VIAC is launching a risk only insurance product (working with Helvetia): https://viac.ch/en/life

Not sure if they’re trying to reposition themselves in the potentially more lucrative insurance business, if they’re setting up to become usable for 3a pledging or indirect mortgage amortization (with the WIR bank? That one would be cool) or are pursuing some other goal.

“The amount for the risk coverage(s) is age-dependent and is recalculated each year based on the mortality / disability risk. This risk-based design has the advantage over the classic models with average premiums that the coverage is constantly adjustable and flexible. This means that you can increase, reduce or cancel the coverage(s) at any time without having to accept a loss of overpaid premium.”

I agree with you. That would be very interesting to know. Maybe we can use this community to collect the data since we do not have all the same age.

For a 100k insurance I have these values (rounded to 1 CHF; YOB = year of birth)

YOB dis. death 1983 121 82

Now everyone who wants to help can add his/her values for YOB, disability and death and of course sort by YOB increasing value so we will have a nice overview.

Maybe does someone even know how to make a nice table in this forum and improve my poor layout

Where did you check those values? When I’m accessing the app on my phone, I have a tab called “life”, but it’s only showing the basic 3a coverage if I have a certain amount of money at VIAC.

On another note: please make sure to also check you pillar 2 annual statement as well. Disability and death is also covered with pillar 2 as well. Afaik, the P2 amounts are annual amount, while the 100k from VIAC might be one time amounts.

How were you able to select different ages? I only have a slider to select the amount for death/disability.

I also just checked my P2 statement. Depending on the provider and your current amount of money in P2, you might already have a better coverage. I’m not sure how it works if you have two insurances for the same issue. I would have to check, but I think you are only eligible to get the higher one. Definitely something to check before signing a new contract with VIAC.

The premiums are pretty good at VIAC (for 300k death and 300k disability), roughly 30% of what is paid for my P2. But again, it’s a one time amount, whereas P2 pays an annual amount for disability and death (to your partner).

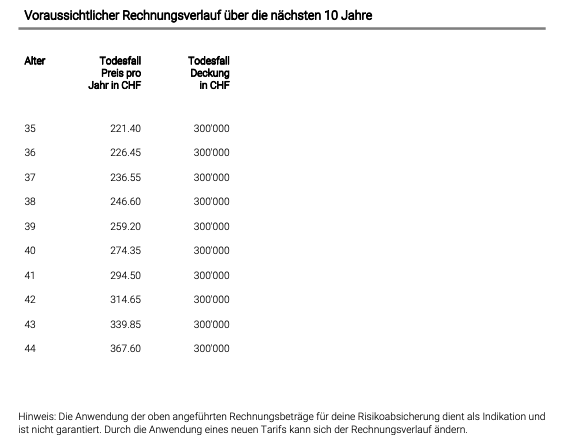

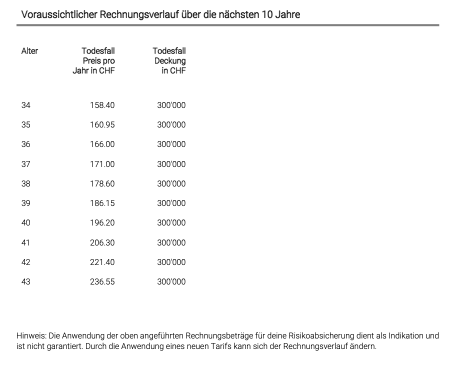

You get a 10 year preview (without price guarantee) with your invoice.

Yes, for many people pillars 1 and 2 (+ savings) may suffice in case of disability or death. I don’t have a pillar 2 myself, though.

Insurances indeed often have restrictions in case of double coverage. I wouldn’t expect lump sum payment, as in the case of VIAC Life Plus, to be an issue, though. However, I agree, it’s better to check this before signing the contract.

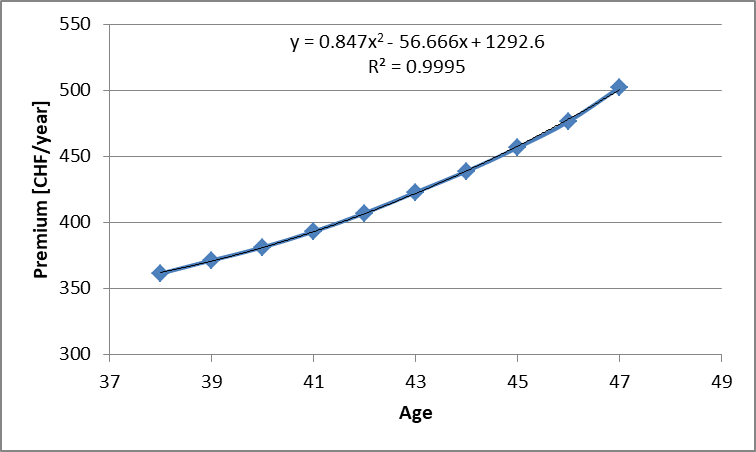

If they actually follow this formula the minimum premiums would be at 33 years of age…

We’d need some more “extreme” datapoints to check if it works over the whole age range

Im a bit confused on this one. I already have a General Prevista life insurance contract. Took out in Sep 2018, and its the same premium each year, 431.20 chf for a insured coverage of 200k.

VIACs offer for me is lower …for now, but then increases each year.

So it doesnt seem good value, but maybe i am missing something?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.