Ok but will you get a mortgage loan without a job?

Ok this is confusing. When you want a mortgage loan, you need to come up with more collateral than the actual loan. You got 200k, take 800k loan and you put the 1m house as collateral, so the LTV is 80%.

So I thought that, analogously, if you give 1m stock as collateral, they give you 250k loan, and begin liquidating when your stock dips below 500k. This made sense because stocks are more volatile than real estate, so they are worse as collateral.

Now you’re telling me something confusing. You’re saying that if put 250k in stock as collateral, the bank can lend me 1m cash? I guess I’m still understanding it wrong.

1 Like

I think you got it right and ChrisL confused something.

From https://www.mrmoneymustache.com/2021/01/29/margin-loan-ibkr-review/

5 Likes

Not at all. You are both right. It is just that this thread is about margin lending, and @ChrisL is talking about margin trading.

3 Likes

If you are buying stocks on margin, then these stocks are your collateral. Similar to if you buy property with a mortgage, this property is your collateral. You can take more mortgage than you need, then it is your margin loan. But if stocks go down strongly, they will be sold and you get a first hand experience what “deleveraging” in bear market means.

3 Likes

I had a read of IBKR education materials, and now I think @ChrisL is actually right!

Check this out:

And here an explanation from the SEC:

The equity in your margin account is the value of your securities less how much you owe to your brokerage firm. FINRA rules require this “maintenance requirement” to be at least 25 percent of the total market value of the margin securities. However, many brokerage firms have higher maintenance requirements, typically between 30 to 40 percent, and sometimes higher depending on the type of securities purchased.

Here’s an example of how maintenance requirements work. Let’s say you purchase $16,000 worth of securities by borrowing $8,000 from your firm and paying $8,000 in cash or securities. If the market value of the securities you purchased drops to $12,000, the equity in your account will fall to $4,000 ($12,000 - $8,000 = $4,000). If your firm has a 25 percent maintenance requirement, you must have $3,000 in equity in your account (25 percent of $12,000 = $3,000). In this case, you do have enough equity because the $4,000 in equity in your account is greater than the $3,000 maintenance requirement.

So this is how I understand it currently:

- you bring in 300k cash

- the broker lends you 300k cash

- you buy 600k worth of stock

- equity = stock_value - loan_value = 600k - 300k = 300k

- margin = equity / stock_value = 300k / 600k = 50%

Over time the value of your stock drops to 400k:

- equity = 100k

- margin = (400k - 300k) / 400k = 25%

Your stock drops again to 360k:

- equity = 60k

- margin = 60k / 360k = 16.6%

- this is below 25%, broker sells 120k of your stock

- broker uses it to repay the loan down to 180k

- after this: equity = still 60k, margin = 60k / 240k = 25%

Right, but these are two sides of the same coin, right? IBKR does not distinguish between lending or trading. They just check if you have at least 25% equity/loan in your account. So, effectively, you can borrow even three times as much you have.

So for example:

- you have a stock portfolio worth 300k

- the broker lets you to borrow up to 900k, which you can then withdraw from your account

- equity = 300k

- margin = 25%

It does because it controls the collateral when you buy stocks with it on IBKR.

If you take it out to buy a house, it cannot call it in anymore (at least not as easy). You could spend it on Roulette, hookers and alcohol and they would not know.

(so basically no, you cannot take out 900k out of IBKR with 300k, but you can have 300k of equity and buy stocks up to 1.2 M - not advised of course from a risk management point of view, except if you leave the 300k in cash/bonds or whatever “low risk AAA rating” and put the 900 k into stocks).

5 Likes

You can’t borrow 900k because of the inital margin requirement of 50%. You can only borrow 300k.

2 Likes

No, you can’t. And that’s the point. You can buy stocks and whatever you want with borrowed funds, but they have to stay in your account. Otherwise your margin requirements are not satisfied.

And that what I meant talking about the difference between margin loan and margin trading.

2 Likes

Thanks, that makes sense. If you withdrew 900k from IBKR, your equity would go to -600k, which is of course forbidden.

