Thanks for the response, and wow so it is not 10% hard cash. Is there still a limit on how much you can pledge 3A? You think i should push the bank? I am surprised they’ve never brought this up.

You can pledge as much as you want. You could for instance pledge 10% and pay 10% with a 2nd pillar withdrawal but it’s always a matter of being able to pass the affordability calculations.

Um, yes?

It‘s 10% hard cash (e.g. bank accounts, pillar 3a). Equivalent can be pledged. Be aware that banks are taking a 10% security margin when pledging 2nd pillar (your 2nd pillar must be CHF 111‘111 if you want to have an equivalent of CHF 100‘000 in pledged assets).

Edit: the bank does not have to bring that up. If I see, that with that option your affordability ratio will move into a non-financiable range, it‘s low priority to tell you about that since you do not meet the criteria anyway.

Just to add: whatever you pledge as 3a (and if you pass the affordability test as pointed out by others), your mortgage amount will actually be increased by the pledged 3a amount. Therefore, this increases the amount of interest to be paid (which, in turn, has an impact on your affordability calculation).

7 Likes

In other words, when you pledge 2nd or 3rd pillar, you don’t provide an own contribution to the value of the property (downpayment), but provide an additional collateral to the loan that can be liquidated by the mortgage provider if there are problems. The whole value of the property can be loaned in this case.

Like all leveraged strategies, it’s a double edged sword, but considering illiquidity and specific goal of the investment, not so cursed one.

3 Likes

Thanks for the comments, very insightful. How about using a mortgage broker? Do you see much benefit or suggest I go straight to the banks.

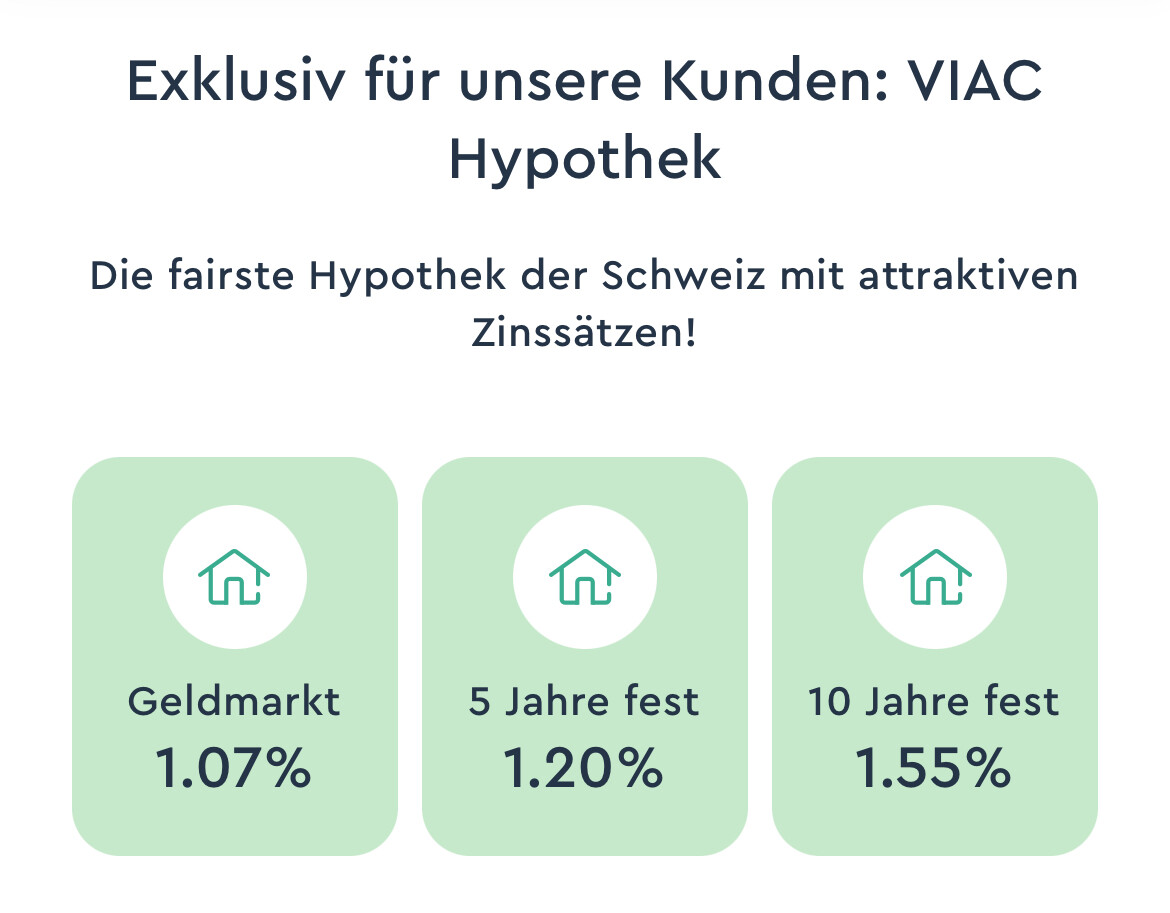

VIAC offer is suspended until may. WIR Bank does not have sufficient HR ressources …

3 Likes

They pushed it to June due to constraints with WIR bank.

