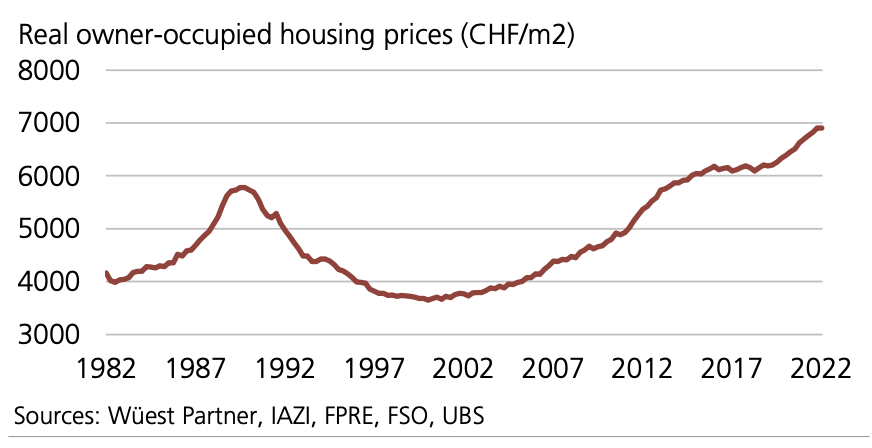

The last time we had “high” prices in 1990, it took 10 years to reach the bottom. And you would think going from 6000 to 4000 per sqm was a solid reduction, 33%! But when I told this to my boss, who is a ca. 55 y.o. Swiss, and who bought his house at that time, and who works in real estate, he said that he does not recall any such dip in prices. He said “maybe it was 10%”. Of course, he just might be wrong.

But applying this historical data to our current situation, if the dips start soon, how long it will take and what level do you expect it will reach? Do you think the prices can go down by 30%? Or just 10%? If 10%, then we’re just gonna go back less than 1 year, which would mean the wait was pointless.

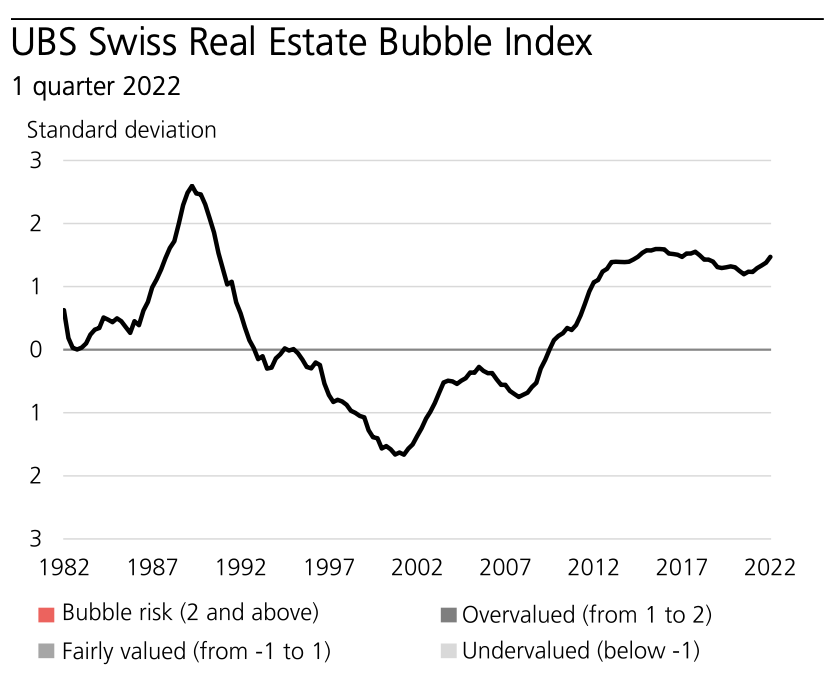

And if we look at the total UBS bubble index, which includes other factors than just price, we can see that according to them we’re only in the “overpriced” range.

