Including 2nd pillar?

So you are not 100% stocks. But you are right, because you shouldn’t be.

Including 2nd pillar?

So you are not 100% stocks. But you are right, because you shouldn’t be.

I’m 100% stocks in my ETF portfolio, 2nd pillar is indeed a different story. Because I don’t get to define the 2022 strategy of my pension fund

Generally we are considering 2nd pillar as bond-like for portfolio calcs. This is because they guarantee or assume around 2% return. Even though we know Pension fund may invest in stocks (e.g. mine is around 35% growing to slightly less than 40%)

Here is the 2022 plan, part of the long term IPS strategy.

Stocks - representing 50% of assets

I expect a 10-20% correction on the markets in 2022 and I was saving 20% of past months savings in cash for buying this dip. Instead of the monthly investments I usually make, I only invested 50% and kept the rest in cash. In 2022 I will continue to buy monthly and also additionally to any -5%, as always, the following ETFs:

Real estate - 50% of assets

Rented apartments in another EU country, delivering 5% yearly net returns.

How many short term plans does your long term strategy include? ![]()

Why?

(I’m not saying it won’t happen, just interested in knowing why this year and why 10-20% ![]() )

)

None, except what I described above ![]()

Because statistically it should happen (I know I can’t predict it, it’s just my personal feeling on which I am I assuming the risk of keeping more cash).

Statistically it should have happened already in the last few years. Since well before the pandemic I heard almost daily “the crash will come soon/next year”. It’s maybe tomorrow or next year or in 10 years, no one knows.

There will always be people predicting the crash and 1 out of thousands will be correct and in hindsight, everyone will think he’s a genius. Then he’ll write about his strategy and the parameters he used to predict and sell it to others, and the next time a crash appears, they’ll realize that it was pure luck.

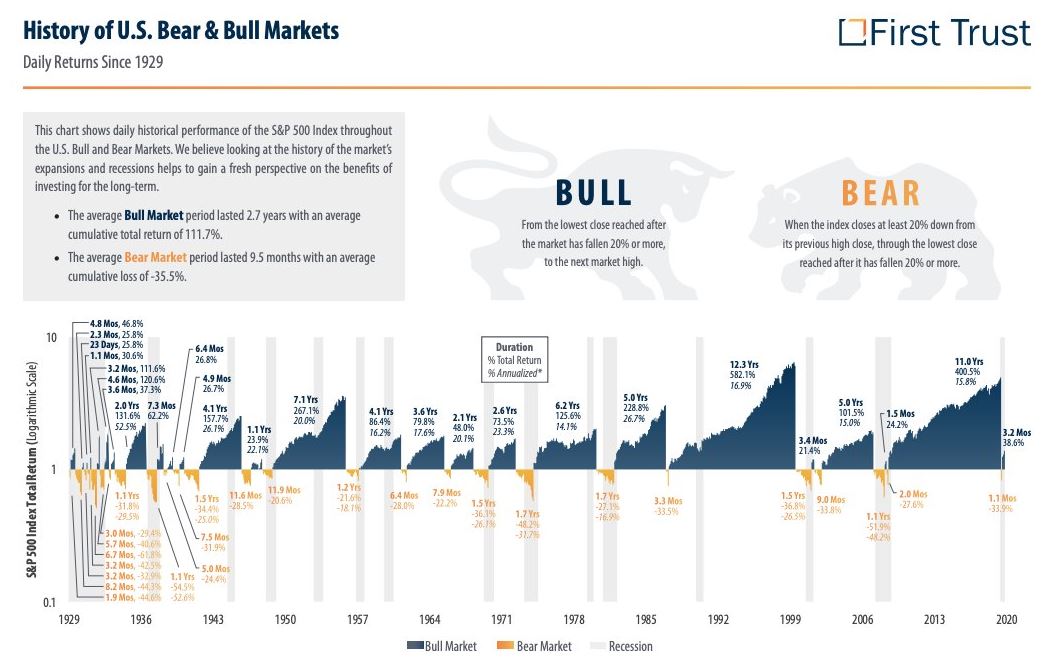

If someone asks me to show him/her one picture to convince him/her about long-term investing advantages, I think this one will be the best. However, would be cool to see the same for:

If the correction is expected, why not shorting then? ![]()

I have another question: If the crash doesn’t come, do you have a plan to move that cash into the market? And if so, when?

