I’m new to this forum, so first of all I’d like to thank you all for your invaluable contributions.

I’m a software engineer living in Zurich since 2018, and even though I’ve been following the Mustachian lifestyle for quite a bit of time now, I’ve never invested any money in financial instruments other than time deposit accounts. I’d like to invest my money in ETFs in hope for higher return.

From what I’ve read at the forum, one should never try timing the market by investing a large sum all at once, as it (almost) never works. Instead, one should do dollar cost averaging to reduce the risk of investing in market peaks.

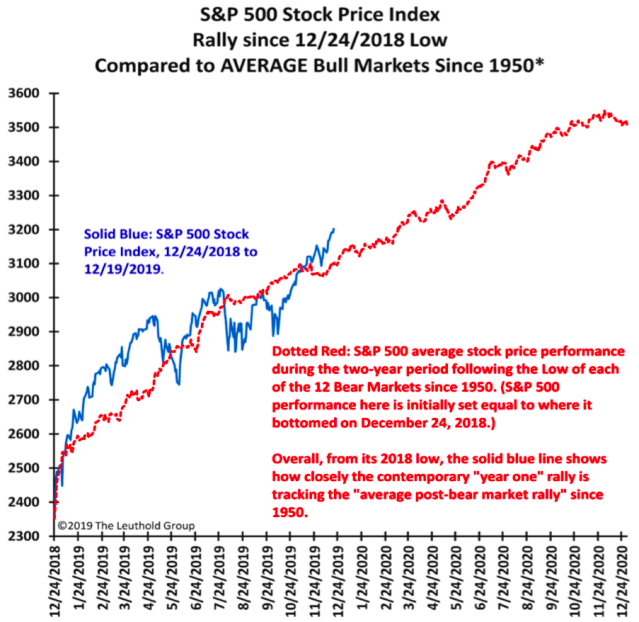

But I’m a bit sceptical about whether it’s a good time to start investing now, given the fact that the US stock market is at its all time high now, and that there are a lot of indicators of a possible recession in the coming year. The prospect of being underwater in the first few years of my investment doesn’t fill me with optimism.

“The best time to plant a tree was 20 years ago. The second best time is now.”– Chinese Proverb

Best time to invest was yesterday. The second best time is now

No avantage of dollar cost average based on backtests. Google should give some answer on this pt.

That said, if it helps lower anxiety it’s a very good reason. @americano, first you need to figure out your allocation (what’s important is that you’ll sleep well at night, and you’ll stick to it even in large market downturns). After that, DCA indeed lowers the risk of market movement (at the cost of lower returns) but what matters if that you feel good about your decision.

Regarding timing, nobody knows what will happen. It’s the stock market so you’ll see some large swings, ups and downs, but if we could predict which way we likely wouldn’t be in that forum. You’ll need a long investment horizon for such volatility (20-30 years) where you might experience several market cycles. What matters is being able to handle the down cycles (because if you pull out, that’s how most people miss on the growth since they’re unlikely to time it correctly when the market will go up again).

Agreed. Someone who saw the S&P 500 performance of -4.23% in 2018 as a sign of a looming recession would’ve missed out on +28.9% growth in 2019. It’s simply impossible to predict these things, so if you can still sleep well at night having invested a large sum all at once (to @nabalzbhf’s point), I recommend doing so.

If you already have some money aside, you are from the mindset in a very challenging position. Once you start fresh with no money, the “greed” is usually stronger than the “fear to lose”. When you look it as a long term, many year journey, the only mistake you can make is not being invested at all.

Because politics or better worldwide Central Banks are heavily involved, there is a certain reality, that this Bull Market could go on up for the next several years (with the usual market corrections on its way).

Uh, like what? And what’s new compared to last 6-8 years they’ve been saying this?

For one thing, P/E is not all time high. I think it’s even lower than just a few years ago

Take the long term view, especially if you’re at the start of your career. There’s no telling what will happen in next few years. Even professionals struggled with this, “economists have predicted 10 of the last 5 recessions.”

The effect is mostly psychological, due to this famous phenomenon where human dislike losing money so much more than making money. But if you take market index as your reference, by not investing you’re actually at much higher risk of losing money performance relative to it! So, lump sum investing is just as good. And you can DCA with your future salary income.

I don’t know where you read it but most probably you misinterpreted it. It is empirically proven that it is better to invest all at once. You can invest in chunks if it makes you feel better.

(Personal opinion: I don’t use bond much due to negative yields)

Let’s say by allocation how much of your net worth is invested in the stock market vs how much is invested in other asset classes with no or low risks (could be cash, pillar 2 depending on its allocation, etc.)

Even with these indicators, it can take years (or months, or days) for crisis to break up and you’ll lose potential returns in the meantime due to not being invested. Unless you’re enormously lucky, you can’t predict this stuff. Nobody can. Just follow John Bogle’s advice: stay the course.

We’re in a rather unique era of ultra low interest rates and quantitative easing, so I’d be cautious on drawing conclusions from past high interest rate regime situations.

It’s entirely discredited by today’s interest rates situation. Interest rates are all time low => P/E are near all time high, that’s a pretty straightforward relationship. As Buffet put it, interest rates act on equity valuations like gravity on matter, but shiller formula does not account for interest rates at all.

I was carefully reading this form, moneyland.ch and poorswiss - I have to say thank you to all the great advice you put out there, this is really helping.

To give you a little background of myself: I am 30 years old, plan to be FI by 40 (maybe retire early in Italy) and have already saved some CHF to invest (thereof 1/3 in EUR). The reason I have that cash is that I had a UBS Fonds before, which and took that out two years ago and just left it… it was not a great idea. However, with the current market situation, it seems like it is the right time to put it back into the market. This time I want to do it “right”. Meaning I will diversify as much as possible and buy only ETFs - and not using overprices UBS mutual funds.

The more I read the more I get confused, I am currently evaluating whether:

I plan to use Conertrader or IB as a broker. I was thinking about Conertrader as I prefer to deal with a Swiss company if it comes to money (frugality not super important when it comes to my hard earned money).

which ETF to buy (and from where and in what currency?). I was thinking only buying Vanguard FTSE All-World UCITS ETF Distributing - one in CHF… however not sure what to buy with EUR.

No Bonds/Gold etc. (third and second pilar is invested conservatively).

That’s something I think one would rather need to verify. And I think I wouldn’t switch everything, but maybe part (half?) to diversify the risks and compare performance, currencies and tax implications.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.