Don’t get me wrong, I’m super frustrated about not being able to afford real estate. Intuitively, it seems wrong that it costs so much that most people have to take huge loans to afford it. I’m just not too optimistic about the price drops or the speed at which it could happen. We would need to see some major shitshow of unforeseen scale in order to witness a crash in prices by 50% or more. And honestly, only then could I afford any of the Swiss real estate with clear conscience. Otherwise it just seems like a leveraged bet on the prosperity of the country for the next 30+ years.

As with everything in CH probably depends a lot on the canton.

In and around ZH we might not see any significant drops.

But elsewhere it might have already started to happen (I overheard some people chatting about Davos and such - probably also not low demand area, but apparently feeling it).

Geneva and Zurich would be high-risk. Ticino not. Although when I look for real estate in Ticino, I don’t get the impression like it’s cheap. Cheap real estate in Ticino looks really crappy and nice ones are scarce and much more expensive.

It is helpful to look at the data underlying the UBS bubble index, which is a made up composite

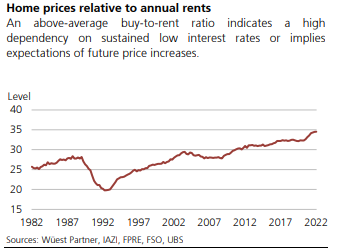

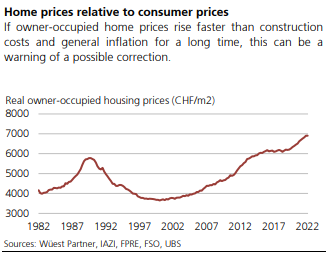

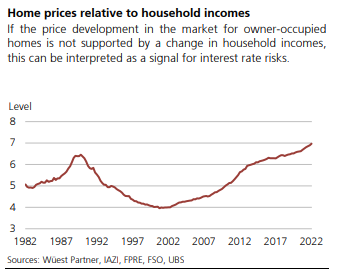

The 3 charts below support the view that things took off with introduction of low / negative interest rate circa 2009.

Even if the population and demand keep growing, at a certain point the current prices just stop being affordable.

Example: our friends nearly pulled out of a 2M purchase when the 10 year rate went to 1.2% as it blew their monthly budget. They would never have bought at 3% (interest cost on 80% loan becomes 4k /month instead of 1.6k)

The regional analysis is based on how the local price-to-rent ratio has changed over the past five years. Regions where this ratio experienced a disproportionately sharp rise have an increased correction risk.

I guess then realty prices went up more than rents. Although whenever I look for some attractive flats to rent, I tend to find places which cost 4’000 CHF or more. So not sure about rents being in check. Maybe for the low standard flats. But the attractive ones are in high demand, I guess.

I think prices in Lugano are in the same bubble as those in Zurich.

I wonder if they decided to work on such a large scale that they “didn’t bother” to show small dots of red here and there.

Or something more malicious. It reminds me the website of a health insurance that conveniently skip Ticino as a non-risk region, only on the italian version of that page. Coincidence?

around back to 2019 levels, where the sqm-prices skyrocketed from 6000 to 7000 CHF in 0 years, at near-0% inflation. This was all because of the negative interest rate was introduced in 2015 + 3yrs pickup on the housing market - or I can expect them to just stall like it did 2015-2019.

On a long-term average, a yearly 2% appreciation would be in order. We are way above that currently.

Friends who bought something in Affoltern am Albis for 850 four years ago are now selling it for 1.1M. That’s just not reasonable. But I might just be wishful Anyhow, the 3% 10-yr kills all options anyway.

Wow that is a really nice return on investment ( which your house should not be viewed as), they lived there for a few years for free and made money. Incredible.

Those were good times from 2008 onwards

@Bojack you will buy something! The right thing will appear at some point in the future

Today I was wondering why increasing interest rates have less impact in RE prices in Switzerland. Especially compared to other countries like Germany.

I think not having to pay back the mortgage is a huge factor. Lets take us for example. We bought an apartment for 770k with a 700k mortgage and our amortization is done by our 3rd pillar contributions. So this 700k mortgage will stay as it is for a very long time. If we assume 9k/year for Unterhalt/Nebenkosten, the only question that matters is: at what interest rate will it be more expensive than renting the same apartment (after taxes)?

