Pension funds may apply the same interest rate or guarantee the minimum interest rate for all parts, but they are not legally required to do so. I don’t know how pension funds manage this in practice or what rules are common in pension fund regulations, though. Maybe deviations are more common when the minimum interest rate is higher.

BVG-Überobligatorium: Einfach erklärt also confirms this with “Im überobligatorischen Bereich haben Pensionskassen keine Mindestvorgaben für die Verzinsung.”

Nop its not (if the fund had sufficient reserves, no material inflow of employees, no change in technical reserve calculation ruleset and the fund performance X was approx 0.25% larger than the technical interest rate). THEN, your interest Y may materially exceed X. This happened quite often, the last few years

Some Big4’s are self managing their own scheme and achieving 6-12% each year, with a guaranteed minimum of 1%. Best deal ever as it doesn’t apply only for the yearly contributions, but the whole balance. Could well be 40-50k yearly, which is a lot of net worth even if it’s somewhat invisible.

Agree, its terrible to see what profind did. Good thing though is that, if I got it right, the regulator said no-no to collective pension funds that want to distribute big time, even though they had insufficient reserves. Therefore, I ecpect this year already to be different.

nitpick revenge succesful… you’re of course totally right, sorry, I manually** picked out the wrong % from the article, it was indeed -6.4%, written in the title of the link I posted even!

Nitpicking the nitpick of my nitpick - said PK is not the LUKB PF, but simply the LU PK, which is the PK of the civil servants, teachers, etc. of Kanton LU.

As a self-employed/business owner, how would you chose your second pillar provider ?

Having no clue, I went with whatever my accountant recommended me (Zurich insurance/Vita, paying 1.25% base + 1% additional interest, if I understand the statement correctly).

A family member of mine said this was a major headache when he started his company. Even the cheapest PF charge fees that look massive compared to a VT portfolio.

You are technically allowed to create a Freizügigkeitsstiftung for your employees but most startup founders have different priorities.

But this market looks like it is waiting to be disrupted

Is probably a thread of its own, but I would be very interested about the feasibilty. I never heard about a small or middle company having its own Freizügigkeitsstiftung.

Btw if I understand correctly public pension fund typically have much lower reserve right? (They have more institutional stability plus state backing) So we can’t compare with private sector.

I don’t know, I suppose what you say is correct because I get the impression that most federal employees are satisfied with their pension fund, at least those who don’t know much about it and don’t take care of their finances.

For my part, I don’t have much to say because I’ve only had short experience with three private employers, twice during an internship (6 months and 12 months) and once as an employee (5 months). I got the impression that only my first private employer (6 months internship) had a better pension fund than the public ones. The other two were with a general pension fund (AXA and Swisslife), which did not give me the impression of being a good provider at all.

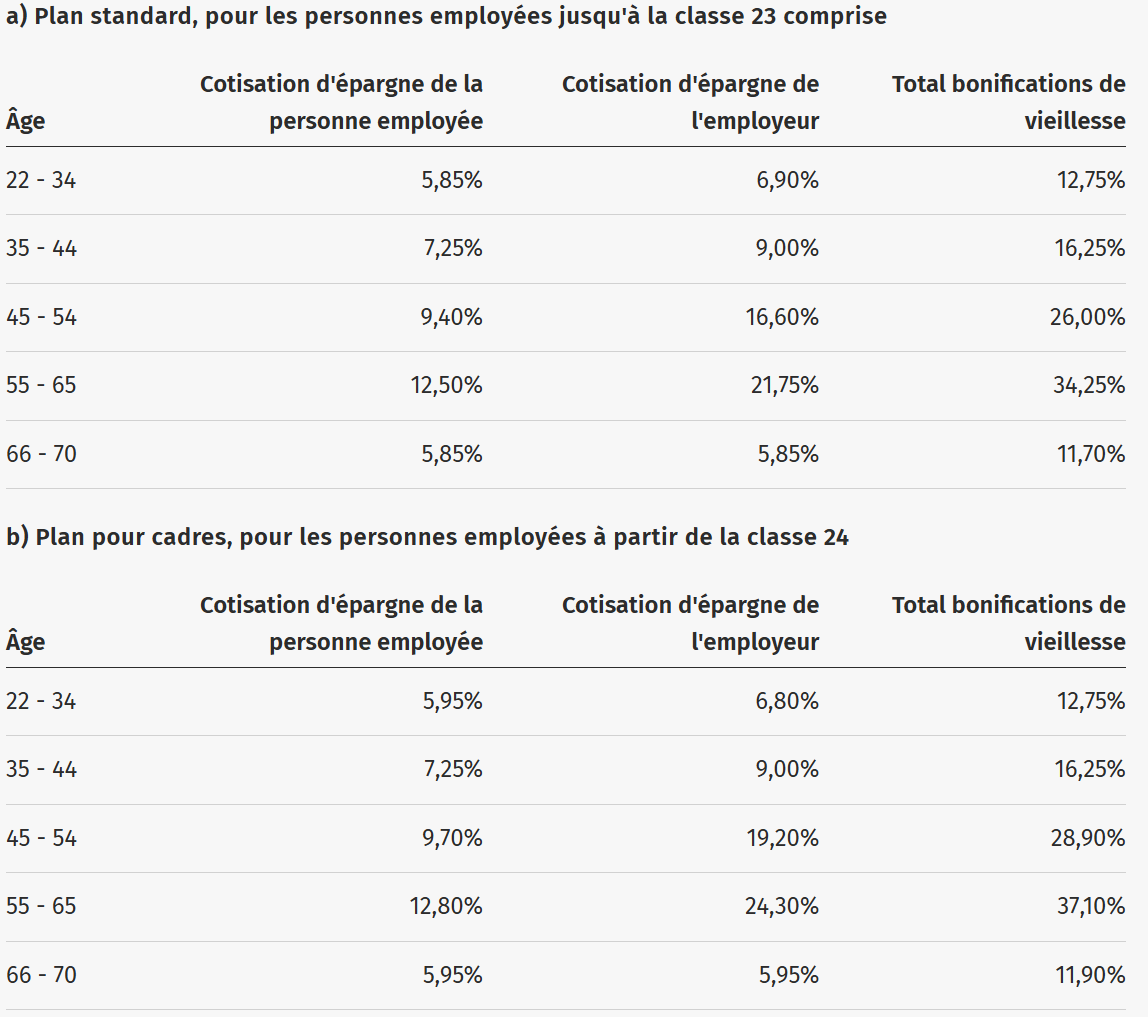

The only thing I notice in particular is that the federal government is generous when you reach the age of 45.

Are you referring to the employer contributions to the pension fund?

Those say more about how generous the employer is, and less about how good the pension fund itself is.

He refers to this table IMO. Generous indeed But as you said it does not say anything about the PF performance. As stated, the performance of Publica was not bad these past years. I wonder what was the compensation offered by the fund.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.