on the book’s usefulness in terms of building a real portfolio? For those who didn’t read it, the main idea is that you build a “World portfolio” out of ETFs with

55% of developed markets (North America, Europe, Pacific) with some small accents on value stocks and small caps (about 10% each within these 55%),

25% emerging markets large and mid caps,

10% global real estate ETFs

10% commodity futures.

If you don’t have much money to invest, he writes, then just one ETF on MSCI ACWI or two ETFs: 75% MSCI World and 25% MSCI Emerging Markets would be enough. Does is all make sense?

I’ve been staying in the information bubble of this book for a while now (reading other books and blogs he recommends, like zendepot.de and finanzwesir.com) and I wonder if I’m not missing something important, that’s beyond the bubble.

Hey Knoch,

i also read that book. it was my first reading on my journey to index investment, and i was the basis of my today’s investments.

In the big picture almost everything in there is reasonable, and by the 80/20 mentality (achieve 80 % of possible investment success by soending 20% of the ultimate read up effort // not to confuse with “80/20” in portfolio design), it is everything you need. It will put you ahead of 99% of private investors.

without knowing your situation and your goals, nobody can give you more advice that this is a well diversified agressive portfolio (90% stocks). for long term returns, re-consider the commodities part. for less volatility, consider less volatile assets like cash and bonds (the latter having no big fans around here)

from the practical point of view, check out vanguard ETFs. for stocks, i made a nice ETF choice help

In the book he is actually talking about the “risk-free” and risky parts of the portfolio. The percentage of these parts (80/20 or whatever) can vary depending on your personal risk profile. However he recommends that you stick to the mentioned distribution of assets (he stresses the yearly rebalancing as well) in the risky part as it is optimised for maximal returns.

Concerning the real estate and commodities he writes that they make sense because they do not correlate with the rest of the portfolio, which would thus reduce the risk without really loosing the return.

Concerning bonds, he recommends that you have short-term (1-3 years) government bonds in your currency (CHF in our case). These together with cash would constitute your “risk-free” part of the portfolio. I guess you could count the non-stocks based 3 pillar accounts to the “risk-free” part as well.

I wouldn’t invest in commodity and REIT. Otherwise, the portfolio makes total sense.

If you don’t have much money to invest, he writes, then just one ETF on MSCI ACWI or two ETFs: 75% MSCI World and 25% MSCI Emerging Markets would be enough.

→ this limit doesn’t make a lot of sense if the buying costs are low like on IB

and don’t forget to check the index tracks by the ETFs you will chose. The name of the index can be misleading (for exemple: MSCI world doesn’t track Emerging markets)

this is only partially true: if you want to fully optimize for expected returns, you will pick a stock only portfolio with bias towards small, value and emerging markets stocks (according to the modern portfolio theory) (I did that to some extent). BUT, mixing in a bit of commodities, real estate and bonds can reduce volatility by a lot and only marginally reduced expected returns. no free lunch between risk & return! check out the great portfolio finder and mind the efficient frontier graph.

this “risk-free” part currently (refferring to the Niedrigzinsumfeld" will give you returns of about -0.7%, i.e. negative returns. that is why people on this forum agreed to preferring cash over bonds, at least until their yield is positive again.

yes, the purchase of a few hundred francs of ETFs cost around $0.3, which is virtually nothing. the only reason to limit the number of ETFs is to reduce complexity, which is a reasonable wish. Out of experience I can tell that (passively) managing my 6-ETF portfolio is really simple

You should add a disclaimer “in my opinion” in front of that statement. You’re saying that the market is underestimating the small caps and emerging markets in the long run. But why is it doing that? Maybe it has something to do with, as you said, volatility. Could you convince me why we should have that bias? Not just with past numbers, but with logic.

It is a conclusion of modern portfolio theory: There is the (more or less plausible) assumption that an stock A that has higher volatility than stock B should have a higher long term return than stock B. If stock A had a higher volatility but just the same retuns as stock B, no investor would buy it.

Historically a positive risk premium for each small, value and emerging markets is found. no guarantee for future returns…

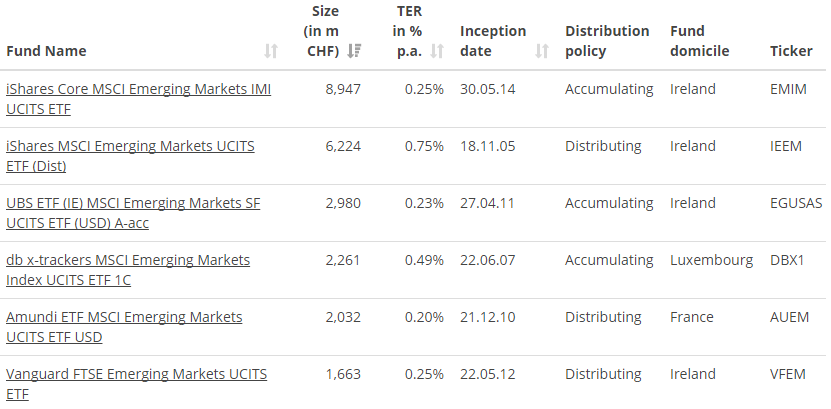

[edit] thinking about this i dound the MSCI EM small Index has a few IE-dimiciled ETFs that track it: http://www.etf.com/equity_emerging_markets_small_cap

however they are not cheap with TERs around 0.5-0.7%. i might open a new thread for this, as it is derailing OP’s questions

OK that sounds logical to me. So the current price levels are the effect of market forces striking a balance between expected return and volatility. I guess you could try to plot a curve between volatility and the average expected return. Maybe it would be linear, maybe not. But this curve would represent the propensity to risk of the whole market.