You could rent our apartment for 2.4k/month or ~29k/year. That leaves 20k/year for interest with the numbers above. The Eigenmietwert is 13.4k (after the 20% “Pauschal” deduction) and marginal tax rate is 25%. So if we pay 22k/year in interest, it will be as expensive as renting it. With a 700k mortgage that’s 3.14%/year. As we have a Saron mortgage the SNB would have to increase its rate up to 2.5-2.75%.

So why should the value of our apartment drop as long as the SNB rate is still below 2.5%?

(P.s. I’m aware that I ignored all opportunity costs, but being 11x leveraged means that you just need 0.5-0.7%/year yield in RE to match stocks longterm)

Did you deduct NK on this figure ? 2.4 k/month net seems on the high side for Aargau (I was visiting super luxurious flats with elevator going into the flat at lower brutto rents than that)

What I see is that suddenly, immo ads are even appearing on youtube, so I guess there is some trouble to sell houses in a timely matter in B-towns.

An article appeared recently that for the first time in Germany, RE prices dropped slightly, also in A-towns.

Not sure how relevant though and if it is a real trend.

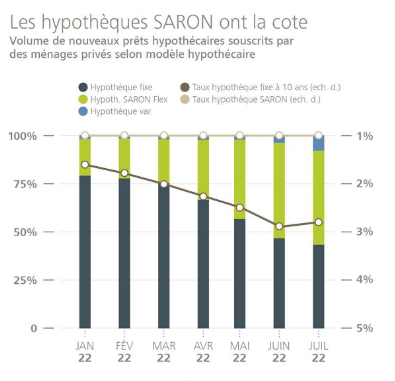

Raiffeisen’s quarterly update on the Swiss property market usually provides some interesting insights (although not a neutral viewpoint due to being a mortgage lender).

According to their Q3 2022 update owner-occupied property prices have been completely unaffected by the increase in rates because people are switching to SARON mortgages:

What shocked me a little is how strongly Raiffeisen call out the benefits of SARON mortgages vs. 10 year fixed rate on the basis that SARON almost always guarantees lower interest costs

SARON makes sense for financially secure borrowers who can afford the risk but it is a big doubt for me whether this “subtle” point will make its way to staff in branches or less financially savvy borrowers

Raiffeisen’s economist shares his view that people taking SARON mortgages don’t have to worry because the increase in SARON rates is not expected to be immediate and in addition everyone has been stress tested based on 5% rates and these seem a long way off

We have seen this in Eastern-Europe (mostly in Hungary) through the early 2000’s, when people started taking variable rate loans denominated in CHF as the CHF interests were less then half of that of the local currencies.

And OF COURSE you read the fine print. OF COURSE they told you. Nevertheless, the whole country started to take out CHF loans as they have been massively cheaper. You also made a comparison on the CHF-HUF ATH in the last 10 years to see the upper side of the risks. It was still cheaper.

Then 2-3 yrs later, the CHF-HUF rate exploded from 150 to 250 (today: 400) and boom everyone went bust and the state needed to bail out the people.

It’s not the same story, but I have a strong dejá vu.

Theoretically people would withstand a 5% rate. But noone actually expects a 5% rate, but everyone kind of hopes it stays under 2%. I wonder what would actually happen around 3.5-4% SARON.

Personally I like SARON mortgages. Even though I have not analyzed time series data, my expectation would be that SARON over a long horizon beats fixed-term mortgages. The yield curve is usually upward sloping so that long-term funding on average needs to pay a premium. This is usually also reflected in swap rates. Also the refinancing risk is much better “spread” across time with a SARON mortgage. This is in particular relevant for a country like CH where amortization is very limited, ie, even mortgages with very long terms are ultimately refinanced to a large extent.

As one exception: if rates are strongly negative the advantage of SARON diminishes as banks floor SARON mortgages (prior to applying the margin) at 0%.

But indeed one needs to be able to cope with a variable budget…

Not sure whether prices are starting to go down, but my email alerts for houses around Zurich started to trigger much more often in the last few months.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.