There are many solutions for lazy people. None of them are the best.

This is no different from VWRL(VWRD) other than being accumulating instead of distributing which makes no difference for a Swiss investor as tax payable is exactly the same.

I would say, in the long term, for a Swiss investor an accumulating fund could be problematic. Let’s say you reach your FIRE age and start withdrawing. With a distributing fund, you have regular dividends, plus you sell as much as you need. With an accumulating fund you could only get money from selling, all of which would be capital gains.

Furthermore accumulating funds are sometimes a shit to figure out in time the dividends it included for tax declaration (they still have to get paid), especially if not available in ESTV tax tool, and sometimes even then.

If they are your only source of income, then you break one of the guidelines. But some said that buy and hold investors like us would never be classified as pros.

Assuming equal dividends of 2% p.a., L1TW of 4% for VT and 10% for IWRA, TER of 0.09% for VT and 0.22% for IWRA, L2TW of 15% for VT and 0% for IWRA, I end up with a dividend-after-TER-and-dividend-taxes of 1.56% for VT and 1.58% for IWRA.

Happy to stand corrected on these figures, though.

The US ETF has a TER of 0.09%.

The IRL ETF has a TER of 0.22%.

The IRL ETF has a non recoverable withholding tax of 15% on the dividend which is ~2%. Which means et the end 0.3% of the value of the ETF.

0.22% + 0.3 % = 0.53% which is 0.4% higher TER.

Even the though U.S. accounts for biggest part (57%) of that fund, that seems a bit oversimplifying it:

It’s an “all-world” ETF:

Ireland has tax treaties with many countries that will reduce withholding tax burden to 0%.

Probably there are be at least some countries for which Ireland has more favourable tax treaties than the U.S. - i.e. for which dividends payed to the Irish ETFs will be taxed at a lower rate than to the U.S. ETF.

Some countries represented in that all-world index will not even levy any withholding tax on dividends to begin with.

Furthermore, a quick google search supports my impression that payout ratios and/or dividend yields are lower in the U.S. than most other markets. I.e. the U.S. share on dividends flowing to the Irish ETF should be lower than their share of the fund’s NAV.

