It was meant as a semi-serious joke! Another semi-serious point would be that I see BRK.B as a an index of sorts, and one which is not totally correlated to the world indices.

I also believe in Buffett’s method, and think it will only be improved once he passes.

My response is: if you can’t even pick a single company, then why can you pick a more complex instrument that contains a whole bunch of companies in it within a structure you probably don’t even fully understand?

I do understand ETFs and mutual funds (though I find mutual funds conceptually simpler and more attractive) - have spent a huge amount of time investigating how they worked before plugging my savings to date into them. I also pick companies from time to time, no brainers, but not with serious money and any profits get plugged into broad ETFs.

I know you know the answer, so I don’t get the point of the question, but I’ll bite anyway: I pick a more complex instrument because it removes the onus of having to pick stocks, essentially putting down my ego, being happy with a fair share of a regression to the mean performance which was passing me (and you and most people in fact) by until we decided to hop on the train, and looking at Socrates’s “All I know is I know nothing” quote.

By, ahem, picking Berkshire Hathaway, a multi sector holding company, you delegate the stockpicking to the master stockpickers with a many decades track record.

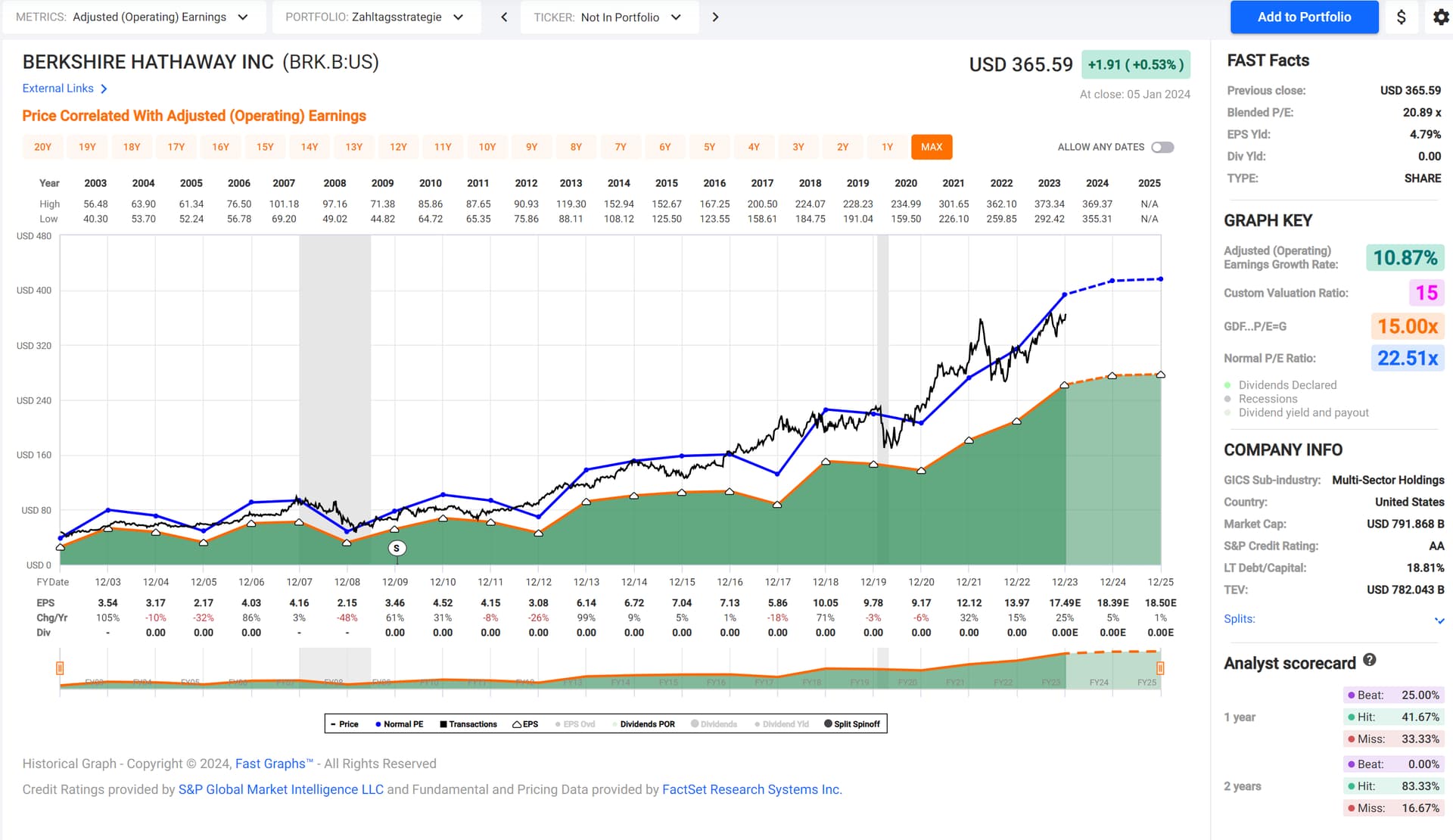

I can see this argument … (even though I don’t like BRK.B at their current valuation, given their ok but really only meh growth) … given the market has deemed it normal for them to have an about 20+ P/E over the past couple of decades.

