IT might go to 2% by June According to this. On the other hand, things are starting to break in the US small banking system starting with SVB and the contagion see this one let’s see how that is handled in the US and if it affects the FED’s decision in march.

interesting times…

(Added) People lining-up to get their money let’s see what happens tomorrow.

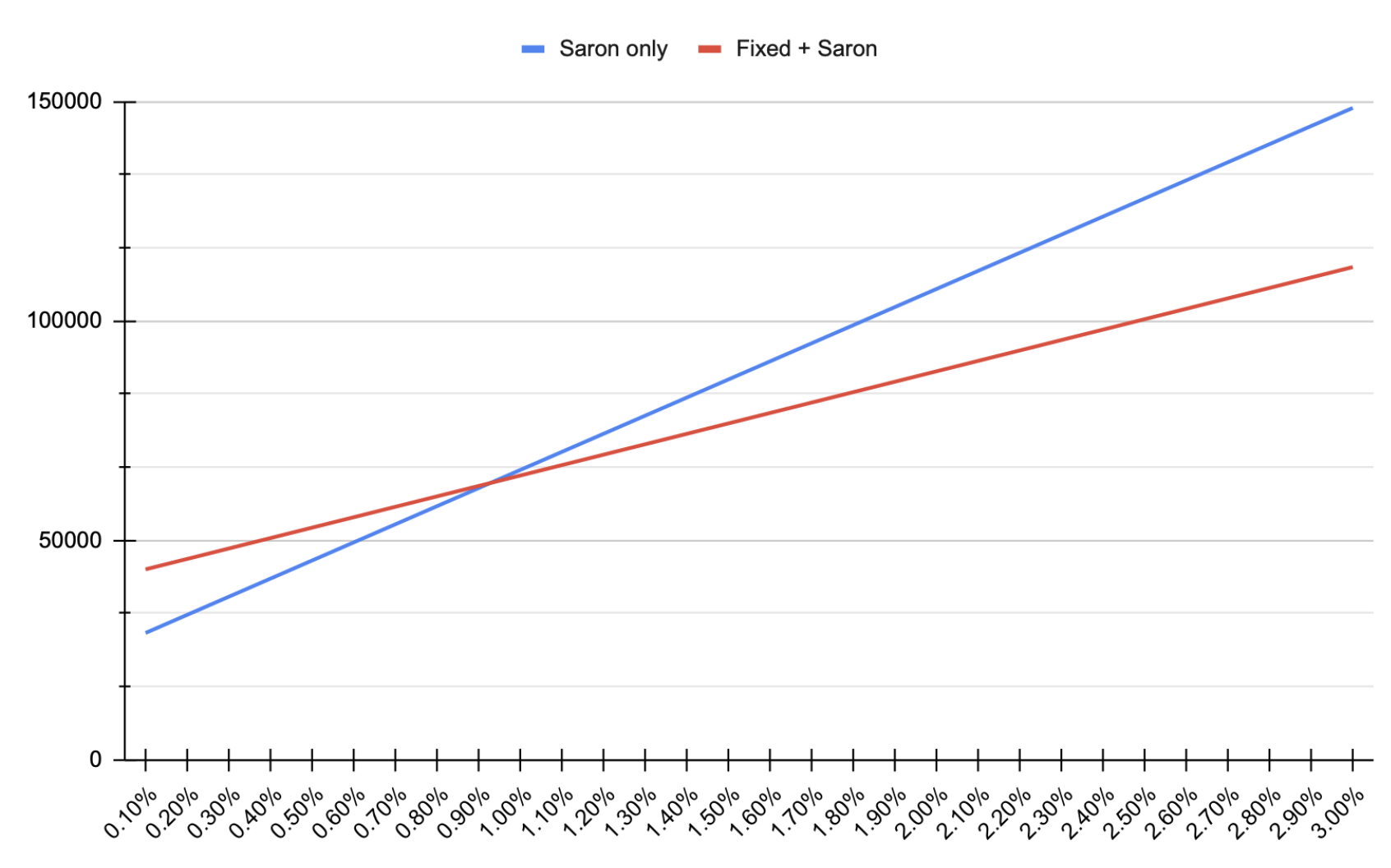

I am getting a mortgage and I need to choose between a 0.6% Saron margin for the full amount (high 6 digits) or take over the existing one (40% fixed at 1.46% for another 5 years + 0.65% Saron for the rest).

I tried to plot the interests I’ll have paid after 5 years, as a function of the average Saron rate:

The crossover point is exactly where we are now at, but everyone tells me it’ll be 0.5% higher in a few weeks and possibly 1% higher in a few months. OTOH, banks tell me that the Saron rate is expected to go down again in 2024.

The risk-averse person in me is heavily tipping towards taking over the existing mortgage, to minimise the downside in case of interests continuing to go up. What would you people do?