Due to personnel bottlenecks at our partner, inquiries about the VIAC mortgage cannot currently be guaranteed or cannot be guaranteed in the desired quality. We are working with our partner to optimize the product so that we can offer it again from the beginning of June.

1 Like

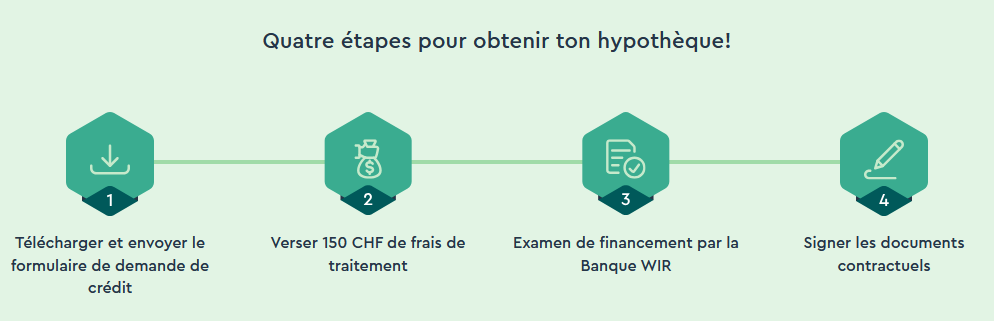

Do I understand correctly that, to submit the mortgage request, we have to pay 150chf?

Is it a normal thing to do?

I would understand the wording in the same way.

And no, that is not the normal way, the offer should be free.

1 Like

Clever, I would do the same if I have limited capacities - focusing on clients with commitment rather than on the „shoppers“.

5 Likes

I agree, clever.

Can we see the rates somewhere?

I think the Viac mortgages are still not open, but can we see the rates either in viac or in Wir bank?

I don’t want to submit a request only to view the rates

Wow, really looks like they are not looking for any new customers anymore… Those rates are quite away from the market.

From my personal experience, I can recommend hypotheke.ch - a few years ago, I got exactly the rates as published on their homepage.

4 Likes

Indeed that’s crap lol, the SARON margin sits at 0.85 with this rate or something like that.

Wow too bad, I was waiting for their mortgage product so badly, as I’m planning to get one in the next months.

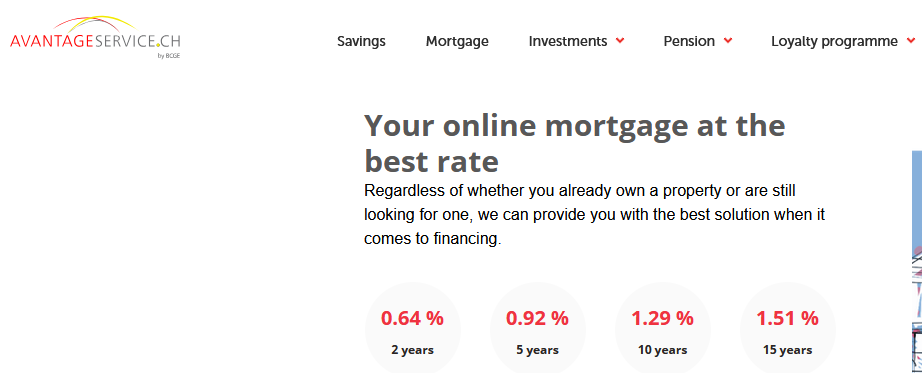

I guess hypotheke.ch will be my next target. Also found out “avantage service” which is a product by BCGE with extremely good rates

The rates are better than Viac for sure but you can get better, on the 10 year you have at least a 0.1% margin.

They still say the SARON margin is 0.65%, the total rate seems high because they do some kind of averaging over the past trimester (they claim the SARON rate is 0.86%, I guess they haven’t updated the text yet because it doesn’t add up but 0.42% average for the first trimester seems correct to me). If the margin is really 0.65% it is still a good deal over time, but the calculated rate lags quite a bit.