I’d probably buy them at 15x P/E for my junior’s portfolio (growth oriented, no income required for the next several decades), but this has only happened for Berkshire about twice or so in the last 20 years.

Honestly, I am buying it because it feels less volatile than the overall world index and incorporates tens of companies, and because as I said above I trust Buffett’s method and am optimistic that it’ll go even better once they start spending the mountain of cash they are sitting on. It’s true that if I am not mistaken the last time BRK beat the S&P (other than in 2022) was…2005? It’s more of a defensive long-term stock for me.

But realistically, I don’t buy it with the intent to ever sell actually, while the ETFs are indeed earmarked for gradually selling eventually, I truly plan to hold BRK forever, passing on to my kids etc.

The stock barely registered Munger’s passing, it was probably priced in, Buffett’s death is not priced in, in my opinion. If the stock goes below -5% once Buffett passes I may back the truck to load up on more BRK.B.

Oh, sorry, I probably messaged things the wrong way.

Berkshire has beaten the S&P consistently over multiple decades. See their track record on page one in their most recent 2022 letter to their shareholders.

They’re a great company. Buy them whenever they’re fairly priced (I prefer more fairly than currently priced, though).

If their growth prospect was better (expected earnings growing at a better clip than 5% in 24 and 1% in 25), maybe buying them now would be ok for me. With that muted expected growth, however, I believe there’s better deals to be had right now (even as I love the company, just not the current price).

In even longer form:

What I meant to say is: if at this moment in time I was forced to make an investment I would not pick Berkshire for myself because

(a) I need cash flow in order to finance my lifesyte

(b) I don’t like having to sell from my portfolio to generate that cash flow especially when my needs determine the point in time of my selling and Mr. Market determines the price at which I have to sell

(c) they do not generate cash flow in the form of dividends which help immensely in generating cash flow for consumation while sparing me to sell the goose that lays the golden eggs.

I finally have some time to share my “strategy” for 2024, my first full year after properly beginning to invest last year and joining this forum. It is rather simple. Since I have basically already reached my safety cushion I will:

Max my 3a (same as the last 3 years) (probably monthly).

Put all that is left of each paycheck into IBKR → VT. From rough metrics from last year it’s around 50%. I’m still unsure exactly what way I want to go for this (i.e. if I should set a recurring payment of a fixed amount or if at a certain time each month I will basically deposit whatever is needed to get my bank account to a yet to be determined amount but that’s less important).

Continue on the lookout for a potential RE deal in my home country. If that happens I might break 2. for a few months just before, to maximize savings. CHFEUR is doing it’s part however.

The challenge for this year will be talking my SO into (a possible variation of) step 2. So far no luck as we started investing in 2021 and so our investments from there are still in the red (normal but harder to stomach for her), but at least that allows me to be more aggressive with my investments and she can work towards step 3 even if it’s not the most efficient way forward.

Oh yeah, I am aware, I was just referring to the fact that BRK hasn’t smashed the S&P500 for a pretty long time, now it’s trailing it by a bit while remaining less volatile. It’s ironic that of all people, Warren Buffett’s company is not exactly a value stock, isn’t it?

Re: dividends, I understand, I am in a different situation where I don’t want dividends. In my mind it’s not inconceivable that they may pay dividends once Buffett dies, he’s been consistently vocal about not being 100% against dividends if they don’t believe that they can generate more shareholder value by not paying them.

I think, Warren Buffet has such big investments, that he also has quite some influence on the companies. This could also make a difference. If you think, a company that you invested 20’000 in, is doing shit, you cannot do anything about. But if you invested 500’000’000, you can probably change the CEO.

The IBKR performance benchmarks are broken when the account base currency doesn’t match the currency of the benchmark. As far as I can tell, your account performance is correctly charted in your base currency but the benchmark is charted in the currency of the benchmark, which makes the comparison useless if the currencies differ.

This is wrong as well. The performance figures are in USD despite the quote being in CHF.

Been wondering, about to transfer 60% of my old 3A to FinPension (40% eaten by an insurance company), if it’s a good idea to go 1% cash, 3% Emerging, 7% CH and 89% Quality for the 3A going forward, given the bulk of my investments out of the 3A are in all-world.

I am currently 49% world ex-CH, 40% quality, 7% CH, 3% EM, 1% cash in FinPension but what’s the point if I am already all-in in all-world in my custody account?

