It did. Major indices in USD are making new 1 year highs, but not in CHF terms.

ist der Dollar am Vortag in Reaktion auf die US-Inflationsdaten deutlich unter die Marke von 0,8750 Franken abgerutscht. Sollte es nicht rasch zu einer Erholung über diese Marke kommen, sei mittelfristig mit Tests der beiden letzten Tiefpunkte von 0,74 Franken (Aufgabe der Mindestkursgrenze 2015) und 0,70 Franken (US-Schuldenstreit 2011) zu rechnen. Die UBS sieht die US-Devise Ende Jahr bei 0,85 Franken und im Juni 2024 bei 0,83 Franken. Bis zum Jahr 2030 könnte der US-Dollar laut den Auguren der Grossbank gar auf 60 bis 70 Rappen sinken.

However

I was thinking a bit about the devaluation of other currencies with respect to CHF. We see that long term all currencies are losing value in CHF terms. But, and this is a big but! I think these charts are misleading because they don’t take into account compounded interest earned by cash deposited at short term market rates, money market type. The effective market hypothesis would imply that no matter which currency you are depositing at short term market rates, long term you are coming to the same result, otherwise there is an arbitrage opportunity. Say, in 10 years USD is falling from 1.00 CHF to 0.9 CHF, which we see as a devaluation. But in the same period, 100 chf are growing to 105 CHF, and 100 USD are growing to 166.67 USD, which results in the same amount in CHF.

Now, if we take into account the fact that our net income after taxes is reduced by taxes on nominal yield, the stack of currency with a lower yield and lower depreciation is going to worth more than the stack of currency with higher nominal yield and higher depreciation. That leads me to two conclusions:

According to the effective market hypothesis, by investing in currencies with higher nominal yield we, Swiss investors, are expected to lose in comparison with staying in CHF. And this is even before considering FX fluctuations risk.

The negative CHF rates period, where a zero interest account would earn rates well above the risk-free rate, should have significantly boosted the value of our CHF deposits vs. any other currency that was giving positive rates.

Say you have VT, which in 10 years goes from 100$ to 200$, when usd goes from 1 chf to 0.5 chf.

Are taxes going to be based on that 100$ profit or on that 0 chf profit ?

Doesn’t matter much in Switzerland since there is no capital gains tax.

Furthermore dividends are made in the home currency of the country of the underlying stocks and the fund just give it to you in converted dollars.

Finally, if you would have a capital gain tax in a country, you would be taxed in terms of home currency.

(has to be checked in the destination country though).

Even if there was one, it would (most certainly) only be levied on the increase of the respective CHF equivalent (none, in the example). Just like wealth tax is.

If anything, differences in the relative distribution yields should be looked at. 2% interest + 3% currency appreciation is preferable to 5% interest and no appreciation (for tax reasons).

Analysts seem to think it won’t change much, I tend to agree. There’s nothing new that wasn’t known before but we’ll still see how it’ll play out. In any case, the moves in the forex and futures markets are rather small for now.

I mean, those who were loosing faith have probably not waited for Fitch to step in to do that already (I mean, Jan 6th and repeated debt ceiling crises with some Republicans, including Trump, openly saying the US should default).

I blame the current dip on algorithmic trading, but I could be wrong.

Of course, if new unexpected shenanigans happen, that could erode the faith in the creditworthiness of the US government even more but Trump supporters shenanigans due to indictments/convictions/the 2024 elections, government shut downs at regular occurences while doing budgets and a new debt ceiling drama in early 2025 should already be priced in at this point…

My biggest question on this “development” is if it impacts any reserve requirements for regulated players like bank or insurance? Didn’t touch these topics for a few years already but on the top of my head - I would have thought that if 2 out of 3 were below AAA, an asset would need to be considered below AAA. Therefore - I am not sure if treasuries would still qualify for highest ranked collateral / reserve requirements. Would anyone know anything about this?

Clearly - things will not change over night but the I still don’t think that this won’t have any impact - lets say 2-3 years down the line?

I was mainly thinking about banks/pension funds/insurances‘ collateral requirements and not specific indices as such.

This article thinks that collateral requirements for AA+ and AAA are substantially the same

Thank you for sharing. This never seems to be reported very prominently in Swiss news outlets.

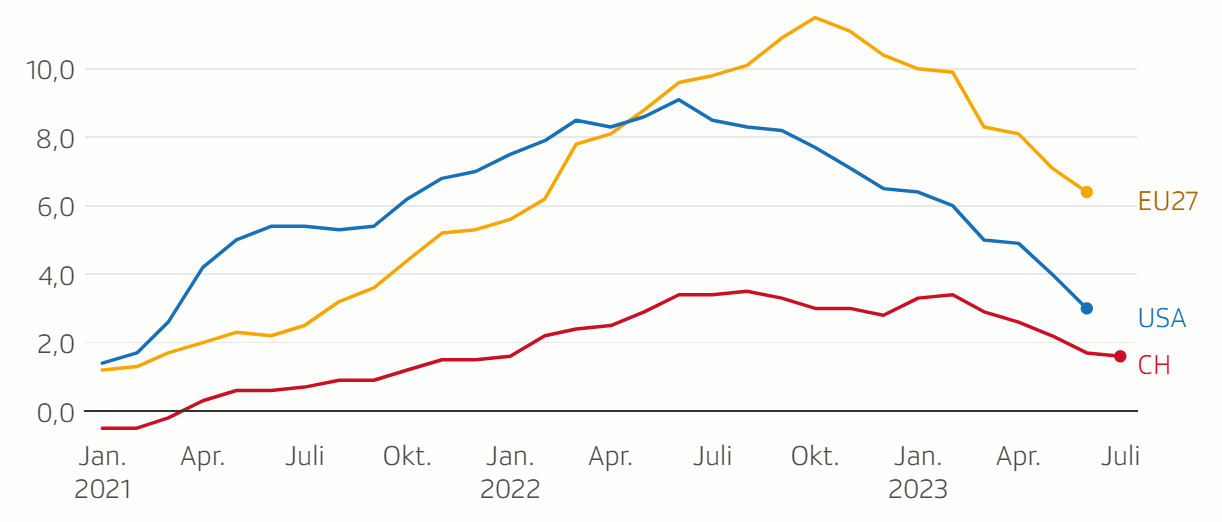

It means interest rates in CH and US might be close to their peak? Swiss core inflation is trending down (1.7% down from a peak of 2.2%). US core inflation is 4.8% down from a peak of 6.7%.

Is anyone following the latest news on energy stocks and potential shortages in winter 2023-24? I am just back from vacation and was shocked that shops and hotels were running high Aircon (doors open…)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.