Sure, but you don’t see your debt here. It is a different thing to have 2m or 1.3m net wealth. If you do it according to my idea, the allocation would be 77% both and the leverage ratio is 1.54.

I was also calculating debt as an “asset class” with a negative value. Same thing, different viewpoint, but you can’t depict it as a nice stacked column.

I don’t like gross wealth because you can arbitrary change it by taking and repaying debts. That means it is not “real”. Psychologically it can also affect how you think about money if you focus on gross values. So I am trying to go around it.

Say, if I see that my stocks allocation is 250% of my net wealth, I would start worrying. I would never be there in the first place. But if you look at gross values, your portfolio might look great!

I think 250% doesn’t help too much because it conflates 2 different things: asset allocation and leverage.

Let’s say you have 250k stocks with 150k debt.

250% of net assets tells you nothing without knowledge of all other assets.

100% of gross assets tells you that you are all-in on stocks

now you can be concerned that you are all in one asset class

now the other side is how much debt you have.

250% tells you that you are leveraged, but you don’t know by how much without seeing all the assets (after all, there could be another asset with 350% of net assets)

if you look at leverage separately and see that debt is 150/250 = 60% of gross assets

With all the information, you can compute everything, but I find it helpful to look separately at asset allocation and leverage rather than to create this calculation which tries to capture both in some way but can’t convey the true picture without viewing the whole.