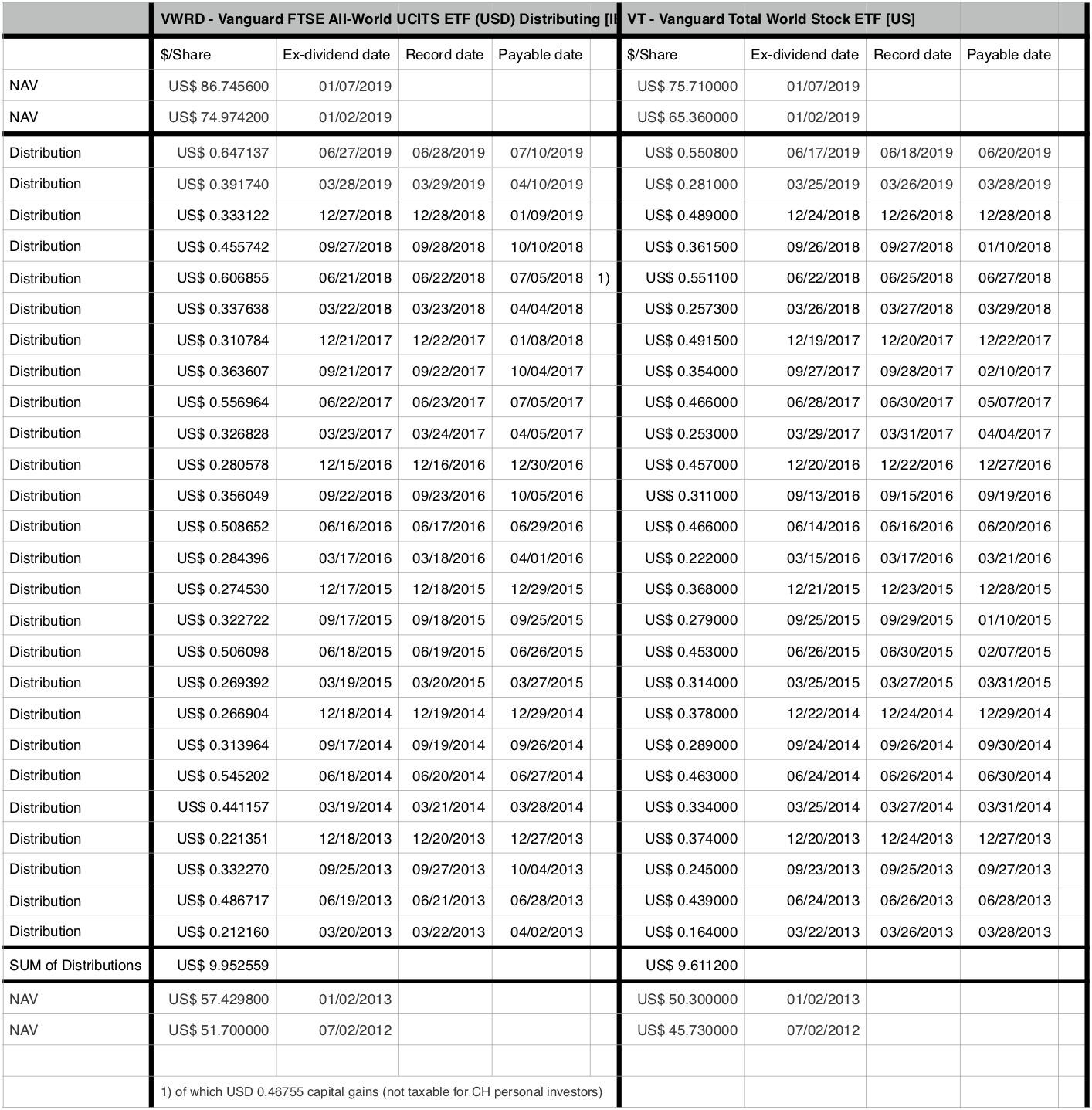

Having questioned before the fixation on TER, I have just quickly cobbled together a spreadsheet for the distributing ETFs (VWRD / VWRL domiciled in Ireland and VT domiciled in the US), beginning in 2013 - the first full year that VWRD / VWRL has been available:

I fail to see how VT or Vanguard’s US ETFs are supposedly that much superior to the Irish ones.

In this example (though not discounting dividend cashflows or accounting for compound interest on them, since I’m lazy and interest rates are now low anyway), the difference would haven roughly amounted to 1% over a period of 6 years.

I tooked your table and made a normalization for 100 USD invested on 01.02.2013. If I sum the dividend with the increase in value I obtain at the end 168.37 USD for VWRD and 170.54 USD for VT which is a bit more efficient. The TER as well as the withholding tax has an influence.

The point which is not clear for me but people with experience could answer. I I am living in Switzerland and I held VT which percentage is the withholding tax for me?

Is it 15% because the ETF is based in the US or is it proportional to the percentage of US shares in the ETF?

Withholding tax at individual level doesn’t matter, you get it back thanks to the treaty with DA-1. And then you pay ordinary swiss income tax, same in both cases.

Withholding tax at fund level does matter, because you don’t get any of it back and get double taxed, that’s why VT is more efficient.

Yes, factoring in the non-taxable capital gains distribution at (whatever) your the marginal tax rate, it’s pretty much 1% over that period.

For dividends distributed by U.S. companies to an ETF…

The U.S.-domiciled ETF effectively pays 0% to U.S. tax authorities

The Irish-domiciled ETF effectively pays 15% tax to U.S. tax authorities.

For dividends distributed by non-U.S. companies (3rd country X or Y) to an ETF…

The U.S.-domiciled ETF effectively pays tax according to country X’ or Y’s withholding tax rate (which might very well be zero!) and double taxation agreement between the U.S. and X or Y

The Irish-domiciled ETF effectively pays tax according to country X’ or Y’s withholding tax rate (again, possibly zero!) and double taxation agreement between Ireland and X or Y

So the oft-cited 15% difference applies to the proportional share of U.S. companies’ stock. Dividends from other countries will might be subject to a lot of different withholding tax rates - or none. For “World” ETFs, it does work slightly in favour of the U.S. ETFs, as U.S. companies’ stock makes up such a big part of their indexes - whereas for other countries (say a European or Emerging market index ETF) Irish funds might fare better.

For distributions made by an ETF to the Swiss retail investor:

For U.S.-domiciled ETF, if fund units are held through a qualified (non-Swiss!) intermediary with W8-BEN 15% will be withheld - but should be “refundable” through DA-1.

Distributions from the Irish-domiciled ETF to these investors will be free of additional withholding tax.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.