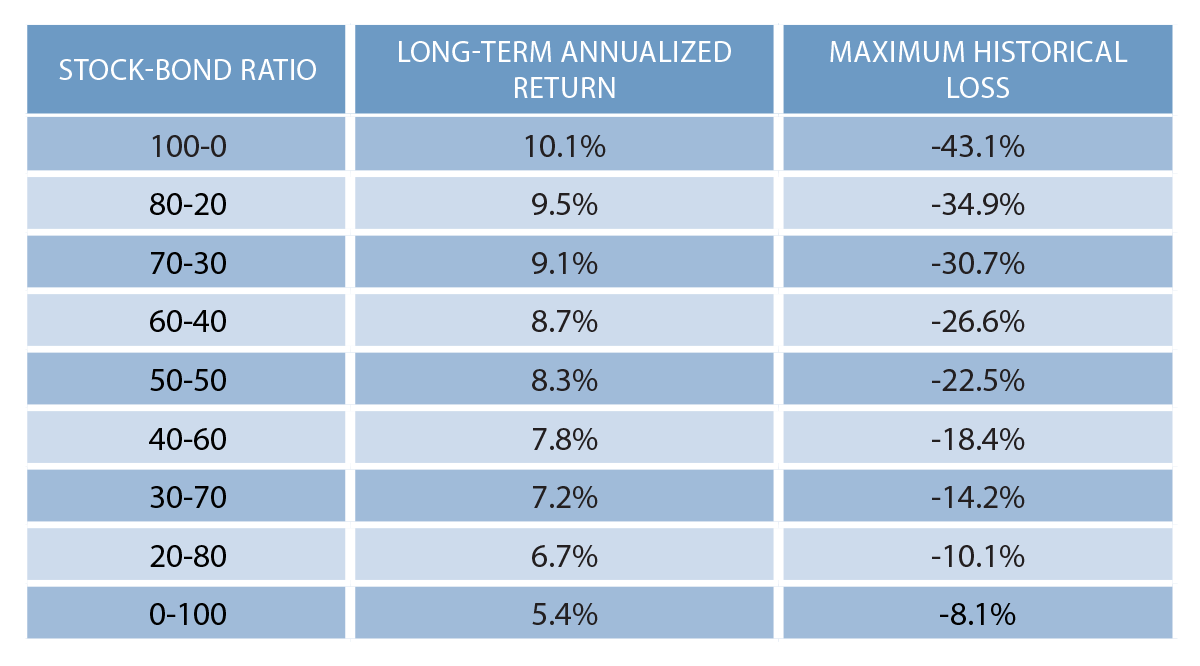

Another question, the Boglehead/Vanguard 3 fund portfolio does include a fair bit of bonds, which I happily saw are also available in FinPension. While bonds do bring performance down, they also bring volatility down (see first pic).

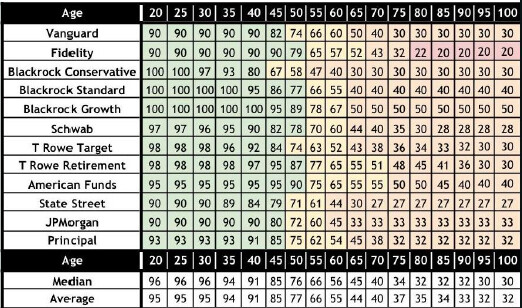

Someone on the Bogle forum took the trouble to collate the big asset managers’ recommendations on stocks/bonds/age ratios, and came up with this table.

I understand these are US bonds they’re talking about (and CH bonds seem to be extremely low yield), but what’s the forum’s idea about adding a 10-20% part in bonds (or even MMF) in a 3A, and if it is positive then are there any suggestions within FinPension?

I really feel quite unsure: if the 3A should be chasing performance or stability given its contributions are capped. I feel more relaxed about keeping a lot more money in all-world and accepting market returns in a liquid account (ie custody account) than in a locked account (ie 3A).

As long as similar assets are available in and outside of the 3a, volatility isn’t a big factor as to what to keep where: you can sell stocks in taxable (and store cash or buy bonds or others) and buy them at a similar price level in the 3a even when they’re depressed and vice-versa. The main difference is taxation.

If I were to hold bonds on top of my 2nd pillar, I would keep them primarily in the 3a: interest is the main way by which they grow and it wouldn’t be taxed while accumulating. As the principal wouldn’t grow much, there wouldn’t be much capital gains that would be taxed upon retrieval (which could have been avoided in a taxable account).

My main choice criterion would be what I feel comfortable with. You can try the allocation you think will work for you and adjust later, as long as you don’t keep adjusting ultra frequently and stick to it once you’re happy with your holdings.

Most of those funds/asset managers target US clients. With the 2nd pillar built into the swiss retirement system, we tend to have a naturally more conservative allocation (for those of us who do have a 2nd pillar), which should allow for a more agressive allocation otherwise, as long as we can stomach it (and what we can stomach should be a hard limit we abide to). I would count the 2nd pillar as bonds in my allocation.

Thank you both. Yes, I always forget the 2nd pillar, you’re right.

Edit: decided to go all-in quality in the 3A, while maintaining all-world outside of it. The two Quality ETFs from FinPension are very heavy in the US but I decided to ride this and see.

This is quite interesting. I thougt so far the Bogle recommendation is age in bonds-percentage. This would be much more aggressive. Where did you find this table? thanks

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.