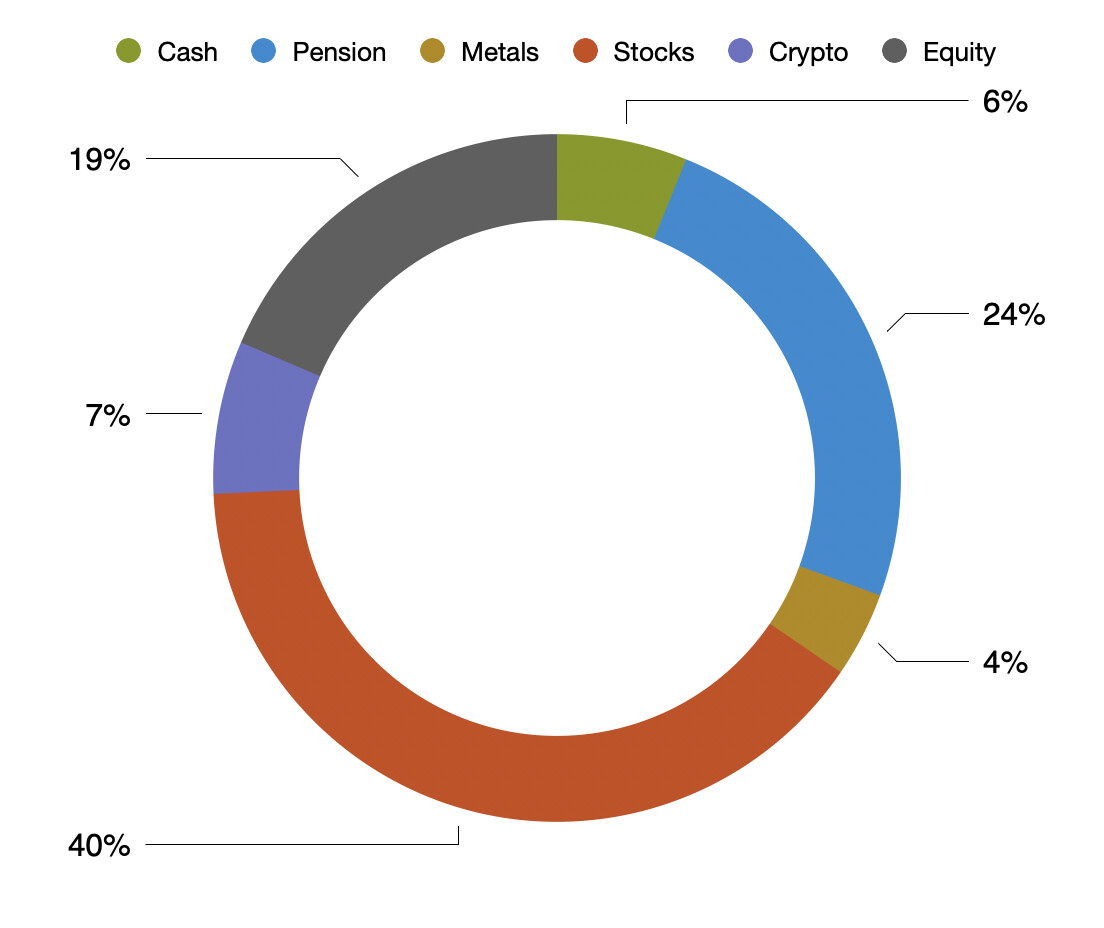

I would be curious to know what’s the typical asset allocation for folks in the taxable accounts or Real estate. Given the perceived higher valuations across asset class, I want to gather your thoughts at this moment as some of you are much more experienced than I am.

I am excluding 3a and 2nd pillar because the money is locked in for many years and might not have similar impact on one‘s emotions like the taxable accounts.

I am starting to wonder what should be my asset allocation because it’s tough for me to define what’s my real risk tolerance actually is. How would I react to a 30% drawdown in equities ? I don’t know as I have never experienced it.

I understand that in accumulation phase it’s best to have high equities

For me right now, my taxable account is 70% equities, 30% fixed income/cash (low yield, short duration)

Were you investing during covid crash and if so, didn’t you get a 30% drawdown then?

I had 3 big drawdowns: dotcom crash, 2008 and covid.

dotcom i had too little invested to impact me, but i do wonder if it subconsciously turned me off investing as I didn’t invest for a long time afterwards.

2008, i was invested mainly in real estate and so didn’t have a big exposure to stocks. i was also extremely bearish during the run up to the crash so in a way, I saw it coming, but didn’t have the knowledge/experience to benefit from that other than to avoid the stock market losses (didn’t know how to bet on the downturn).

2020, i thought i was prepared to hold through, but i made one huge mistake: i used margin and this ultimately forced me to sell at the worst possible time. had i not had margin, i’d be up 7 figures more that currently. i now no longer use margin after this experience.

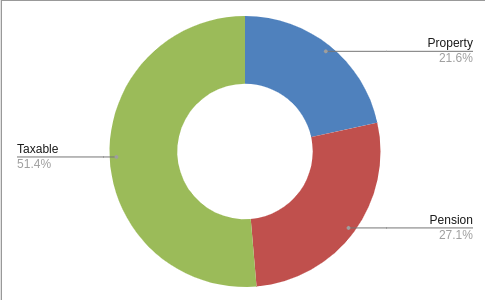

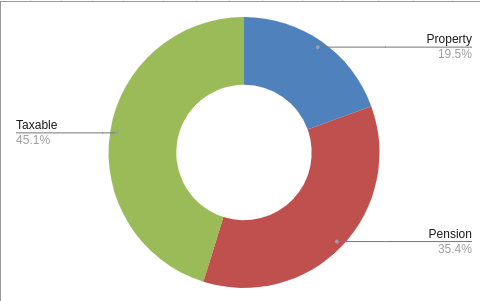

in terms of asset allocation. you have to think whether you look at taxable as a whole or look at the whole including pension funds. some people will look at the whole and take the pension fund as their ‘bond portion’ and so if they want 30/70 bond/stock and their pension is 30, the taxable stock portion is 100% stock to make up the total 30/70 split.

