As per subject, I’m in the negotiation phase for a job position full remote for a US based company. And their offer is in… USD.

Now, I’m clearly skeptical on having a “floating salary”, I don’t think I should bear the risk of currency fluctuation, it should be on their side. If you are US company and want to start hiring in Europe in general, you can’t expect people to get a salary in dollars I believe.

Does any of you have had similar experience? Is this normal? Any advice?

Thanks

If they’re a business in the US and they earn in USD and have some work to delegate, then of course it’s the most convenient to also have it billed in USD. They don’t care where you live or what your expenses are, they just want the cheapest/easiest way to have it done. There is no should or shouldn’t. If you’re willing to accept the exchange rate risk, the better for them.

And why wouldn’t you accept it? Unless you spend over 60% of your income, it shouldn’t put you under pressure. And sure, you should expect a little USD premium over a CHF salary, for the risk that you have to bear. But intuition tells me this risk should be worth it.

You would have to work as ANobAG, which means the ball for paying Swiss social security will rest in your court. You pay the contribution for the child benefits scheme and the compensation office’s administrative fee, which are both normally covered by your employer. If you want to use the pillar 2, you will pretty much be limited to the Substitute Occupational Benefits Institution, with you covering the full contributions, but pillar 3a might make more sense in this case. You will have to get accident insurance from your health insurance and get private loss-of-income insurance if you want to match the accident insurance you get through Swiss employers.

It’s pretty standard for US and even Asian companies to pay salaries in US$, with you carrying the currency risk. I did this for some time.

You can’t really claim anything from your US employer from a legal perspective - not even paid vacation or sick leave. Your US employer is not subject to Swiss law. But of course you could negotiate paid holidays, a private pension fund and compensation for your Swiss social security contributions, etc.

Ultimately it all comes down to gross and net salaries. If you can cover all your bases and still come out with more, then why not?

I’ve been in the same situation and worked with a payroll company based in Switzerland (there are quite a few) to serve as an intermediate entity between me and the US company. This is convenient because you become the employee of the Swiss payroll company with all the benefits that it entails. A very simple solution for a somewhat complex problem but of course this is not a free service. Some companies may accept to cover this extra cost. Feel free to send me a PM if you want more details.

Coming back to your original question, from my experience, it seems common for US companies without offices in Europe to pay in USD.

indeed this is a valid point. Luckily i’m actually on the saving side, roughly ~55-60%, so as you said it shouldn’t concern too much.

Yes, that will be my case too. So I will be officially employed by this intermediate company, so to get all benefits of a CH contract (pillar 2a, accident insurance, etc.), which is also good as they will bare the conversions fee, and the CHF amount will be the conversion rate at the time of monthly payment.

Not sure that’s good, it could also be you’re losing 1% of your salary compared to being paid in USD. (I somehow doubt they care much about avoid conversion fees). Same for other things, if you were working as ANobAG maybe you’d be able to use VIAC as pillar2 instead of a pension fund which doesn’t suits your needs (somehow based on @MrRIP experience I don’t think those payroll providers have super nice pension funds…)

A “problem”? A “problem” I’d love to have… since about 2006 they have been laughing to the bank and have had an exchange rate related raise alone of about 50% compared to their peers in for eg Germany stuck on a constant euro salary.

While we Swiss have had a decade of annual appraisals ending with “sorry we can only give you a raise of 1% (if lucky) since the CHF is so strong & we have problems remaining competitive bla bla”, the German and other Grenzgänger have been getting raises of about 5% annually, sometimes 20% all at once. for everyone, I’d say.

A payroll company can work better than ANobAG if you want convenience, but your US employer will obviously be thinking gross, so ultimately it will be you paying for the extra service. The Swiss social security benefits will obviously still be paid in full from your gross salary. The biggest possible benefit would be that you could participate in a Swiss pension fund which has better conditions than the Substitute Occupational Benefit Institution.

Managing things on your own as ANobAG is a pretty small time investment, from my experience. One issue I experienced as ANobAG earning a foreign-currency salary is that in some years my actual income exceeded my CHF stated income (you have to give an income in CHF to the social security office) due to currency fluctuations in my favor. This resulted in my getting some AHV/IV bills for the difference in arrears up to 4 years later based on my actual income as per tax results. Just something you have to be prepared for. I suppose the opposite (refunds from the AHV) could also apply, but I have no experience with that.

Hey there… it’s me again with an update and looking for your opinion on an alternative I thought about.

