I liked last year’s strategy thread very much. I even adapted my investment strategy based on some of the arguments brought forward in that thread.

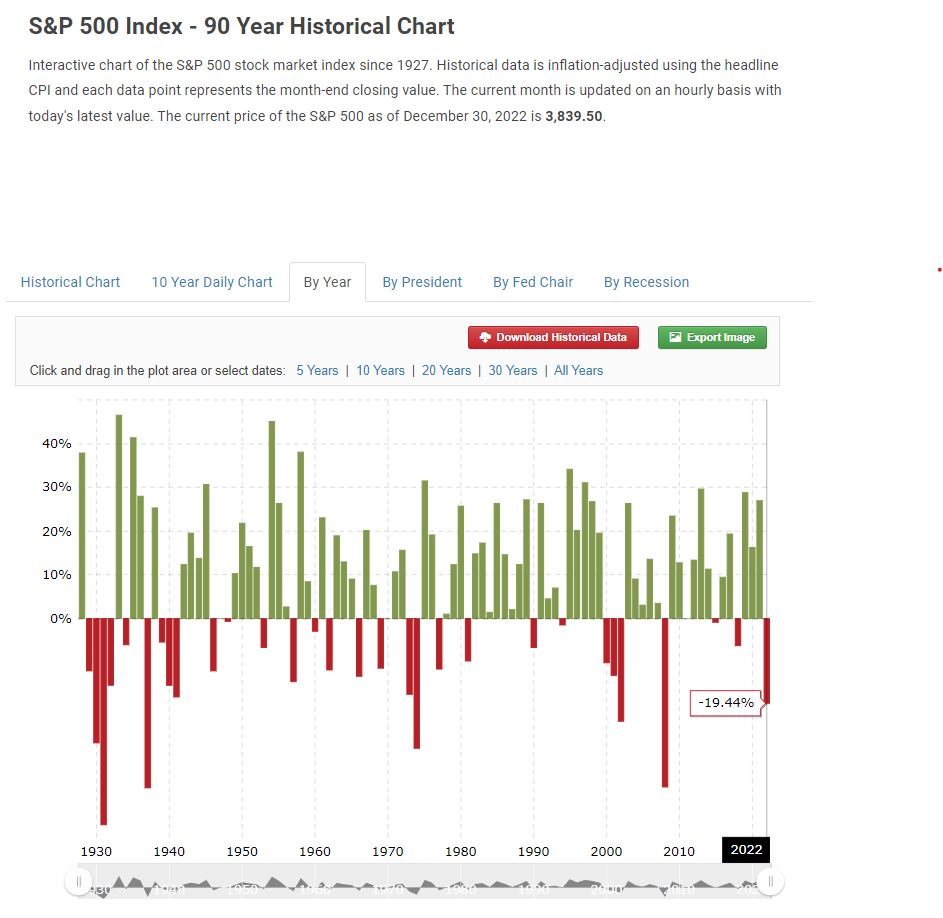

So, after a difficult year (for most of us, I guess), what are your thoughts at the onset of a new year in the markets? Will it bring some relief? Or even more pain? And most importantly… what does that mean for your investment strategy?

I started on 1 January 2022 with a CHF 884,000 all ETF portfolio. And despite fresh investments of CHF 115,000 throughout the year (mostly shifting money from existing 3a accounts to VIAC), I will end up this week with a portfolio worth considerably less (CHF 841,000)

As of today, I have 20.5% in Swiss stocks (CHSPI and SMMCHA), 19.4% in Emerging Markets (VDEM) and 60.1% in All-World (ex CH), mostly in VWRD and VT.

Strategy for 2023

Not knowing the directions markets will take I will continue with my long-term approach:

No selling, just buying!

Deplete the available cash stack of CHF 32,000 according to my secret formula

Buying only CHSPI and VT, so that the 20:80 allocation remains intact (hopefully being able to resist the ever present temptation to pick some “better” ETFs)

Stop buying if ETF portfolio has reached 45% of Net Worth (probably not going to happen in 2023…)

That’s it, KISS!

Btw, I spend more time on this forum than I should. You are an inspiring lot and I wish you health, success and happiness in the new year!