So if you had 300k stock in your porfolio, the following requirement would have to be met:

(stock_value - withdrawn_amount) / stock value >= 25%

So the maximum withdrawn amount is:

withdrawn_amount <= stock value * 75%

So it goes like this:

- I have 300k in my portfolio

- I get a margin loan of 225k (75% of 300k)

- I withdraw the 225k to buy a flat

- equity = stock - loan = 300k - 225k = 75k

- margin = equity / stock = 75k / 300k = 25%

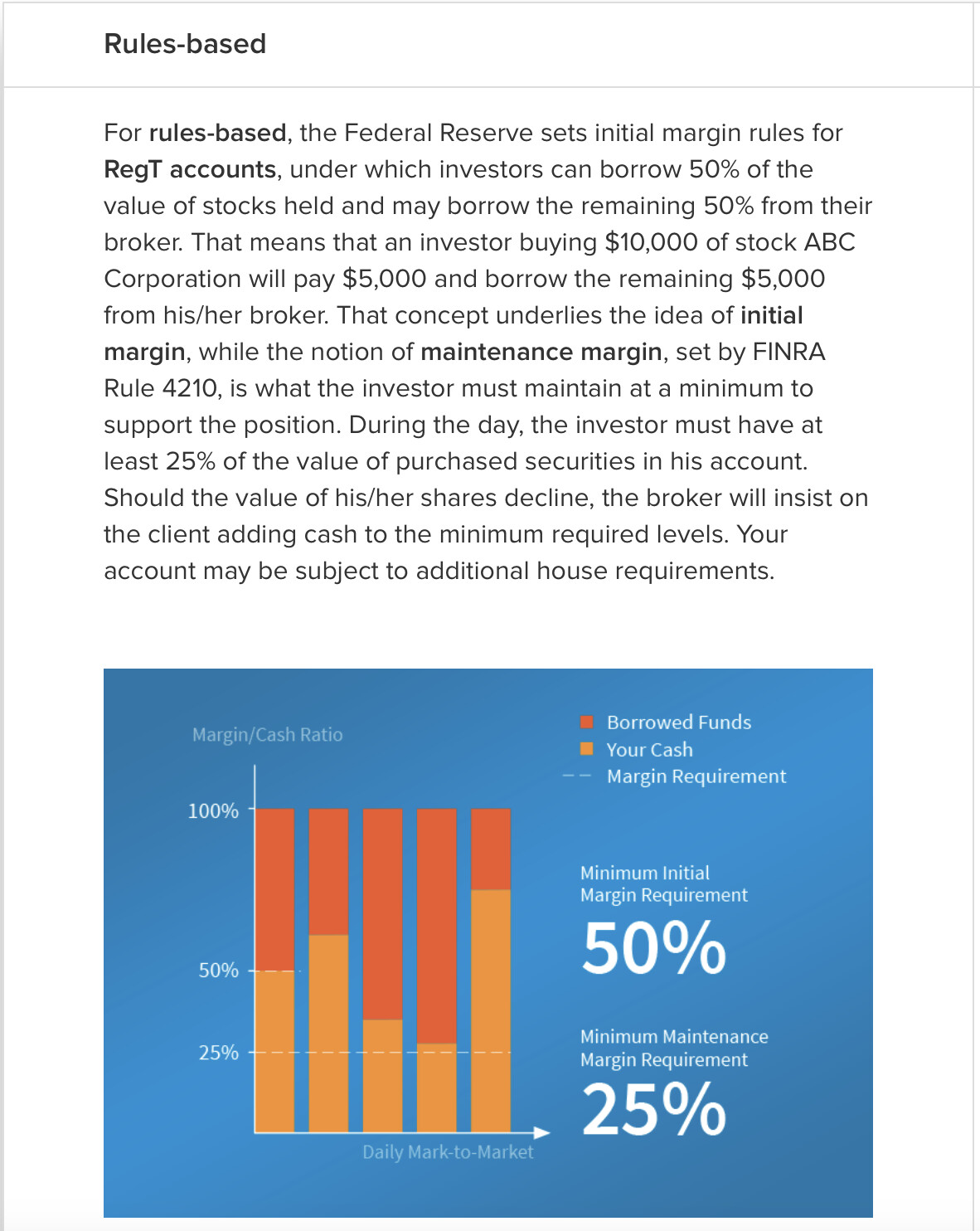

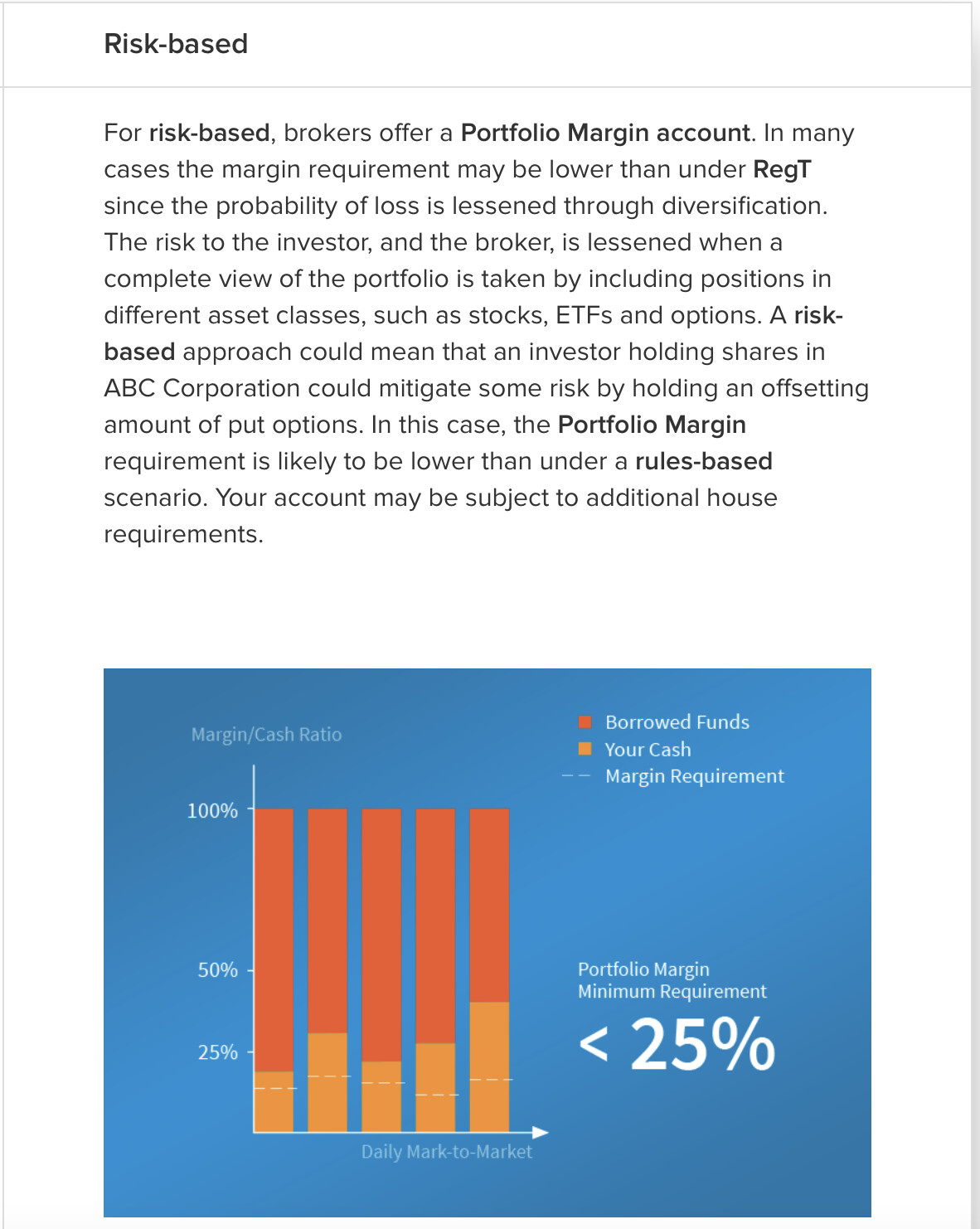

Are you absolutely 100% sure about this? From what I see is that IBKR offers two types of margin accounts:

- rule based (Regulation T applies)

- risk based (a.k.a. Portfolio Margin)

Are you sure you can’t get down to 25% initial margin with a portfolio margin account?

Ah maybe with portfolio margin, depending on your collateral. I was talking about reg T margin.

But keep in mind that the maintenance margin requirement can change any time for a single stock.

It happened during the “corona crash” and probably any time there is some kind of crash.

So you might think you are on the safe side above, say, 25% and then IBKR tells you that next week it becomes 50%.

