The vice chairman of the Swiss central bank recently said in a speech that (quote) “between 20 and 30 percent of newly granted mortgages would no longer be sustainable if interest rates rise by 3 percentage points.” See also the link below.

To my understanding, banks calculate with a potential interest rate between 5-6% when granting a mortgage. So why would an increase of 3% be a problem? The only reason that I can think of is this: Mortgages must be reduced to 65% of the real estate price within 15 years, so if interest rates go up and prices go down, people would be in trouble.

Are those 5% calculated for everyone, or do professional investors receive different conditions? I could imagine that professional investors with a rather large real estate portfolio might be treated differently in terms of potential interest rate.

Plus banks might get more creative with the loans and negative interest rates nowadays. I can’t say for Swiss banks, but I know German banks are doing it already for a while. So yes, while officially they have to consider potential interest rates, there are ways to trick the system. And if the quotes for the quarter are not looking well, managers are also approving mortgages who would not qualify (speaking strictly about Germany in the last two sentences)

I woud also like to understand the SNB’s underlying analysis.

My thoughts:

3% increase would take us from ~1% mortgage rate today to ~4%. This is virtually at the 5% stress test rate. As the affordability calc is not a precise science, I would assume it is not binary that once we cross 5% people start to get into problems and lower than that everyone is ok. There must be a continuum and issues start before 5%

The stress test assumes no more than 1/3 of income should go on housing cost, this is a rule of thumb and some people may not have 1/3 of income available for housing

People’s situation may have changed since taking out the loan e.g. lost job during Covid

A rate of 4% is a 400% increase in interest costs vs. today, it could lead to house values decreasing and owner’s equity decreasing or negative equity. When renewing loans the banks may ask owners to stump up more equity or increase amortisation. If buyers stretched their finances to make the initial downpayment and perhaps already withdrew their 2 pillar it might be tricky to stump up more equity

I can confirm that over 50% of my clients wouldn’t be able to pay 3-4% interest per year. It doesn’t matter that banks are calculating with 5% when people are living beyond their means.

~65% of all people above 18 are saving less than 500 CHF per month, most of them basically zero.

This is a cool insight I got while working in Banking (in Portugal that is, no experience in Switzerland). Almost everyone was living pay check to pay check (income didn’t matter) and around 10-15% were going negative every single month, paying 15% interest on the borrowed about

I was discussing this with a fellow mustachian friend, how do people spent so much in Switzerland?

Your spending just continues to grow as your income grows?

The reasonable thing would be to think “Cool, I’m paying 1% instead of 5% interest, I should save/invest those 4%”. But usually it ends up being “Cool, interest rates are so low, now I can lease a 2nd Mercedes C-class”.

I wouldn’t say “lol” when referring to a negative savings rate…

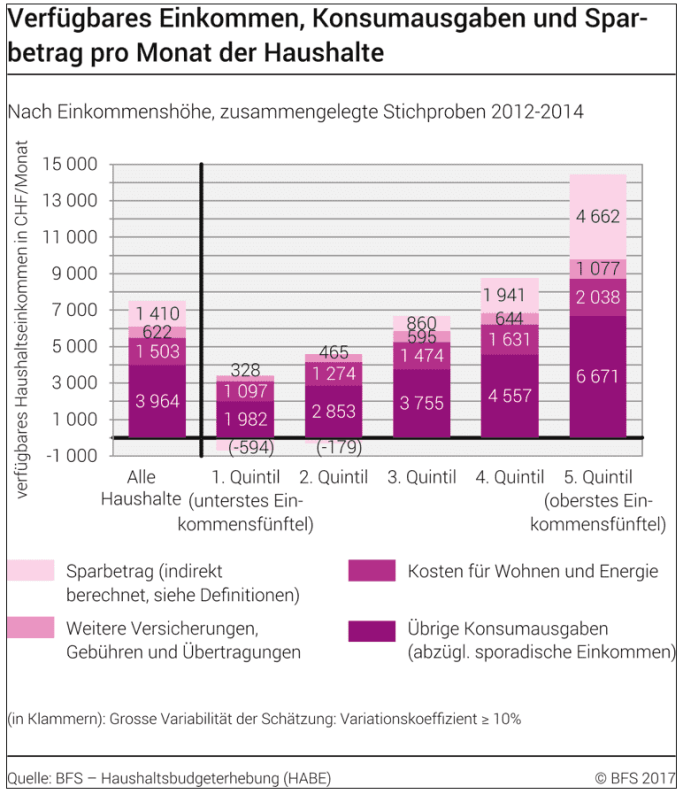

Quintil has CHF 3’407.- total household income, 2. Quintil CHF 4’592.- That is probably enough for one person, but imagine two people or even a family with kids.

Saving isn’t about how much you are earning, rather how much you are spending. Making kids = spending more money. So if you have a negative savings rate due do kids, why did you make them in the first place? This is controversial and sligthly offtopic anyway.

If a bank knows that their clients might have issues later this/next year, maybe they should inform their client to check their expenses. If the bank’s business plan is 90% lending money and 60% of its customers default, it’s not good news.

Maybe those 60% that will have issues need only to give back the 2nd car and stop paying expensive stuff in order to go back to a safe budget.

isn’t as well because an increase of interest rates makes the home value go down? Many may then need not only to pay 3 % of interest, but to add considerable capital to compensate for the value difference.

To come back to the topic: Most of those that couldn’t afford interest rates at 3-4% are probably already retired. The others are just spending too much.

First group will be in trouble, second group will be forced to rethink their spending behaviour.

I can absolutely confirm this behaviour within my friends, many of whom are expats working with Pharma/Finance/Banks in Switzerland.

Case in point: A couple earns approx. 25 KCHF per month net (after deduction of Pillar 1, Pillar 2, Health Insurance, IV, etc. but not taxes).

Their monthly savings is 5 KCHF.

Typical of their monthly expenses are: 1) 5.5 Apartment in Basel Stadt at 4.2 KCHF 2) Full-time Kita at 3.3 KCHF (even though they are not using the service) 3) paying for a nanny at 3.2 KCHF 4) lowest deductible health insurances at 1.5 KCHF 5) Full Batmaid service at approx. 1.2 KCHF, etc.

They recently bought a brand new hybrid SUV at 54 KCHF.

I brought up the FIRE philosophy with them a few months ago and they were totally dismissive of that idea, calling it unachievable.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.