What pivot are you waiting for, I assume the moment they become dovish and start cutting interest rates? If you think this is going to happen, surely now is a good time to buy equities rather than waiting until the rally has already happened?

Like most I expect inflation to come down and unimployment to rise in the next 6 months. The FED will congratulate itself for a job well done and lower interest rates.

Still I will wait for a confirmed trend reversal, well aware that I’ll not time the bottom perfectly. My risk aversion has substatially grown in the last 12 months as I have to live from my investments.

History has at least given some credit to Kraphael, as stock market usually only bottom after the fed pivot…

but well… time will tell, if this time is really different…

As a sidenote: Eventhough headline inflation has come down recently, core CPI (The Core Consumer Price Index (CPI) measures the changes in the price of goods and services, excluding food and energy) is still very high with almost 6%…

Personally, I will continue to buy ETFs, especially since they are heavily discounted. I expect some volatility on the markets, just like last year, at least in the first half of the year, mainly due to the things that we don’t know much about, which are around:

If the pandemic will return or not.

What will the inflation do - we have a downward trend for inflation in the US which should be followed by inflation in most other countries.

If the economy will have a technical, moderate or more severe decline - it seems analysts predict that in 2023 we will have a minor or moderate recession - but there is just no way to be sure about it.

How much will interest rates rise? At the moment, we are going for a scenario in which the FED will marginally increase interest rates, up to a little over 5%. And then… will they grow? Will they decrease or stay there? And for how long?

Black Swan? Will there be another major, unpredictable event that will change all the calculations? We had a pandemic in 2020, we had a war in 2022, what will we have in 2023? Or will it be nothing special?

I think it’s a great period to accumulate equity, period that historically might not come very often:

Overall no change to my strategies in 2023: accelerate savings rate on 1 ETF for FIRE, max 3a Finpension also on 1 index-fund (99% actions), 2ieme considered Bonds (still heaviest portion of portfolio next to real estate). I am gaining more and more comfort in my decisions/results and understandings through this forum …whether for FIRE or estate planning overall - thx again to all!

However, I would love help with a decision about when (not if) I should move the majority of my 3a investments (and those of my wife that has a smaller amount by the same funds:same situation).

Context:

I am historical present at my cantonal bank, starting my 3a in a very short list of funds, which at the time were still maxed at 45% actions (so I took 2 Swisscanto funds: SWC BVG3 P45, SWC BVG3 StP45)

my situation evolved with a purchase of an apartment, through family which had its mortgage at the same cantonal bank, where the “family price” was considered as the rest of the downpayment. Long story short, my mortgage wasn’t negotiated as well as it could have been but purchase was a steal.

Moving forward, in Jan 2022: within my indirect gage, I asked to sell my existing 3a funds (45% actions) to reinvest them to the newer funds at 95% actions, but I got delayed by my bank telling me that I wouldn’t be able to reinvest at all since their policies had changed for 3a in “gage” (insult to injury: Jan’22 would have been perfect timing to realise 42k CHF gains on the 134k CHF overall value)

After really insisting, I was later told that I’d be able to “exceptionally” invest again but I’d need to take an even shorter list of funds (only ones from the bank). This obviously lead to me saying FU and triggered the following thread Mortgage Negotiation with 3a Indirect to Free Up for Investments, where I had my apt re-evaluated to know what I’d need to pay down to free up my gage and invest whats left as I wanted

In the end, I was able to free up the “gage” even without selling any invested 3a funds, hitting the magic 66% only on the evaluation the value for my mortgage, but by then Russia had invaded Ukraine and I am down 18k CHF today

I now have portfolios with Finpension where my future strategy is clear and all new 3a amounts go

Questions:

I’ve been telling myself "now you need to wait before selling to get back your unrealised gains" but I am now wondering if this is not too conservative?

I could still realise 24k CHF profit even today, and as they are only 45% actions with high TER and crazy “droit de garde” (>600 CHF / year), would I not be better off to sell them now, sacrificing the 18k chf of unrealised gains to reinvest them at 99% actions and lower expenses before the markets go back up?

I am still hesitant since I “see/feel” the paper loss but with much lower potential returns at my bank, I’m realising that I am likely missing higher potential for future gains in addition to lower expenses in the meantime at Finpension.