5 Likes

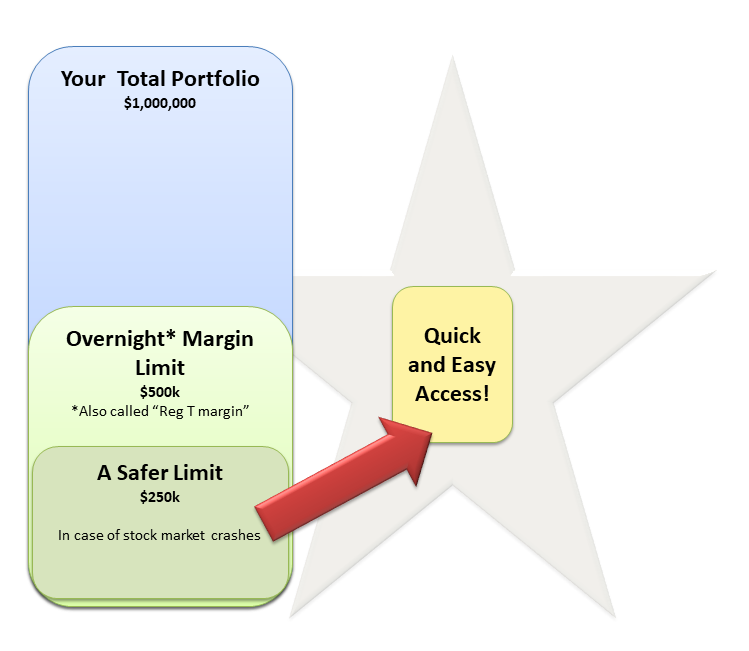

Right, I am only using max values to understand how it works. I want to know the limits, not to use it in practice. I suppose if I had 1m at IBKR and wanted to finance a real estate purchase, I would maybe withdraw 250k for a longer period of time. In such a scenario I would not get in trouble until my stock value fell 50% to just 500k.

But for sure this margin is very practical if you want to quickly buy a dip in some stock, and you don’t want to wait for the bank transfer to come through. Or worse, wait for your next salary.

What I’ve dealt with in the past, is that I wanted to buy an even number of TSLA shares, like 100. But I always had to transfer too much cash to take price swings into account. With margin it’s so simple. You just buy the stock, you automatically get a negative cash balance, and a few weeks later you transfer the exact amount that you’re short.

By the way, you didn’t take into account that mortgage comes with cash downpayment of 20% (35% eventually), and this cash can’t work for you for the entire duration of the mortgage. Whereas the pledged stock still yields returns.

1 Like

Actually I see another case for margin.

Let’s say your FIRE value is 1 MCHF, you need 40 kCHF/y (simple 4% rule to make it easy - just a concept study)

With margin you could do :

-Deposit 604 kCHF in IBKR in VT

-Take another 400 kCHF in margin

-With the actual 1% margin rate on that amount (4000 kCHF/y) you got your 40 kCHF income, and you pay less wealth tax (since you are actually only having 600 kCHF wealth) , plus you can deduct the 4 kCHF interest from your income

Would I do it ? Probably not, I am way to risk averse for that (100% stocks portfolio fine, but going margin… Nah).

I was considering this. The problem that I see is that unlike for example for a mortgage, there is no guarantee that the margin loan will be available in the future and conditions can change any time.

There is a blog post from big ERN on the topic. You might want to give it a read.

2 Likes

I think you understand this already, but I think it’s worth it to put some emphasis on Gesk’s point: what we can calculate are the current limits. IBKR can change them at any time and for any reason. This can particularly happen in bear markets. For example, in a few days, the collateral value of VWRL shares in CHF will apparently be 0. Not a big deal since VWRD seems to be keeping it’s collateral value, but an indication of how quickly things can change.

5 Likes

Ok that’s a bummer. Then idk how MMM went through with buying real estate like this. Btw I wonder how rich people do this. They have this line of credit thing, I guess banks are a bit more solid when it comes to the rules that you agree on.

Yes I saw that VWRL’s collateral value will become 0. Do you know why is that?

The IB TWS has a feature that estimates the portfolio margin you would receive. Since it is risk based it depends on the stocks you have. I just ran it on a paper trading account and got for VT an extremely low 10% and for TSLA I got 40% (TSLA is 40% on Reg T account as well, but at least the portfolio account removes the overnight 50% rule).

As pointed out by others, it would be pretty crazy to go that low and put the money into an illiquid asset. But on the other hand one should know the limits, if only to know how much safety buffer there is in case of a (inevitable) crash. Converting to a portfolio margin account would increase that safety buffer, but expect that IB will increase their margin requirements exactly when you would need that buffer: in a crash.

If you can stay clear of the 50% mark even during a decent crash maybe you have a case. Somewhere north of 80% in good times should survive the bad times as well. That still gives you $1 million out of your “insane $5 million portfolio”. If that is not enough maybe you can still find a way to pledge the house itself as collateral? It should still be possible to get a mortgage approved when you sit on such a portfolio.

3 Likes

No idea. Nobody shared that experience yet. But surely, any Swiss bank would need to have custody of this portfolio in order to give a mortgage?

I just wonder if you can get a mortgage without income, so that you can buy real estate without having to sell any of your stocks.