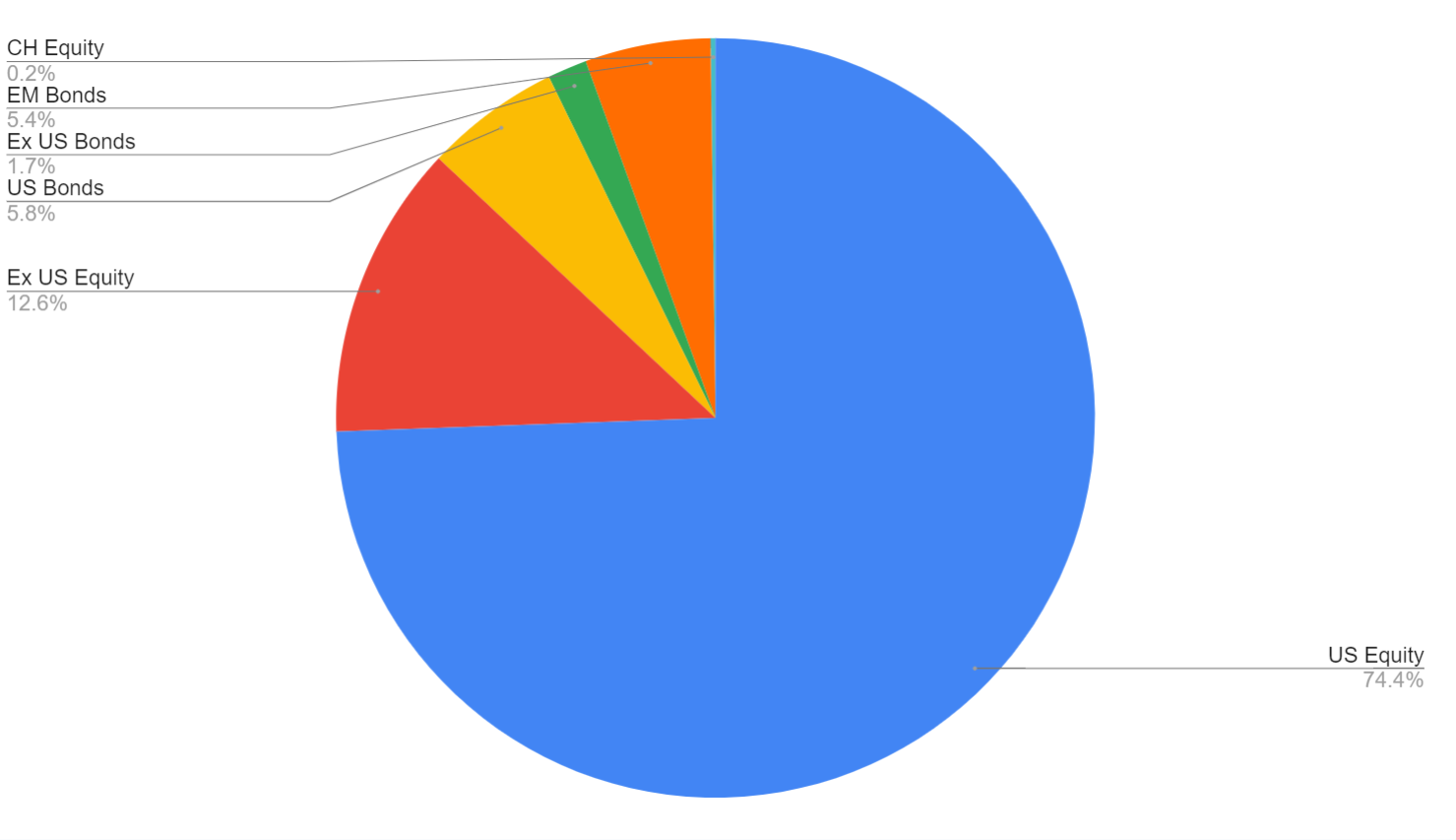

in my current taxable portfolio, i’m about 70% stocks. The remaining 30% is 9% bonds and the rest: gold, gold stocks, uranium (sprott and yellowcake plc) and CAOS. the bonds will be sold over the next few years and moved into the pension fund (voluntary purchase).

i’ve tried to de-risk the equity portion by buying low-vol, low-beta and generally boring steady stocks (with a few speculative ones thrown in for fun).

My first real investment happened in Feb 2021. any earlier Investment was most likely without me knowing.

For example I enrolled in some unit linked insurance plan when I passed out of university and they had 30% allocation to stocks. I had no idea what was happening one day I checked and at one point it had 80% drawdown … I just never knew.

ah. unfortunate. it’s really impossible to know how you react to the crash so better to do this earlier to help you calibrate.

even now, i don’t know how i will react to the next crash esp. if my situation changes e.g. if i’m retired and have no income coming in, i might react differently. during covid, i was buying aggressively in - too aggressively and on margin: i should have managed my risk better.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.