So as much as it bothers me that my bank literally cost me 18k by not letting me realise those gains*, I would’ve perhaps not been provoked to free up my gage as quickly either, so may not be as bad as it feels…I don’t want to be stubborn and miss another opportunity - so all comments are welcome!

THX in advance for any advice/opinions guys and gals!

*best scenario, would likely have been to have sold 3a funds in Jan’22, sat on the cash, reevaluated apt, reduced my mortgage to 66% as needed at the next mortgage negotiation, transferred cash remaining to Finpension for reinvestment…but Feb’s events happened faster than me thinking that through

Not sure I am following up well, but it looks like a pure mental accounting / anchoring bias. 100k is 100k, no matter how high is your unrealized gain or loss. If the question is to keep 100k in shitty expensive funds with 45% stocks and some bullshit or to move these money to your portfolio at finpension, the answer I think is obvious. Any time, no matter the current state of the market.

Furthermore, I prefer not to have business relationship with entities that were or seemed trying to trick me. It looks like the case in your situation.

Another note: your bank had probably saved you some paper losses by delaying your investment in funds with more stocks . Now after a major crash, it is even better constellation to move funds into more stocks.

This thinking doesn’t make sense to me.

The market doesn’t care whether you are invested in an expensive product or if you change to a cheaper and better solution. In both cases you are invested. So all you need to do is find the best solution from here going forward. You can’t change the past, you can only do better in the future.

And investing in a cheap option with 95% stocks certainly sounds better than your current one.

@Dr.PI : you hit the trifecta i think …all three are true! To be honest, even typing out my long post, I was already convinced that I had been deluding myself - any perceived “paper loss” by selling expensive 45% funds short term when the market is low is only relevant next to the long term potential gains for cheaper 99% funds as @Luk_nuts also exactly mentions.

So decision confirmed: RDV to be made asap. THX everyone - just needed a kick in the pants.

P.S. @nabalzbhf : this is a good way to look at it…I was indeed biasing myself into no action rather than look at it more objectively.

I am expecting a baby in March and I am increasing my emergency fund as it is unknown for me.

I am sure i won’t be able to maintain the 65% saving rate with the loss of salary for my spouse and the cost of the day care starting end of June.

We have almost all the furnitures for the newborn so nothing crazy expected.

I am stilling wiring 4kchf monthly to IB but I have not invested the cash at the moment.

I will stack it just in case.

My plan is still to invest it in VT.

both of us will maintain the Viac Global 100 or custom strategy with Viac.

We’ve been through this, but and for us was either wife losing the salary or paying cost of day care. There should not be both: if baby goes to day care, the wife can work, if she stays home with the baby, there is no day care cost.

What is the reason for this in a time when we have already a huge discount on all stocks?

My strategy is continuing to invest large sums of money into the capital market through VT.

At the same time, I’m continuing to study the real estate market in the canton of Zurich, but I’m not yet sure what to expect regarding opportunities.

Also considering whether to sell my RSUs and convert them to VT.

From a risk management perspective, this would be the better decision, but I also believe in my company and count it like an income. so it’s not clear to me yet from the financial side. I’ve not yet made a decision.

True,

But what I meant (and not sure if it’s true) is that you can also look at it another way and say:

I work for a company and I enjoy being there. My salary, including RSUs is X.

If I want to reduce risk or if I don’t believe in my company’s growth, perhaps I should consider switching to another company to balance this?

It’s unlikely you can really know what will happen to the stock price, and it can even touch an entire sector (eg tech market right now) so that changing company wouldn’t change the outcome.

Maybe just don’t compound the risk, you already have a lot of exposure between grant and vest, there’s no need to increase that risk.

Invest at my current target allocation, without leverage, until I feel secure the market has hit a temporary bottom and I can handle a potential subsequent leg down later on. Leverage must be activated at the latest on March 31st.

Then, invest on leverage with a target allocation of “stock market exposure=1.4x liquid assets”.

Keep on the lookout for interesting real estate opportunities, both on a financial and personal wellbeing perspective.

Leverage has been activated, I’m planning to ride this out whatever hells it takes us through.

Single, no dependents, self assessed high need for risk (need of having options to quit my job), self assessed high ability to take risk (good family/friends network with an ability to help, useful skillset, high ability to adapt to dire circumstances), self assessed high willingness to take risk.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.