I said a correction, not a crash ![]() I will buy additionally on any -5% correction doing DCA over a period of time. Depends a lot on how the market will be.

I will buy additionally on any -5% correction doing DCA over a period of time. Depends a lot on how the market will be.

PS: here is something about the China real estate bubble and Evergrande: https://www.youtube.com/watch?v=WOufbsyMFk0&t=98s

wow that’s an eye opener, thanks!

Time is money (all your savings of all your life’s work).

If the next 5 years there is a drop of 50% and the 10 years are bringing in a net zero capital gain (which very well might be the case), you basically have wasted half of your time saving for the stock market - unless you have some firepower for the bottom to boost your earnings to (up to) 100% instead of zero in the same time frame.

It’s been an easy market since 2009. Not everyone has the patience/mental strength to ride out 10 years in (massive) minuses. And a good portion of the current active traders have never seen a bear market (except for the covid flash crash).

It’s also a matter of balancing this possibility with the possibility that the market might still go up for a potentially long, but undefined, amount of time, in which case, having a decent part of your assets sitting on the sidelines also costs more of your time, working, that you could have otherwise spent in another way by benefiting from those gains.

Things look pretty orderly right now, nobody seems to want to crash the market and we seem to have learnt from past mistakes. I wouldn’t exclude a soaring 2022 year from the realm of possibilities.

Edit: I guess the outlook is different when you have accumulated a decent amount of assets than when you are just starting out, which is why I plan to shift toward a more conservative allocation as my net worth grows.

Edit2: and for full disclosure, I’m also totally a market timer, I just think it’s important to have precise signals to follow and not to rely on vague concepts like buying after a drop (not saying it’s what @user137 does, my understanding is that it’s not, but the idea that we may be able to intuitively understand on the spot that it’s time to sell high or buy low is very appealing and may sound attractive to some. I don’t think it works. The profits of those who time the market successfully come from those who time it poorly - the only way to secure a win is not to play and take the market returns by buying and holding broadly diversified cheap ETFs.)

Then you shouldn’t invest in stocks in the first place.

Or you should invest according to your risk tolerance.

I am not trying to time the market, I see this as the alternative to holding bonds. So 20% cash is the new old bonds ammo, that will be used in case of something. In the past I used to sell bonds to buy specific corrections. I was getting a little extra above the market by doing so. You can beat the market with proper bonds / ETF allocation, by selling bonds at the right time and buying ETFs.

Let’s say you have the following strategy:

Above percentages are just an example. Your are basically reducing your bonds portfolio in bear trends and accumulating again on bull trends. Now what I did last year was to keep cash only instead of bonds, since CHF as you saw, had a some of a rally so I am now in a better position.

And of course, tilting to specific factors or regions (I do it on Quality factor in case of a correction) and on EM constantly can also help get a little extra.

And it doesn’t take a lot of time, just having some automated buy sell orders based on above. It’s not something I would recommend to anyone, it’s just what I do.

Hi @larix.aurea,

I’m wondering what is your strategy with your tactical cash reserve and how you plan to deploy it if the market go down.

Thanks

Sure. The “strategy” (a big word…) is based on an average ATH level for some of my most important ETF’s. As long as the current price level is > 95% I keep CHF 125,000 in cash (note: this is not the liquidity or ‘Notgroschen’, which is a separate amount).

If the price level of my ETF’s is lower than 95%, I start to buy shares thereby reducing the tactical cash reserve. More chunks of cash will be invested if prices continue to drop below certain thresholds.

On the way up, I plan to fill up the cash reserve again before buying more shares, according to the same schedule (no selling of shares, though).

I regret that I did not have any strategy in place yet when prices dropped sharply in February/March 2020.

Btw, my portfolio stands currently at 96.2% of ATH.

So if markets are just going up for years, you don’t invest anything?