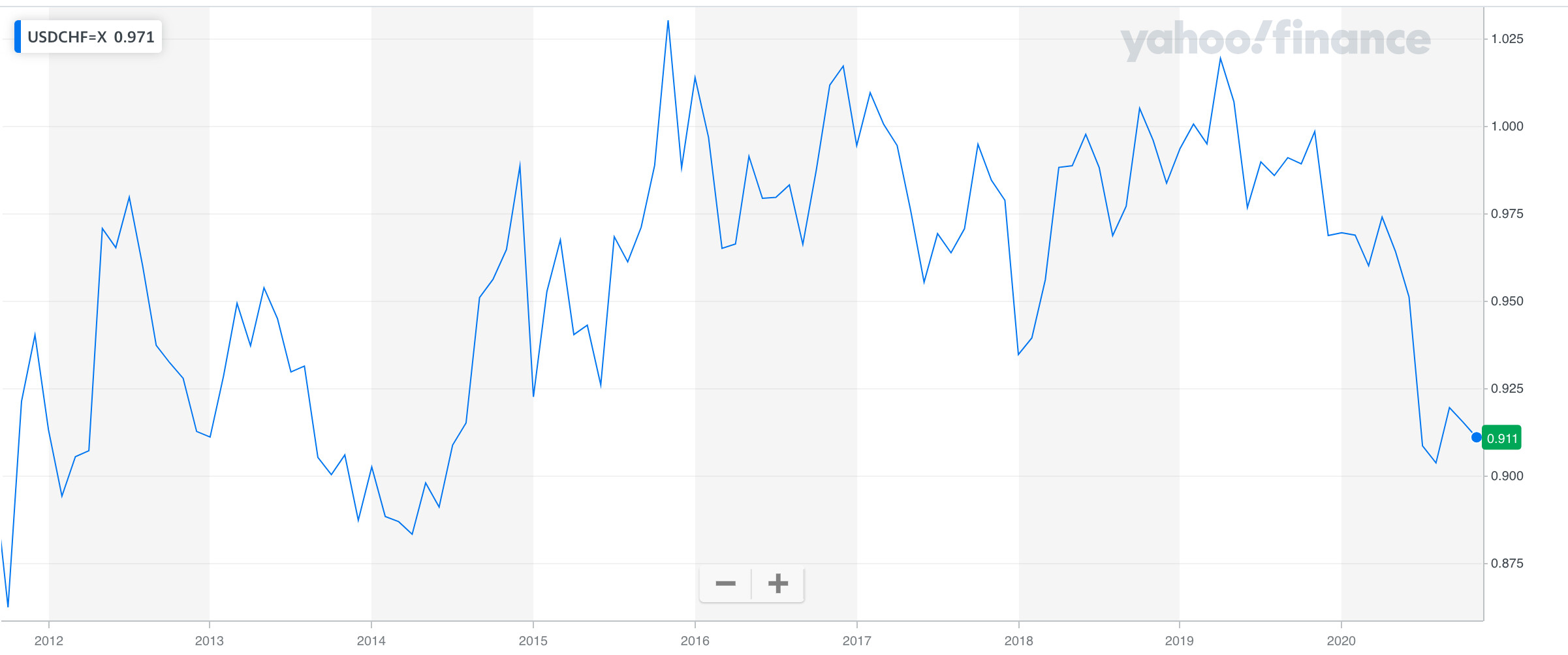

Let’s use a round number to make it easy, let’s say the US company salary offer is 100k USD/year (gross). The proxy EU company, who will provide me with a local CH contract, made a bulk conversion on the date they signed the agreement and is proposing me a contract in CHF, for about 92k CHF/year, so using a USD.CHF conversion rate of 0,92. This is slightly better than today’s rate (0.91) but in general not that great considering that pre-covid and with the Fed not printing money all day long, the two currency have historically been (at least the last ~10y) very close to 1:1

I was expecting a month-by-month conversion rate instead of a bulk one. so here my questions to you about the possible options I could have:

Keep the agreement as it is, so with the USD salary fully converted already at 0,92

PRO: this would give me a peace of mind, not having to worry how the FX market will go every month

CONS: I know, past performance etc etc… but the 0,92 rate is extremely unfavourable I think. Sure it can happen some months may be even lower, much lower, but not sure on the long run

Ask for having it converted on a month-by-month base (or at least no longer than every six months)

PROS/CONS: can help mitigate the current 0,92 bad rate, but can add a risk if in 6months the rate will be lower

Open a USD account here in Switzerland and ask to have it wired monthly in USD.

PRO: I can choose if, how much and when to convert my money, or directly invest most of them in US ETFs so avoiding exchange costs

CONS: the exchange fees will be on me and my exposure to USD will be super high in the long run, which can add significant stress

About #3 I’m not even sure it is entirely possible under Swiss law, but before asking I wanted to gather some opinion here, also because I have really very few knowledge on FX and monetary policies.

I highly doubt that any company would do monthly adjusted conversion rates. Would be extremly complicated for the payrolling provider as many contributions are depending on the yearly base salery.

These below are the last 10y, it has been going up and down but definitely closer to an avg 0,97, hence my comment. Not saying you are wrong that it won’t go up, as I wrote I don’t know much about FX/monetary policies. But until 2020/covid, it doesn’t look to me it was dropping 0.9%/year at all

Thanks for the extra context, very useful.

So basically it was a sort of artificial rate, like the 1.20 with the Euro the ended ~5years ago. Good to know.

I’m in the same boat right now. May I ask if your employer was based in the EU/UK, or abroad? In my case the employer is based in the US and I want to clarify how to go about the accident insurance. I have contacted the Ersatzkasse UVG, but given that the person who answered my request for attribution to an insurance company seemed not have not read a single word from my email, I want to make sure I understand what it is I need before starting to make more formal and explicit requests.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.