This boils down to savings rate and return on investment. 7% is pretty good, so if that is not enough, I’d look at the savings rate: either look to where you are spending too much, or how you can increase earnings.

I’m pretty sure if I invested every dollar I had in real estate into ETFs instead, I’d be far richer than I am today. I think the one good thing about real estate is that it is a forced investment that has high friction which prevents you from panic selling. So you are just forced to save/invest each month for decades. That same discipline applied to stocks should be far more gainful.

Frankly for me it boils down to “when”, rather than “how much”, I remember a graphic showing that a person investing 20k aged 18 (and never investing again) has more money at 65 than a person investing a fixed amount from 30-65, or even 25-65 - I don’t have the graph handy. I started late and any modelling shows me that missing 15+ years of compounding makes it impossible to catch up. That said, 2012-today has made people I know personally go from 0-1000k so yeah it can be done!

I had this convo over the weekend, taking living in Greece as an example, I wouldn’t call anyone with less than 3mn EUR “rich”. 1mn on JEPQ can fund FIRE pretty comfortably but not at all extravagantly. For me the cut-off of “rich” is less about being FIREd and more about whether you can really make big ticket spends (>500-1000k) without batting an eyelid. My grandpa, a businessman, used to say “Unless you can spend 10x without a second thought, don’t even spend 1x, you can’t afford it”.

Yes, sure, that’s my projection too - a good spot, but no Ferrari for my dog. I don’t even have a dog anymore

Well, this is where lifestyle and attitude become important. I have no desire for a ferrari for my dog, or flying 1st class to stay in 5* hotels and so becoming ‘rich’ is easy for me: the things I actually want are free/cheap.

One concept has helped me: that is to figure out if/when you have already earned the last dollar you’ll spend. Unless I make better strides in my battle against frugality, I’ve already earned the last dollar I’ll ever spend. Every further dollar that I earn will go to my kids.

I’ve basically hardly spent any discretional money over the last 7 years due to all my time being spent on work/kids and so no time and no energy to spend money on anything.

I used to like to go to restaurants, but after years of not going, it isn’t even that attractive any more: many restaurants don’t have healthy food, high end restaurants are limited and I don’t want to spend 2 hours on eating. So I ended up in a situation where the less I spent, the fewer things I wanted to buy.

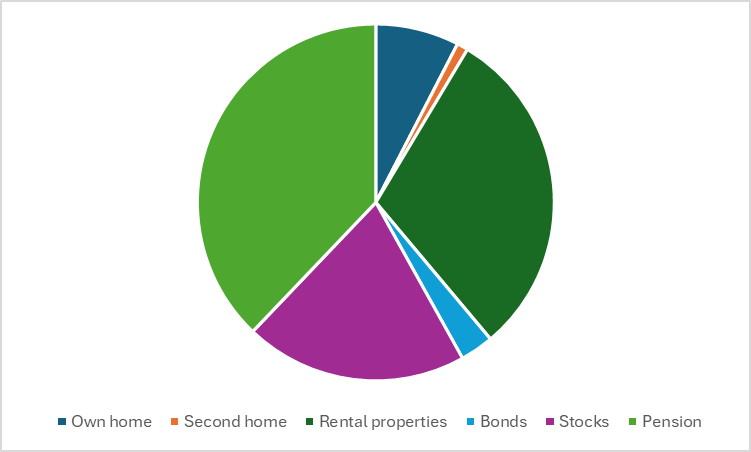

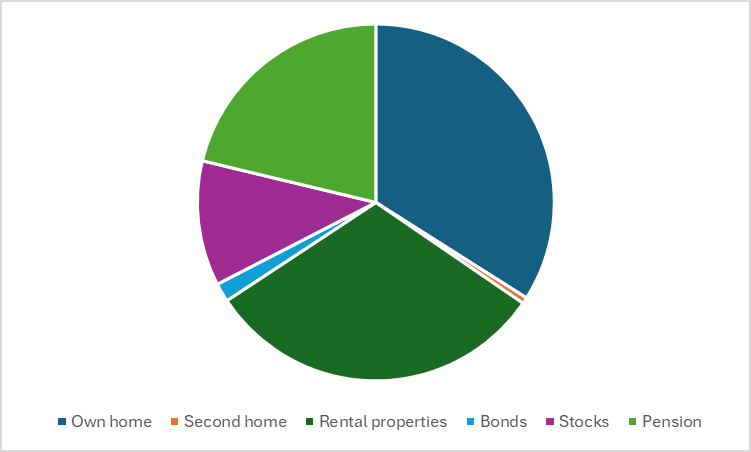

Pension is actually less bad than I thought, in both comparisons. Clearly, ZH housing prices went crazy over the last 10+ years (Rental properties not in CH!).

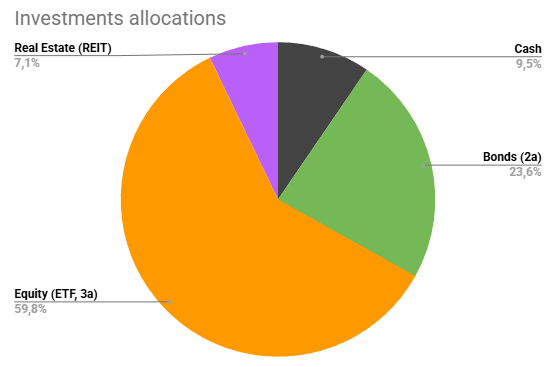

LPP 3a represent 10% of it in the ETF part.

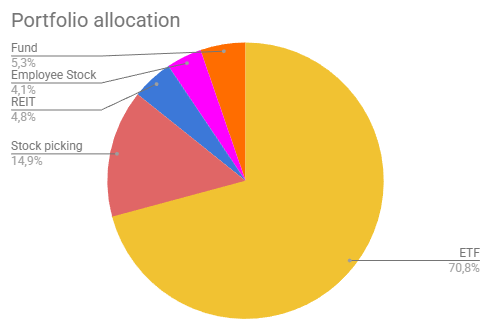

I have too much stock picking on French small caps and I am aiming to reduce it.

The fun money target should be no more than 5%.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.