So what you’re suggesting is to be more risk tolerant than the average of the market. But why not go all the way? Why not invest only in small caps and emerging markets? They should yield the biggest returns in the long run, right?

I have another explanation, at least for small value caps.

No institutional investor goes for true small caps. if you are a fund manager with 10 billions to invest, 1% of your portfolio is 100 million USD. Therefore, you will totally ignore small companies with market cap inferior or equal to 100 Million USD, else, your stake in this company would have too big of an impact on the price of the stock.

Therefore, it is my experience that market are much less efficient in small caps.

Using a fishing analogy, if you were a retail fisherman, would you go fishing where the trawler fish boats are, with their industrial nets? Or would you go where they cannot go due to their size, and get some fish?

qualitiatively scientists agree that each additional portion expected return costs an increasing amount of volatility (or risk). so no, it is not linear.

That would be very consistent. you would end up with that single most risky stock available deep in the jungle of EM small value stocks. Then you have the highest expected return, the highest risk, and no diversification. and here i decided to not trade in the diversification of a world portfolio. it would go too far now to point out why you want diversification here

also i like julianek’s point of fishes^^

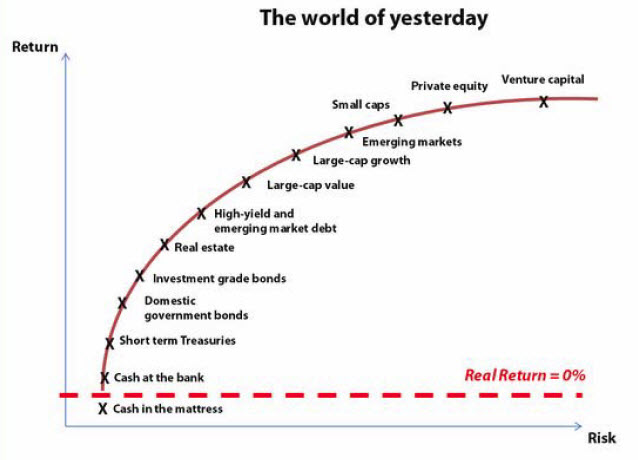

That is a very cool chart! Exactly what I had in mind. So, first thing that comes into my mind is that it ranks growth stocks as more risky than value, thus, one would assume, more up your alley. Yet you recommend value?

Anyway, one might argue, that including too many small caps and emerging markets brings you a lot of risk for not so much more return.

That’s a good point. However, are small caps not what venture capital is investing in? And they are not guys with small wallets. I agree with your conclusion that small caps are less efficient, but that’s not necessarily a good thing when you buy a whole-market small cap ETF.

If I was a smart fisherman and I knew where to fish, I could probably find some small fish that the trawlers didn’t bother to catch. But for this I would need to actively bet on particular areas. An ETF is not like that.

It’s why am thinking about. Currently, my portfolio is 50% EM and will put more USA Value.

Yes, on the long rung the yield will be bigger. But the term “long run” also depends of your time horizon. Are you ready to wait XX year to see the bigger return?

The downside is that cost to own small-cap might be more expensive. You will need to check if the return after cost worth it.

For exemple:

-MSCI emerging market in the last 10 year has a return of: 1.68% by year. To track this index, the cost is around 0.25% + small/medium spread (around 0.2%)

-MSCI emerging market Small cap in the last 10 year has a return of: 2.78% by year. To track this index the cost around 0.74% (iShares MSCI Emerging Markets Small Cap UCITS ETF) + a big spread (around 1% on the SIX).

The spread applies only when you buy or sell the share. At the end the difference is not so big after cost.

I think it’s a bad idea to buy EM etf on the US market due to the withholding tax.

… and they usually buy the whole or a big fraction of the company, getting involved or overtaking management altogether. other than the tiny pieces passive investors buy

One thing Gerd Kommer advocates for is using a GDP-weighted portfolio and not a market cap weighted portfolio. The reasoning being better historical and expected future performance, because a market-capped portfolio already invests in the “winners” so kind of like a bubble.

His 70/30 World EM Portfolio incorprated the GDP weighted approach. Another approach would be ~50World/20EU/30EM

However he uses the MSCI index for World and EM, we here like Vanguard and the FTSE index. If I were to recreate the 70/30 Portfolio with FTSE indexes would much change? I’m guessing less EM because South Korea isn’t in the EM index but world.

What are your opinions on this? In germany the GDP route seems to be preferred, here I don’t see it so much.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.