During discussions at the latest Meetup in Zurich I realized that since my expenses for the year are at around 100k CHF including taxes, my FI expenses would be roughly 36k CHF lower. And an income of 70k CHF would lead to only 9k CHF in taxes, so my real FI expenses would be around 75k CHF.

What other things have to be considered for the FI number? I’m unclear about things like:

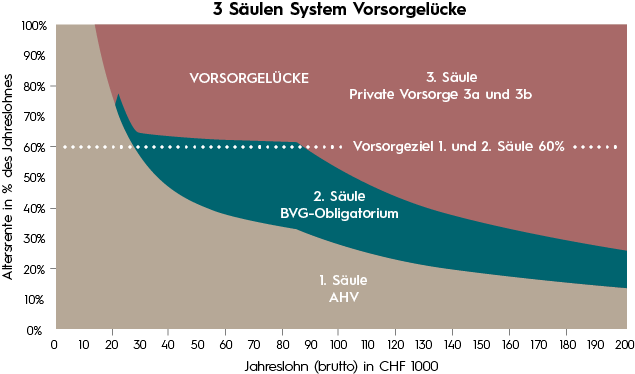

Keep paying for AHV Pillar 1 until 65? How much would that be?

Keep paying for Pillar 2? is it possible?

Keep paying into Pillar 3a to get nice tax deductions?

Anything else I’m missing like increased health insurance premiums because one needs to cover for accident insurance which is usually payed by the employer?

Any reasons on why you include taxes in your expenses? Those are highly dependent on location, income, available deductions, etc.

IMHO taxes, investments (ETFs, stocks, bonds, Pillar 3A, 2 additional contributions) should be taken out of expenses as they tend to distort the real picture.

Mortgage repayments, maintenance fees on the other hand should be included in expenses (but not amortisation).

Thanks, so let’s assume I have a net worth of 1M CHF plus an appartment for which I understand “• Mietwert der unentgeltlich zur Verfügung gestellten Wohnung,” applies which is 25000 CHF per year (which is said to be multiplied by 20) that would lead to 1.5MCHF in the AHV payments table and therefore would lead to 3 059.50 CHF in AHV payments until 65, right?

Fair point on taxes being highly depending on location. However they always will be there in some form or another… but yeah maybe I should exclude them from my expenses. How do the fellow beancount users track taxes? As liabilities?

Why would be mortgage repayments (did you mean interest payments or the renewal fees?) but not amortizations be tracked as expenses?

My reasoning is that mortgage repayments (interest + monthly maintenance, fees) are part of expense bearing items whereas amortisation payments go towards building up your asset and equity.

I do not consider the overall market value of the apartment in my net worth, just consider the downpayment or own equity (although the associated mortgage is used for reducing the wealth tax implications).

That’s correct. But it’s totally worth it. If you retire at 50 and miss out on 15 years, your max. AHV rent will be ~1620 CHF per month, so you’ll lose 9k/year. For not paying 15x3k.

If retiring at 45 or younger that would be rather 20x3k… but yeah probably worthwhile since the return is very good on that one (expected 20x9k starting at 65).

What about Pillar 2? What would the contributions be? Can there be any?

Once you stop working your pension fund assets will be transferred to a 2nd pillar institution like Viac or ValuePension. No further contributions can be made at that point, same for 3rd pillar. Only way would be to start your own company.

Btw you need a total gross salary of 3.72 million CHF (without kids) to get the max. AHV. Otherwise it’s less than that. But paying the required amount yearly once retired is still worth it.

I never did the math myself to be honest … so you are saying that paying 5% (the rough AHV percentage) of 3.72 million in salary (so 186k in ahv payments) ensures already the minimum monthly payout of 1620 chf, right?

It ensures that you get 2370/month if you have no gaps (44 years).

Looking at those numbers you should realize why paying 190k over your working years and getting 15-25x28k (420-700k) once retired can’t be sustainable.

You can get more if you pay the minimum required amount every year (depending on net worth like above stated). But you have to be proactive here, nobody is going to ask you.

paid years/44 x 2370 = your AHV at 65 in your case.

Just did the math and my conclusion is that I basically paid a huge tax but not getting much in return given the gap years. My mental model in terms of expected CHF was actually fairly accurate so far …

yes, ahv system is big f 'ing socialist scam. good neither for high earners nor low earners - pay too little you’re on that other side of wealth spectrum

you can calculate exactly how much your pillar 1 is worth from tables here. the formula is (for refund calculations, if you’re eligible for it):

round(<number of years of work in CH> / 44 * 2370) * 12 * B20(current age)

it ain’t gonna be much if you were just a temporary high earner immigrant here. most of your money went to swiss geezers already

Lol come one now. It’s a pretty good system and part of the reason why Switzerland has one of the highest living standards in the world. There isn’t a lot of poverty in old age. If you start working here as a young adult and get to 44 years, it’s great IMO.

@IdleThought

Care to share when you started working in Switzerland? When did you stop? How old are you? Will you pay the minimum till 65?

ahv pension is not enough to live on. after 44 years of working you get whopping 2.3k pension a month (and even have to pay tax on it). this is a big f’ing joke considering CoL here. well yeah you won’t starve (there’s a separate thing that takes care of that), but i wouldn’t exactly call it a living, more like barely surviving.

Hence why there are also the 2nd and third pillar, or complementary subsidies for the people who haven’t got them.

The system is flawed, I agree (I’d really like a flat AHV pension without difference between earners better than the current system) but it IS designed to allow poor people to get some measure of a safety net while richer people should be able to maintain their standard of living, provided they do save some and don’t spend it all on lifestyle creep.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.