That would be a no-brainer for me and I would take the fixed + Saron for the rest. Getting a 5-year fixed rate for 1.46% when the current rate is >2.5% is a very good deal.

When they expect this, why do their quoted mortgage rates not reflect it?

I would not listen to the banks as they have incentives for you to switch. The market implied SARON rate (based on futures) for march 25 is currently ~1.7%: Three Month Saron® Index Futures Contract Pricing

It is expected that the rates go down in 2024, but the highest market implied rate is currently roughly around ~2.5%.

Which institution offered 1.46% for 5 years? take it!

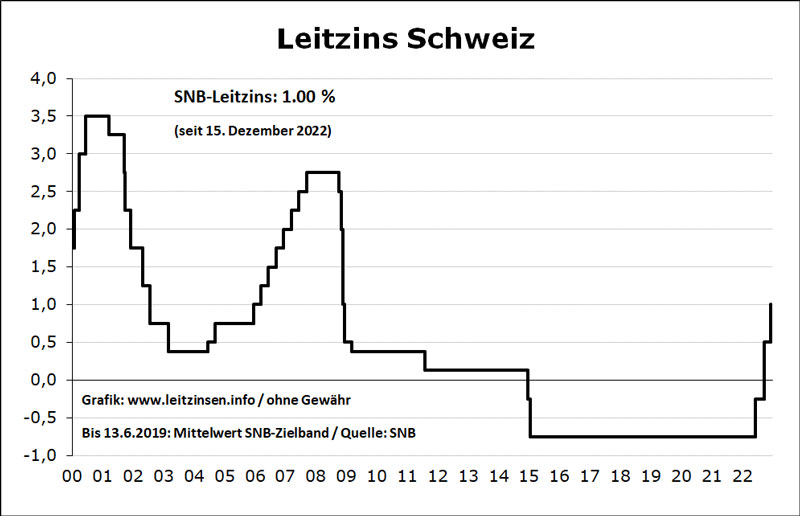

keep in mind that the 0.6% SARON is just the bank cost, you need to add the current SNB policy rate on which the SARON is calculated (today it oscillates between 0.9 - 0.96%)

The SNB policy rate is expected to increase from 1% to 1.5%

your mortgage (SARON based) will go from 1.6% to 2.1% (SARON base + Bank SARON cost).

The SNB policy rate could go to 2% in June.

With the current dev in the US this all could change I read that the FED most probably will pause and then pivot to reduce interest rates. would the same happen in CH… I don’t know.

I’m currently holding a SARON Flex at 0.68% from UBS.

The “Flex” allows me to change anytime to any institution/product. The bank must keep the same rate 0.68% for an indefinite period if the bank wants to change that rate they need to let me know ith 12 months’ notice.

If I could get a 1.46% I would take it for peace of mind.

I was offered 2.5% fixed 2 years last week… I’m riding this wave on my SARON Flex board for now.

It’s a no-brainer on 1st thought, but it’s not guaranteed that you’ll end up paying less interest over those 5 years by taking over the existing 5 year contract + adding the Saron. Looking at historic rates the SNB rate tends to fall pretty fast once the peak is reached. So if rates come down really fast in 2024/2025, we might look at 0.0-0.5% again.

My personal choice would be: take the existing mortgage, add the Saron. Once it runs out shop for a better Saron rate, change banks and stay at Saron for the rest of your life.

UBS called me today to offer a 2.11% in a 2 year fixed. that is down from the 2.5% I was offered last week.

The current situation would help us to get better rates in the next days…

I guess I could say that another bank offered me 0.6% (true) and that the increases in interests rates might start to slow down/revert, making the fixed part of the mortgage a bit less attractive…

Usually if the previous owners have to cancel their mortgage instead of transferring it to you they have to pay a hefty fine to the bank which they will include in the house /flat price. Usually this is the remaining mortgage payments, so easily many tens thousands. If you take over their mortgage they should lower the house /flat price!

I think in this case they don’t have to pay anything for canceling (according to @Cortana and depending on the contract, banks might even pay you to cancel a fixed interest rate mortgage after rates have gone up).

Any update on this? I guess they’re now paying about 3%. If the banks did their calculations OK, then I suppose they can afford it, but maybe they can’t afford other aspects of their lifestyle…

No big impact as interest rates were at 3% only a couple of months. Now you can get 1.8% for 3-5 years again and the SNB is expected to reduce its base rate down to 1.00-1.25% by end of this year. Most people that didn‘t want to prolong at those rates (2.5-3%) switched into a Saron.

Having seen first-hand in Estonia, where almost all mortgages price off 6-month EURIBOR +2% margins, what happens when rates go from 0% to 4%, I would call this “postponed”.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.